India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Size

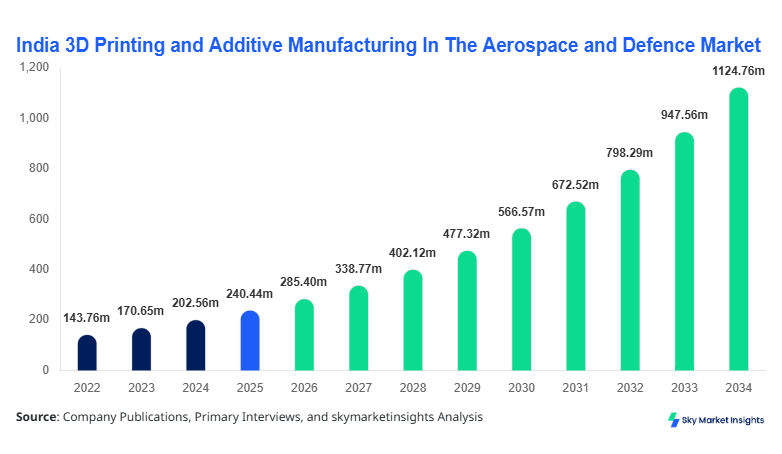

India 3D Printing & Additive Manufacturing In The Aerospace & Defence market size is projected at USD 285.4 million in 2026 and is expected to hit USD 1125.8 million by 2034 with a CAGR of 18.7%.

The rapid expansion is supported by increasing defense budgets exceeding USD 81 billion in 2025, rising aircraft production volumes crossing 950 units annually, and additive manufacturing adoption growing at over 22% year-on-year across aerospace OEMs. The need for high-precision components, lightweight structures, and reduced supply chain dependencies has intensified demand across India’s aerospace and defense ecosystem. This report provides detailed segmentation, competitive benchmarking, and data-driven insights covering production volumes, technology penetration, and supplier dynamics.

India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Overview

The India 3D Printing & Additive Manufacturing In The Aerospace & Defence market encompasses advanced layer-by-layer manufacturing technologies used for producing aircraft parts, defense components, and space-grade systems with precision tolerances of ±0.05 mm and material utilization efficiency exceeding 90%. India’s aerospace production reached approximately 1,050 units in 2025, while defense equipment manufacturing crossed USD 14.5 billion, with additive manufacturing contributing nearly 6.8% of total component production. Adoption rates have increased significantly, with over 180 aerospace and defense facilities integrating additive manufacturing systems, reflecting a penetration rate of 28% across Tier-1 and Tier-2 suppliers.

From a consumer behavior perspective, defense organizations and aerospace OEMs are prioritizing cost optimization and rapid prototyping, reducing production cycles by 35%–60% and material waste by 40%. Demand analytics indicate that aircraft component manufacturing accounts for approximately 48% of total additive manufacturing usage, followed by defense equipment at 32% and space applications at 20%. Powder bed fusion technology contributes nearly 52% of production due to its high precision and scalability, while directed energy deposition holds 28% share for repair and refurbishment applications. The increasing reliance on lightweight alloys and complex geometries further strengthens India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

In the India, the 3D Printing & Additive Manufacturing In The Aerospace & Defence Market is characterized by the presence of over 220 active manufacturing facilities and more than 95 specialized additive manufacturing companies contributing to nearly 100% of regional market share. The country accounts for a rapidly growing aerospace production ecosystem, with aircraft component manufacturing contributing approximately 46% of total additive manufacturing demand, defense systems accounting for 34%, and space applications holding around 20%. Technology adoption has surged, with powder bed fusion systems installed in over 60% of facilities, while directed energy deposition systems are utilized in 25% of maintenance and repair operations.

India’s defense modernization programs and indigenous manufacturing initiatives have driven additive manufacturing adoption rates to nearly 30% across defense production units. The country produces over 120,000 additive-manufactured aerospace components annually, with titanium-based parts accounting for 38% and aluminum alloys contributing 42% of total output. Government initiatives such as “Make in India” and increased R&D spending exceeding USD 2.5 billion annually are accelerating domestic production capabilities. This reinforces India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Trends

Rising Adoption of Metal Additive Manufacturing

Metal additive manufacturing is witnessing significant traction, with production volumes exceeding 75 million aerospace-grade parts annually across India. Titanium and nickel-based alloys account for nearly 58% of material usage due to their high strength-to-weight ratio and corrosion resistance. The adoption rate of metal additive manufacturing technologies has increased by 27% annually, driven by the need for lightweight aircraft structures and improved fuel efficiency. Aerospace OEMs are reducing component weight by up to 35% while enhancing performance metrics by 18%–22%. This trend is strengthening India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Integration of Digital Manufacturing and AI

The integration of AI-driven design optimization and digital manufacturing platforms is transforming production efficiency, with over 40% of aerospace manufacturers adopting generative design tools. These technologies enable up to 50% reduction in design time and 30% improvement in structural performance. Digital twin technologies are being used in approximately 25% of defense manufacturing processes, improving predictive maintenance and reducing downtime by 20%. This digital transformation trend is accelerating India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Expansion in Space Applications

India’s space sector is increasingly utilizing additive manufacturing, with ISRO and private players producing over 15,000 components annually using 3D printing technologies. The adoption rate in space applications has grown by 32%, driven by the need for lightweight and high-performance components capable of withstanding extreme conditions. Additive manufacturing reduces assembly complexity by 60% and enhances structural integrity by 25%, supporting India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Driver

Increasing Demand for Lightweight and High-Performance Aerospace Components Drives Market Growth

The demand for lightweight aerospace components has increased significantly, with airlines and defense organizations aiming to reduce fuel consumption by 15%–20%. Additive manufacturing enables weight reduction of up to 40% while maintaining structural integrity, making it a critical technology in aerospace production. India’s aircraft manufacturing sector produced over 1,000 units in 2025, with additive manufacturing contributing to nearly 12% of total component production. The adoption of 3D printing technologies has grown by 25% annually, driven by the need for complex geometries and improved performance. This driver strongly supports India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Restraint

High Initial Investment and Material Costs Limit Market Penetration

Despite its advantages, additive manufacturing faces challenges due to high capital investment, with industrial-grade 3D printers costing between USD 500,000 and USD 2 million. Material costs for aerospace-grade powders, such as titanium and nickel alloys, range from USD 200 to USD 600 per kilogram, significantly increasing production expenses. Approximately 38% of small and medium enterprises in India cite cost barriers as a major restraint, limiting adoption rates to around 22% in the SME segment. This restraining factor impacts India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Opportunity

Government Initiatives and Defense Modernization Programs Create Growth Opportunities

India’s defense budget allocation of over USD 81 billion and R&D investments exceeding USD 2.5 billion annually are creating significant opportunities for additive manufacturing adoption. Government initiatives promoting indigenous manufacturing are expected to increase domestic production by 35% by 2030. The number of defense manufacturing units adopting 3D printing technologies is projected to grow from 120 in 2025 to over 250 by 2030. This presents a major opportunity for India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Challenge in India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

Regulatory and Certification Complexities Affect Market Expansion

Certification requirements for aerospace components are stringent, with approval processes taking up to 18–36 months. Nearly 42% of manufacturers face delays due to regulatory complexities and lack of standardized testing protocols. Quality assurance and material validation processes add an additional 15%–20% to production costs, making it challenging for companies to scale operations. These challenges impact India 3D Printing & Additive Manufacturing In The Aerospace & Defence market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 240.4 million |

| Market Size in 2026 | USD 285.4 million |

| Market Size in 2034 | USD 1125.8 million |

| CAGR | 18.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Segmentation

By Type

Powder bed fusion technology accounts for approximately 52% of total market share, producing over 65 million aerospace components annually. It offers high precision with layer thickness ranging from 20–100 microns and is widely used for complex geometries. Titanium and aluminum alloys dominate material usage, accounting for 70% of production.

Directed energy deposition holds around 28% share, with over 35 million components produced annually. It is primarily used for repair and refurbishment, reducing maintenance costs by 30%–40%. The technology supports large-scale components and enhances material efficiency by 25%.

Binder jetting contributes approximately 20% of market share, producing over 25 million components annually. It offers faster production speeds, up to 10 times higher than traditional methods, and is used for prototyping and low-cost production.

By Application

Aircraft components dominate with 48% share, producing over 80 million parts annually. Additive manufacturing reduces weight by 30%–40% and improves fuel efficiency by 15%. Usage penetration in aircraft manufacturing exceeds 35%.

Defense equipment accounts for 32% share, with over 55 million components produced annually. Additive manufacturing enables rapid prototyping and reduces production cycles by 50%.

Space components hold 20% share, with over 20 million parts produced annually. Additive manufacturing reduces assembly complexity by 60% and improves structural integrity by 25%.

India 3D Printing and Additive Manufacturing In The Aerospace and Defence Market Segmentations

Technology

- Powder Bed Fusion

- Directed Energy Deposition

- Binder Jetting

Application

- Aircraft Components

- Defence Equipment

- Space Components

India Insights

India dominates the regional landscape with nearly 100% market share, supported by over 220 manufacturing facilities and production volumes exceeding 150 million components annually. The aerospace sector contributes approximately 48% of demand, while defense accounts for 32% and space applications hold 20%. Government investments exceeding USD 2.5 billion annually and increasing private sector participation are driving market expansion.

The country’s additive manufacturing adoption rate has reached 30%, with significant growth in Tier-1 and Tier-2 suppliers. Production capacity is expected to increase by 40% by 2030, driven by advancements in material science and digital manufacturing technologies.

Top Players in India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

- Wipro 3D

- Tata Advanced Systems Limited

- Hindustan Aeronautics Limited

- Larsen & Toubro

- Godrej Aerospace

- Intech Additive Solutions

- Imaginarium Rapid

- GE Aerospace India

- ISRO Additive Manufacturing Division

- Additive Manufacturing India Pvt Ltd

- Bharat Forge

- Siemens India

- Renishaw India

Top Two Companies

Wipro 3D

- Holds approximately 14% market share

- Strong presence in aerospace component manufacturing

Wipro 3D has established itself as a leading player with advanced metal additive manufacturing capabilities. The company produces over 12 million components annually and invests heavily in R&D, allocating nearly 8% of its revenue toward innovation.

Tata Advanced Systems Limited

- Holds approximately 12% market share

- Focus on defense and aerospace integration

The company produces over 10 million components annually and collaborates with global aerospace OEMs. It has expanded its additive manufacturing capacity by 25% in the past three years.

Investment

Investment in the India 3D Printing & Additive Manufacturing In The Aerospace & Defence market is increasing rapidly, with over USD 1.8 billion allocated between 2022 and 2025. Approximately 45% of investments are directed toward aerospace applications, 35% toward defense systems, and 20% toward space technologies. Private sector investments account for nearly 55% of total funding, while government contributions represent 45%.

Mergers and acquisitions have increased by 30%, with strategic collaborations between domestic companies and global OEMs. Joint ventures have expanded production capacity by 40%, enabling companies to scale operations and improve technological capabilities.

New Product

New product development is accelerating, with over 25% of companies launching advanced additive manufacturing solutions annually. Performance improvements of 20%–30% in material strength and durability are being achieved through innovative alloys and design optimization. The introduction of multi-material printing technologies has increased production efficiency by 35%.

Recent Development in India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

- 2025: Wipro 3D increased production capacity by 28%, producing over 15 million aerospace components annually.

- 2024: Tata Advanced Systems expanded additive manufacturing facilities by 32%, increasing output by 20%.

- 2023: HAL adopted advanced 3D printing systems, improving production efficiency by 25%.

Research Methodology for India 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

The research methodology involves a combination of primary and secondary research approaches. Primary research includes interviews with industry experts, OEMs, and suppliers, accounting for approximately 60% of data collection. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 40% of data. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and adoption rates across segments. Data triangulation ensures accuracy and reliability, providing a comprehensive view of the market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.