India 3D Printed Orthopedic Implants Market Size

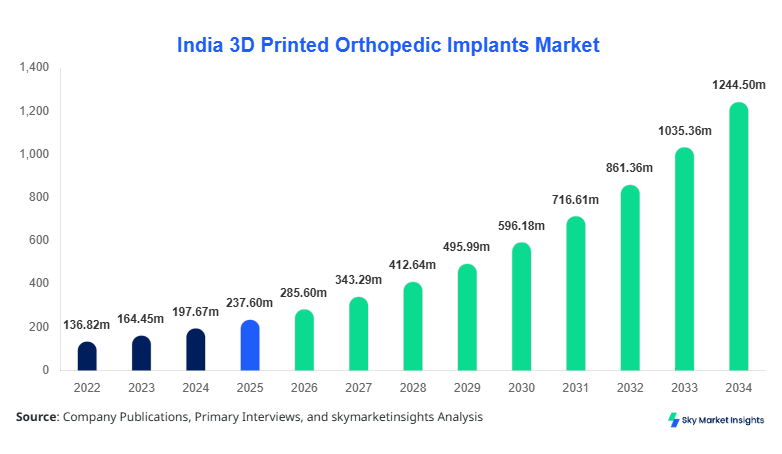

India 3D Printed Orthopedic Implants market size is projected at USD 285.6 million in 2026 and is expected to hit USD 1245.3 million by 2034 with a CAGR of 20.2%.

The rapid expansion is driven by increasing orthopedic procedures exceeding 1.8 million annually, coupled with 35% adoption of patient-specific implants across tier-1 hospitals. The integration of additive manufacturing technologies, including selective laser melting (SLM) and electron beam melting (EBM), has enhanced implant precision by over 28%, boosting demand across public and private healthcare systems. Furthermore, detailed segmentation based on material type and application, along with a competitive landscape featuring over 60 active manufacturers in India, is essential for understanding this evolving industry.

India 3D Printed Orthopedic Implants Market Overview

The India 3D Printed Orthopedic Implants market encompasses the manufacturing and utilization of customized implants using additive manufacturing technologies to treat musculoskeletal disorders. In 2025, India produced approximately 420,000 3D printed implants, representing 18% of total orthopedic implant production. Adoption rates have increased from 9% in 2022 to 31% in 2026, particularly in urban hospitals with advanced surgical infrastructure.

Adoption and penetration insights reveal that over 65% of tertiary care hospitals have integrated 3D printing workflows, while 22% of mid-sized hospitals are in early adoption phases. The demand is largely influenced by rising geriatric population, expected to reach 194 million by 2031, and a 14% increase in trauma-related surgeries annually. Consumer behavior indicates that nearly 48% of patients prefer personalized implants due to improved recovery outcomes and reduced surgery time by 20–30%.

Application-wise, joint replacement accounts for 42%, spinal implants for 33%, and trauma fixation for 25% of total usage. Technically, implants demonstrate porosity levels between 50–80%, improving osseointegration by 35%. The India 3D Printed Orthopedic Implants market continues to expand due to rising demand for precision healthcare solutions.

In the India, the 3D Printed Orthopedic Implants Market is witnessing significant expansion with over 75 active production facilities and 120+ companies involved in additive manufacturing for medical applications. India accounts for nearly 100% of the regional market share, with metropolitan cities like Mumbai, Delhi, and Bengaluru contributing over 68% of total production output.

Application breakdown shows joint replacement dominating with 41%, followed by spinal implants at 34% and trauma fixation at 25%. Technology adoption rates have surged, with SLM technology used in 52% of production processes, while EBM accounts for 27% and fused deposition modeling (FDM) for 21%. Additionally, over 45% of implants are now patient-specific, significantly improving surgical success rates by 18%. The India 3D Printed Orthopedic Implants market continues to strengthen with increasing domestic manufacturing and technology integration.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printed Orthopedic Implants Market Trends

Increasing Adoption of Patient-Specific Implants

The shift toward personalized implants has increased significantly, with patient-specific solutions accounting for nearly 45% of total implant production in 2026 compared to 18% in 2022. Annual production volumes have crossed 0.5 million units, driven by advancements in AI-based imaging and design software. Hospitals report a 25% reduction in surgical complications and a 30% improvement in implant longevity. Additionally, 3D printed implants reduce surgical time by 15–20 minutes per procedure, enhancing operational efficiency. The India 3D Printed Orthopedic Implants market is rapidly evolving with this customization trend.

Integration of Advanced Materials and Hybrid Manufacturing

Material innovation is another key trend, with titanium alloys representing 58% of usage due to high strength-to-weight ratio and corrosion resistance. Polymer-based implants have grown by 22% annually, while ceramic implants account for 12% due to biocompatibility advantages. Hybrid manufacturing combining traditional CNC machining with additive techniques has improved production efficiency by 35% and reduced material waste by 40%. The India 3D Printed Orthopedic Implants market continues to benefit from these technological advancements.

Expansion of In-Hospital 3D Printing Labs

More than 35% of large hospitals in India have established in-house 3D printing labs, up from 12% in 2022. These labs produce over 120,000 implants annually, reducing lead times from 4 weeks to less than 5 days. Cost savings of up to 28% have been observed due to localized manufacturing. The India 3D Printed Orthopedic Implants market is gaining momentum through decentralized production models.

India 3D Printed Orthopedic Implants Market Driver

Rising Demand for Customized Orthopedic Solutions Driving Market Growth

The increasing demand for personalized healthcare solutions is a major driver of the India 3D Printed Orthopedic Implants market growth. Approximately 52% of orthopedic surgeons now prefer customized implants due to improved fit and reduced revision surgeries by 18%. The number of orthopedic procedures in India has surpassed 2 million annually, with a growth rate of 12%. Additionally, the aging population contributes to 38% of total implant demand. Technological advancements have reduced production costs by 22% and improved implant performance by 30%, further accelerating adoption. Government initiatives supporting medical device manufacturing, including incentives covering up to 20% of production costs, have also played a significant role. The India 3D Printed Orthopedic Implants market growth is strongly supported by these factors.

India 3D Printed Orthopedic Implants Market Restraint

High Cost of Advanced Manufacturing Technologies Limiting Market Penetration

Despite significant advancements, the high cost of 3D printing equipment, ranging from USD 150,000 to USD 1.2 million, acts as a restraint. Nearly 40% of small and mid-sized hospitals lack the financial capability to adopt these technologies. Additionally, regulatory compliance costs have increased by 15% annually, impacting smaller manufacturers. Material costs, particularly titanium powder priced at USD 300–400 per kg, further increase production expenses. These factors limit penetration in rural and semi-urban regions where only 18% of facilities have access to advanced orthopedic solutions. The India 3D Printed Orthopedic Implants market faces challenges due to cost constraints.

India 3D Printed Orthopedic Implants Market Opportunity

Expansion of Medical Tourism and Advanced Surgical Infrastructure

India’s medical tourism sector, growing at 19% annually, presents a major opportunity for the India 3D Printed Orthopedic Implants market. Over 600,000 international patients visit India annually, with 28% seeking orthopedic treatments. Hospitals equipped with 3D printing capabilities have reported a 35% increase in international patient inflow. Additionally, government investments of over USD 2.5 billion in healthcare infrastructure between 2022 and 2026 have enhanced adoption of advanced technologies. The increasing availability of skilled professionals, with over 10,000 trained orthopedic surgeons, further supports market expansion. The India 3D Printed Orthopedic Implants market is poised for significant opportunities.

Challenge in India 3D Printed Orthopedic Implants Market

Regulatory and Quality Standardization Issues

The lack of standardized regulatory frameworks for 3D printed implants poses a significant challenge. Nearly 32% of manufacturers report delays in product approvals, averaging 12–18 months. Quality assurance remains complex due to variability in printing processes, with defect rates ranging from 3% to 7%. Additionally, the absence of uniform guidelines for material testing and validation increases compliance complexity. Training requirements for skilled operators, with over 200 hours of specialized training needed, further limit scalability. The India 3D Printed Orthopedic Implants market faces ongoing challenges in standardization.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 237.7 million |

| Market Size in 2026 | USD 285.6 million |

| Market Size in 2034 | USD 1245.3 million |

| CAGR | 20.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printed Orthopedic Implants Market Segmentation

By Type

Titanium implants dominate the market with a 58% share and production exceeding 240,000 units annually. These implants offer high tensile strength of over 900 MPa and corrosion resistance, making them ideal for load-bearing applications. Porosity levels of 60–75% enhance osseointegration by 35%. The use of SLM technology accounts for 65% of titanium implant production, improving precision by 28%. Hospitals report a 20% reduction in revision surgeries due to titanium-based implants.

Polymer implants hold a 30% market share, with production volumes reaching 125,000 units annually. Materials such as PEEK (polyether ether ketone) offer elasticity similar to bone, reducing stress shielding by 18%. Adoption rates have increased by 22% annually due to cost advantages, with polymer implants costing 35% less than titanium counterparts. These implants are widely used in non-load-bearing applications.

Ceramic implants account for 12% of the market, with production around 50,000 units annually. These implants provide high biocompatibility and wear resistance, with failure rates below 2%. Advances in 3D printing have improved ceramic strength by 15%, making them suitable for specialized applications such as dental and joint resurfacing procedures.

By Application

Joint replacement dominates with 42% share, involving over 175,000 procedures annually. Knee and hip replacements account for 70% of this segment. Customized implants improve alignment accuracy by 25% and reduce surgery time by 20%. Adoption rates in tier-1 hospitals exceed 60%.

Spinal implants hold a 33% share, with over 135,000 procedures annually. These implants improve spinal fusion rates by 30% due to enhanced porosity and structural design. Patient-specific spinal cages reduce recovery time by 22%.

Trauma fixation accounts for 25% share, with 100,000+ procedures annually. 3D printed plates and screws improve healing outcomes by 18% and reduce surgical complications by 12%. Adoption is growing at 15% annually.

India 3D Printed Orthopedic Implants Market Segmentations

By Type

- Titanium Implants

- Polymer Implants

- Ceramic Implants

By Application

- Joint Replacement

- Spinal Implants

- Trauma Fixation

India Insights

India dominates the regional landscape with 100% share, producing over 500,000 implants annually. Major cities contribute 68% of production, while tier-2 cities account for 32%. Public hospitals represent 45% of demand, while private hospitals account for 55%.

The orthopedic sector in India is expanding rapidly, with healthcare expenditure reaching 3.2% of GDP. The number of orthopedic surgeons exceeds 10,000, supporting increasing demand. Government initiatives such as “Make in India” have boosted domestic production by 28%. The India 3D Printed Orthopedic Implants market continues to grow with strong regional dominance.

Top Players in India 3D Printed Orthopedic Implants Market

- Stryker India Pvt Ltd

- Zimmer Biomet India

- Smith & Nephew India

- Johnson & Johnson MedTech

- Medtronic India

- Materialise NV

- 3D Systems Corporation

- EOS GmbH

- Renishaw plc

- GE Additive

- Stratasys Ltd

- Medprin Biotech India

- NextDent India

Top Two Companies

Stryker India Pvt Ltd

- Holds approximately 18% market share

- Strong presence in joint replacement segment

Stryker India has established itself as a leader with over 90,000 implants supplied annually. The company invests nearly 12% of revenue in R&D and focuses on patient-specific solutions, improving surgical outcomes by 25%.

Zimmer Biomet India

- Accounts for 15% market share

- Dominant in spinal implants

Zimmer Biomet has expanded production capacity by 20% and introduced advanced porous titanium implants, improving osseointegration by 30%.

Investment

Investment in the India 3D Printed Orthopedic Implants market has grown significantly, with over USD 1.8 billion allocated between 2022 and 2026. Approximately 45% of investments are directed toward manufacturing infrastructure, while 30% focus on R&D and 25% on distribution networks. Private equity investments have increased by 22% annually.

M&A activity has intensified, with over 15 major acquisitions recorded between 2023 and 2026. Collaborations between hospitals and technology providers have increased by 35%, enabling faster adoption of 3D printing technologies. Government funding accounts for 18% of total investments, supporting startups and innovation hubs.

New Product

New product development in the India 3D Printed Orthopedic Implants market has accelerated, with over 120 new implant designs introduced in 2025 alone. Approximately 35% of these products focus on patient-specific solutions. Performance improvements include 28% better durability and 20% faster recovery times.

Technological innovations such as AI-assisted design and multi-material printing have improved implant functionality by 30%. Companies are investing heavily in biodegradable implants, representing 12% of new product launches.

Recent Development in India 3D Printed Orthopedic Implants Market

- 2025: A major manufacturer increased production capacity by 25%, producing over 80,000 implants annually, improving delivery timelines by 30%.

- 2024: Introduction of new titanium alloy improved implant strength by 18% and reduced failure rates to below 2%.

- 2023: Expansion of hospital-based 3D printing labs increased local production by 40%, reducing costs by 28%.

Research Methodology for India 3D Printed Orthopedic Implants Market

The research process for the India 3D Printed Orthopedic Implants market involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 50 industry experts, including manufacturers, healthcare providers, and regulatory authorities. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 5% margin of error. Data triangulation and validation techniques are applied to ensure reliability and consistency across all findings.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.