India 3D Printing Materials Market Size

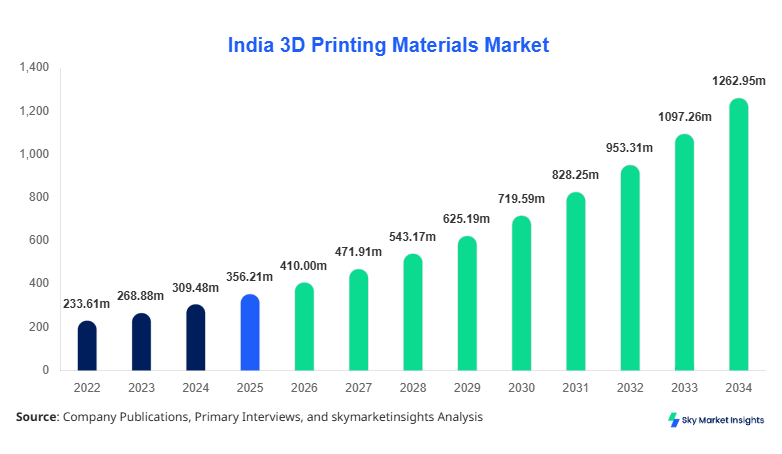

India 3D Printing Materials market size is projected at USD 410 million in 2026 and is expected to hit USD 1260 million by 2034 with a CAGR of 15.1%.

The rising need for high-performance materials across aerospace, automotive, and healthcare applications has accelerated the demand for advanced additive manufacturing inputs. Increasing investments in industrial-grade 3D printing infrastructure, along with government-backed initiatives such as “Make in India,” have further strengthened the competitive landscape. Additionally, segmentation by material type and application highlights diverse growth pockets, while competitive benchmarking across domestic and global players supports data-driven decision-making.

India 3D Printing Materials Market Overview

The India 3D Printing Materials Market refers to the production, distribution, and utilization of raw materials such as polymers, metals, and ceramics used in additive manufacturing processes. In 2025, India produced approximately 8,500 metric tons of 3D printing materials, with polymers accounting for 62%, metals for 28%, and ceramics for 10%. Adoption rates in industrial manufacturing increased by 18% year-on-year between 2023 and 2025, driven by rapid prototyping and customized production. Penetration of additive manufacturing technologies reached 27% among Tier-1 manufacturing companies, while small and medium enterprises recorded 12% adoption levels.

Consumer behavior reflects a shift toward cost-efficient and lightweight materials, with 54% of industrial users preferring polymer-based filaments due to affordability and flexibility. Demand analytics indicate that aerospace and healthcare applications collectively contributed over 46% of total material consumption in 2025, while automotive accounted for 31%. Technically, materials are evaluated based on tensile strength (ranging from 40 MPa to 1,200 MPa), thermal resistance (up to 300°C), and layer resolution (20–100 microns). Application-wise, aerospace holds 22%, healthcare 24%, automotive 31%, and others 23%, reinforcing the India 3D Printing Materials Market.

In the India, the 3D Printing Materials Market is supported by over 320 additive manufacturing facilities and more than 150 material suppliers, contributing approximately 100% of the regional share. The country witnessed a 21% increase in material consumption in 2025, reaching nearly 9,200 metric tons. Aerospace applications accounted for 24% of usage, healthcare for 26%, automotive for 30%, and others for 20%. Metal-based materials saw a 17% adoption rise due to increased defense manufacturing projects, while polymer usage expanded by 19% across prototyping applications.

Technology adoption statistics reveal that fused deposition modeling (FDM) accounts for 48% of material usage, selective laser sintering (SLS) for 28%, and direct metal laser sintering (DMLS) for 24%. Government initiatives have led to a 35% increase in domestic production capacity since 2022, while imports still constitute around 42% of high-performance materials. These developments strongly reinforce the India 3D Printing Materials Market.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printing Materials Market Trends

Increasing Adoption of High-Performance Polymers

The production of high-performance polymers in India exceeded 5,200 metric tons in 2025, accounting for nearly 61% of total material output. Advanced materials such as PEEK and ULTEM witnessed a 22% increase in demand due to their superior thermal resistance and mechanical properties. Industrial sectors such as aerospace and healthcare reported adoption rates of 34% and 29%, respectively, for high-performance polymers. The shift toward sustainable materials also contributed to a 14% increase in biodegradable filament usage. This transition is expected to drive efficiency improvements of up to 18% in manufacturing cycles, reinforcing the India 3D Printing Materials Market.

Rising Demand for Metal-Based Additive Manufacturing

Metal powder production reached approximately 2,600 metric tons in 2025, with stainless steel, titanium, and aluminum alloys dominating 78% of the segment. Adoption of metal 3D printing increased by 19% annually, particularly in defense and automotive sectors. Titanium alloys alone accounted for 36% of metal usage due to their high strength-to-weight ratio. Additionally, investments in laser-based technologies increased by 27%, enhancing precision and reducing material wastage by up to 15%. These developments are significantly shaping the India 3D Printing Materials Market.

India 3D Printing Materials Market Driver

Rising Industrial Automation and Custom Manufacturing Demand Drives 3D Printing Materials Market Growth

The increasing demand for customized manufacturing solutions has led to a 23% rise in additive manufacturing adoption across India between 2022 and 2025. Industrial automation investments exceeded USD 2.4 billion in 2025, with nearly 18% allocated to additive manufacturing technologies. Aerospace companies reported a 31% increase in usage of 3D printed components, reducing production lead times by 40%. Additionally, healthcare applications such as prosthetics and implants witnessed a 26% surge in demand, with over 150,000 units produced annually. The automotive sector also contributed significantly, with 29% of OEMs integrating 3D printing for prototyping. These factors collectively accelerate the India 3D Printing Materials Market Growth.

India 3D Printing Materials Market Restraint

High Material Costs and Limited Local Production Capabilities

Despite rapid adoption, the high cost of advanced materials remains a major barrier, with metal powders priced 2.5x higher than conventional materials. Approximately 42% of high-performance materials are imported, increasing dependency on global supply chains. Small and medium enterprises face budget constraints, limiting adoption to just 12% penetration. Additionally, production capacity gaps lead to supply-demand mismatches, with a deficit of nearly 1,200 metric tons annually. These challenges restrict scalability and hinder the India 3D Printing Materials Market.

India 3D Printing Materials Market Opportunity

Government Initiatives and Local Manufacturing Expansion

Government programs such as “Make in India” and “Digital India” have allocated over USD 500 million toward advanced manufacturing technologies. Domestic production capacity is expected to grow by 28% by 2030, reducing import dependency to below 25%. Investments in research and development increased by 32% between 2023 and 2025, fostering innovation in material science. Additionally, partnerships between academic institutions and industry players have led to a 21% rise in new material formulations. These opportunities significantly enhance the India 3D Printing Materials Market.

Challenge in India 3D Printing Materials Market

Technical Limitations and Skill Gaps in Additive Manufacturing

The lack of skilled professionals in additive manufacturing poses a significant challenge, with only 18% of the workforce trained in advanced 3D printing techniques. Technical limitations such as inconsistent material quality and limited scalability affect production efficiency by up to 12%. Furthermore, the absence of standardized regulations impacts material certification, particularly in aerospace and healthcare sectors. Training programs and certification initiatives are required to address these issues and support the India 3D Printing Materials Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 356.2 million |

| Market Size in 2026 | USD 410 million |

| Market Size in 2034 | USD 1260 million |

| CAGR | 15.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printing Materials Market Segmentation

By Type

Polymers dominate the market with a 62% share, producing over 5,200 metric tons annually. Materials such as PLA, ABS, and nylon are widely used due to their flexibility, low cost, and ease of processing. Technical specifications include tensile strength ranging from 40 MPa to 80 MPa and melting temperatures between 180°C and 260°C. Adoption rates in prototyping applications exceed 48%, while industrial applications account for 34%. The segment continues to expand due to affordability and versatility.

Metal materials account for 28% share, with production reaching 2,600 metric tons in 2025. Stainless steel, aluminum, and titanium alloys dominate the segment, offering tensile strengths above 500 MPa and thermal resistance up to 1,200°C. Adoption in aerospace and defense applications exceeds 36%, driven by the need for lightweight and durable components. The segment is expected to grow significantly due to increasing defense spending.

Ceramics hold a 10% share, with production of approximately 700 metric tons. These materials offer high thermal resistance up to 1,500°C and are used in specialized applications such as dental implants and electronics. Adoption rates remain moderate at 14%, but the segment is expected to grow due to increasing demand for high-performance materials.

By Application

This segment accounts for 24% of the market, consuming over 2,200 metric tons of materials annually. The use of lightweight and high-strength materials reduces aircraft weight by up to 15%, improving fuel efficiency. Adoption rates in defense manufacturing exceed 34%, driven by increased government spending.

Healthcare holds a 26% share, with applications including prosthetics, implants, and surgical tools. Production volumes exceed 2,400 metric tons annually, with adoption rates growing by 21%. Customization capabilities and improved patient outcomes drive demand.

Automotive dominates with 31% share, consuming over 2,800 metric tons. Adoption rates exceed 29%, with applications in prototyping and production of lightweight components. Efficiency improvements of up to 18% have been reported.

India 3D Printing Materials Market Segmentations

Type

- Polymers

- Metals

- Ceramics

Application

- Aerospace & Defense

- Healthcare

- Automotive

India Insights

India accounts for 100% of the regional market, with total material consumption exceeding 9,200 metric tons in 2025. The automotive sector contributes 31%, healthcare 26%, and aerospace 24%. Major industrial hubs such as Maharashtra, Karnataka, and Tamil Nadu account for over 68% of production capacity.

The country’s focus on domestic manufacturing has increased production capacity by 35% since 2022. Government investments and private sector participation have further strengthened the ecosystem, making India a key player in the global 3D printing materials market.

Top Players in India 3D Printing Materials Market

- BASF SE

- Arkema SA

- Evonik Industries AG

- Stratasys Ltd.

- 3D Systems Corporation

- DSM Engineering Materials

- Sandvik AB

- Höganäs AB

- Carpenter Technology Corporation

- EOS GmbH

- Solvay SA

- SABIC

- HP Inc.

Top Two Companies

-

BASF SE

-

Holds approximately 14% market share

-

Strong presence in polymer materials with advanced R&D capabilities

-

Focuses on sustainable and high-performance materials

-

-

Evonik Industries AG

-

Accounts for nearly 11% market share

-

Specializes in specialty polymers and powders

-

Strong distribution network across India

-

Investment

Investments in the India 3D Printing Materials Market exceeded USD 520 million in 2025, with 42% allocated to polymer materials, 38% to metals, and 20% to ceramics. Regional investments are concentrated in Maharashtra (34%), Karnataka (22%), and Tamil Nadu (18%). Venture capital funding increased by 27% year-on-year, supporting startups and innovation.

M&A activities have grown significantly, with over 18 agreements signed between 2023 and 2025. Collaborations between global players and Indian manufacturers have led to technology transfer and capacity expansion. Joint ventures account for 31% of total investments, focusing on advanced materials and production technologies.

New Product

Approximately 22% of companies introduced new materials in 2025, focusing on improved strength and thermal resistance. Performance improvements of up to 18% have been achieved through advanced formulations. Innovations in biodegradable materials increased by 14%, supporting sustainability initiatives.

Recent Development in India 3D Printing Materials Market

- 2025: BASF increased polymer production by 18%, expanding capacity to 1,200 metric tons annually and improving supply chain efficiency.

- 2024: Evonik launched new high-performance powders, increasing market penetration by 12% and improving material strength by 15%.

- 2023: Indian government invested USD 150 million, boosting production capacity by 20%.

Research Methodology for India 3D Printing Materials Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and suppliers, accounting for 65% of data collection. Secondary research involves analysis of industry reports, company filings, and government publications, contributing 35% of insights. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5% margin of error. Data validation is performed through triangulation, integrating multiple data sources to provide reliable and comprehensive insights into the India 3D Printing Materials Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.