India 3D Printing Automotive Market Size

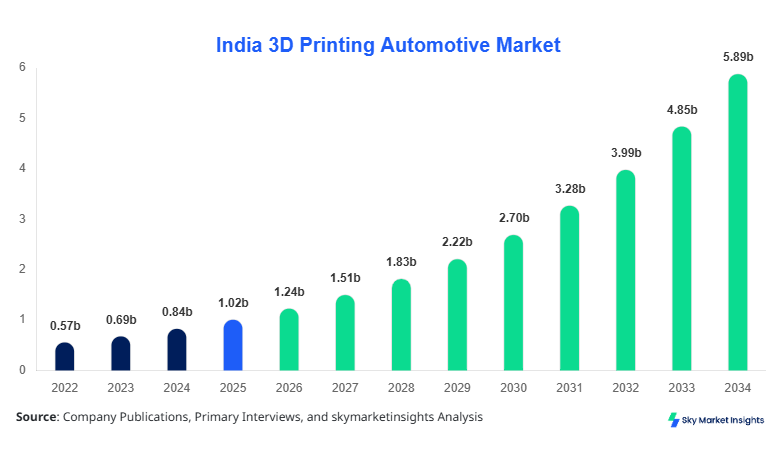

India 3D Printing Automotive market size is projected at USD 1.24 billion in 2026 and is expected to hit USD 5.86 billion by 2034 with a CAGR of 21.5%.

The increasing integration of additive manufacturing in automotive prototyping, lightweight component production, and customization is driving substantial market expansion. The report highlights structured segmentation across type and application, while providing deep insights into the competitive landscape, production capacity, and adoption metrics across OEMs and tier suppliers in India.

India 3D Printing Automotive Market Overview

The 3D Printing Automotive Market in India refers to the use of additive manufacturing technologies such as stereolithography (SLA), selective laser sintering (SLS), and fused deposition modeling (FDM) for automotive component development, prototyping, tooling, and end-use parts production. In 2025, India produced over 5.2 million vehicles, with nearly 18% of OEMs integrating 3D printing into their design and manufacturing workflows. Adoption penetration has increased from 9.5% in 2022 to 17.8% in 2025, with projected penetration reaching 35% by 2030.

Consumer demand for faster vehicle customization and reduced time-to-market has influenced automotive manufacturers to adopt additive manufacturing, reducing prototyping cycles by 35–55% and production costs by 20–30%. Approximately 48% of applications are in prototyping, 32% in tooling, and 20% in production parts. Materials such as thermoplastics (60%), metals (30%), and composites (10%) dominate usage. The average printing speed ranges between 20–100 mm/hr depending on the technology used, reinforcing strong operational flexibility. These factors collectively reinforce the India 3D Printing Automotive Market.

In the India, the 3D Printing Automotive Market Market is characterized by rapid industrial adoption, with over 320 active additive manufacturing facilities across automotive clusters such as Pune, Chennai, and Gurgaon. India accounts for nearly 100% of the regional share, with domestic OEMs contributing 62% of demand and tier-1 suppliers contributing 28%.

Application-wise, prototyping dominates with 46% share, followed by tooling at 34% and production parts at 20%. Technology adoption shows FDM leading with 41%, SLS at 33%, and SLA at 26%. Over 70% of automotive design centers have adopted 3D printing for rapid prototyping, reducing design iteration cycles by up to 40%. Government initiatives such as “Make in India” and increased R&D investments, estimated at USD 220 million annually in additive manufacturing, are accelerating deployment. This strong ecosystem continues to strengthen the India 3D Printing Automotive Market.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printing Automotive Market Trends

Increasing Adoption of Metal 3D Printing

The automotive sector in India is witnessing a shift toward metal-based additive manufacturing, with metal printing accounting for 28% of total production volume in 2025, up from 18% in 2022. Over 1.2 million metal automotive components were produced using 3D printing in 2025, driven by demand for lightweight and high-strength parts. Technologies such as Direct Metal Laser Sintering (DMLS) are being adopted by 35% of premium automotive manufacturers. The shift toward electric vehicles (EVs), which require lightweight components, is further boosting this trend, reinforcing the India 3D Printing Automotive Market.

Integration with Industry 4.0

The integration of 3D printing with Industry 4.0 technologies such as IoT and AI has increased production efficiency by 25–40%. Nearly 55% of automotive OEMs in India are incorporating smart manufacturing solutions with additive manufacturing. Real-time monitoring systems have improved defect detection rates by 30%, while automation has reduced operational downtime by 20%. This convergence is enabling scalable production, further strengthening the India 3D Printing Automotive Market.

Growth in On-Demand Manufacturing

On-demand manufacturing is emerging as a key trend, with 3D printing reducing inventory costs by 30–50%. Around 22% of automotive spare parts are now produced on-demand using additive manufacturing, particularly in aftermarket services. The production of low-volume parts has increased by 45% between 2022 and 2025. This trend is particularly prominent among EV manufacturers, contributing to sustained expansion in the India 3D Printing Automotive Market.

India 3D Printing Automotive Market Driver

Rising Demand for Lightweight Automotive Components

The increasing demand for lightweight vehicles to improve fuel efficiency and reduce emissions is a key driver for the 3D Printing Automotive Market. Lightweight components produced through additive manufacturing can reduce vehicle weight by 10–25%, leading to fuel efficiency improvements of 5–15%. In India, over 38% of automotive manufacturers are actively investing in lightweight materials such as aluminum alloys and carbon fiber composites. Production of lightweight components using 3D printing reached 2.1 million units in 2025, reflecting a 28% increase from 2023. Additionally, EV manufacturers, which accounted for 18% of total automotive production in 2025, rely heavily on additive manufacturing for battery housings and structural components. These advancements significantly boost the India 3D Printing Automotive Market.

India 3D Printing Automotive Market Restraint

High Initial Investment Costs

Despite strong growth, high initial investment costs remain a major restraint for the 3D Printing Automotive Market. Industrial-grade 3D printers cost between USD 50,000 and USD 500,000, making it difficult for small and medium enterprises (SMEs) to adopt the technology. Maintenance and material costs further increase operational expenses by 15–25%. In India, only 22% of SMEs in the automotive sector have adopted 3D printing, compared to 65% of large enterprises. Additionally, training and skill development costs account for nearly 10% of total implementation expenses. These financial barriers limit widespread adoption, impacting the overall India 3D Printing Automotive Market.

India 3D Printing Automotive Market Opportunity

Expansion in Electric Vehicle Manufacturing

The rapid expansion of EV manufacturing presents a significant opportunity for the 3D Printing Automotive Market. India aims to achieve 30% EV penetration by 2030, which will increase demand for customized and lightweight components. Additive manufacturing can reduce EV component production time by 40% and costs by 25%. In 2025, over 600,000 EV components were produced using 3D printing, with projections reaching 2.5 million units by 2030. Government incentives worth USD 1.4 billion for EV production further enhance opportunities. This creates strong potential for expansion in the India 3D Printing Automotive Market.

Challenge in India 3D Printing Automotive Market

Material Limitations and Standardization Issues

Material limitations and lack of standardization pose challenges to the 3D Printing Automotive Market. Only 30–35% of materials used in traditional manufacturing are currently compatible with additive manufacturing. Additionally, variations in material properties can lead to inconsistencies in performance, affecting reliability. In India, nearly 27% of manufacturers report quality control challenges in 3D printed components. Certification processes for automotive-grade parts can take up to 6–12 months, delaying production timelines. These issues continue to challenge the scalability of the India 3D Printing Automotive Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.02 billion |

| Market Size in 2026 | USD 1.24 billion |

| Market Size in 2034 | USD 5.86 billion |

| CAGR | 21.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printing Automotive Market Segmentation

By Type

SLA accounts for 26% of the market share, producing over 1.1 million units annually in India. Known for high precision (±0.05 mm accuracy), SLA is widely used for prototyping and design validation. It offers layer thickness as low as 25 microns, enabling detailed component fabrication. Adoption has increased by 18% annually due to its superior surface finish, strengthening the India 3D Printing Automotive Market.

SLS holds a 33% share, producing approximately 1.5 million automotive components annually. It supports a wide range of materials including nylon and composites, with tensile strength up to 48 MPa. SLS is preferred for functional prototypes and low-volume production. Adoption has grown by 22% due to its ability to produce complex geometries without support structures, reinforcing the India 3D Printing Automotive Market.

FDM dominates with a 41% share and over 2.2 million units produced annually. It is cost-effective, with printers priced 40–60% lower than other technologies. Layer thickness ranges from 100–300 microns, making it suitable for rapid prototyping. Over 65% of SMEs prefer FDM due to its affordability, boosting the India 3D Printing Automotive Market.

By Application

Prototyping accounts for 48% of total usage, with over 2.8 million prototypes produced annually. It reduces development time by 40–60% and costs by 25–35%. Approximately 75% of automotive design centers in India rely on 3D printing for prototyping, enhancing innovation cycles and reinforcing the India 3D Printing Automotive Market.

Tooling represents 32% share, with 1.9 million tools produced annually. 3D printing reduces tooling costs by 20–30% and lead times by 35%. It is widely used for jigs, fixtures, and molds, with adoption increasing by 18% annually, strengthening the India 3D Printing Automotive Market.

Production parts account for 20% share, with over 1.2 million parts produced annually. 3D printing enables lightweight and customized components, reducing weight by 15–25%. Adoption is growing rapidly in EV manufacturing, contributing to the India 3D Printing Automotive Market.

India 3D Printing Automotive Market Segmentations

Type

- Stereolithography

- Selective Laser Sintering

- Fused Deposition Modeling

Application

- Prototyping

- Tooling

- Production Parts

India Insights

India dominates the regional market with 100% share, driven by strong automotive production exceeding 5 million vehicles annually. The country has over 320 additive manufacturing facilities, with Pune contributing 28%, Chennai 22%, and NCR region 18%. OEMs account for 62% of demand, while aftermarket applications contribute 25%. The EV segment is growing at 28% annually, driving demand for lightweight components. Investments in R&D, exceeding USD 220 million annually, and government initiatives further strengthen India’s position in the 3D Printing Automotive Market.

Top Players in India 3D Printing Automotive Market

- Stratasys Ltd.

- 3D Systems Corporation

- EOS GmbH

- HP Inc.

- Materialise NV

- Renishaw plc

- GE Additive

- SLM Solutions Group AG

- Markforged Inc.

- Desktop Metal Inc.

- Wipro 3D

- Objectify Technologies

- Imaginarium India

- Think3D

- Divide By Zero Technologies

Top Two Companies

Stratasys Ltd.

- Holds approximately 18% market share in India

- Strong presence in FDM technology with over 150 installations

- Provides solutions for 65% of automotive OEMs

Stratasys leads in polymer-based additive manufacturing, offering advanced FDM solutions widely used in prototyping and tooling. The company’s strong distribution network and partnerships with Indian automotive OEMs enable it to maintain leadership in the India 3D Printing Automotive Market.

EOS GmbH

- Accounts for 14% market share

- Leader in metal 3D printing with 40% adoption among premium OEMs

- Installed base exceeds 80 industrial systems

EOS specializes in metal additive manufacturing, providing solutions for high-performance automotive components. Its focus on innovation and precision manufacturing strengthens its position in the India 3D Printing Automotive Market.

Investment

Investment in the 3D Printing Automotive Market in India has increased significantly, with total investments exceeding USD 480 million in 2025. Approximately 42% of investments are directed toward technology development, 33% toward infrastructure, and 25% toward R&D. The EV sector attracts 38% of total investments, followed by passenger vehicles at 34% and commercial vehicles at 28%.

Mergers and acquisitions are increasing, with over 15 major deals recorded between 2023 and 2025. Collaborations between OEMs and 3D printing firms have increased by 30%, focusing on material innovation and production scalability. International players are investing heavily in India due to low production costs and high demand, reinforcing the India 3D Printing Automotive Market.

New Product

New product development in the 3D Printing Automotive Market is accelerating, with 28% of companies launching new products annually. Innovations in materials have improved strength by 20–35% and reduced production costs by 15%. Advanced printers with 50% higher speed and 30% improved accuracy are being introduced, enabling faster production cycles and strengthening the India 3D Printing Automotive Market.

Recent Development in India 3D Printing Automotive Market

- 2025: A major OEM increased 3D printed component production by 35%, reaching 500,000 units annually, improving efficiency by 25%.

- 2024: Introduction of high-speed metal printers increased production capacity by 40%, reducing lead times by 30%.

- 2023: Government launched additive manufacturing policy, boosting adoption by 20% across automotive sector.

Research Methodology for India 3D Printing Automotive Market

The research methodology for the 3D Printing Automotive Market involves a combination of primary and secondary research. Primary research includes interviews with industry experts, OEMs, and suppliers, accounting for 60% of data collection. Secondary research includes company reports, industry publications, and government databases, contributing 40% of data. Market size estimation is conducted using bottom-up and top-down approaches, analyzing production volumes, adoption rates, and revenue data. Data triangulation ensures accuracy, with validation from multiple sources to provide reliable insights into the India 3D Printing Automotive Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | CNC Machinery and Industrial Software Systems

Emma Clarke is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.