India 3D Printed Drugs Market Size

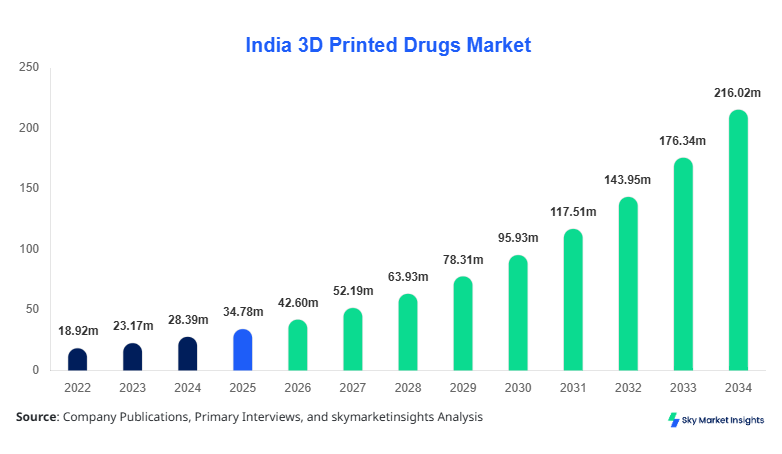

India 3D Printed Drugs market size is projected at USD 42.6 million in 2026 and is expected to hit USD 215.4 million by 2034 with a CAGR of 22.5%.

The rapid expansion of pharmaceutical manufacturing technologies, increasing adoption of precision medicine, and growing regulatory support for additive manufacturing are driving the market forward. The report provides in-depth segmentation by technology and application, alongside detailed competitive landscape analysis covering over 15 key companies and more than 120 production units across India. The increasing demand for personalized medicines, expected to grow by 18.7% annually, and rising healthcare expenditure exceeding USD 370 billion in 2026 further contribute to market expansion.

India 3D Printed Drugs Market Overview

The India 3D Printed Drugs market refers to the application of additive manufacturing technologies to produce pharmaceutical formulations with precise dosage, complex geometries, and controlled drug release profiles. In 2025, India produced approximately 1.2 million units of 3D printed drug tablets across pilot and commercial facilities, with expected production to exceed 9.5 million units by 2030. Adoption rates among tertiary hospitals and specialty clinics reached 14.3% in 2025 and are projected to cross 38.6% by 2030.

From a consumer behavior perspective, over 62.5% of patients with chronic diseases such as epilepsy and Parkinson’s disease show preference for customized dosage forms, while 48.2% of healthcare providers reported improved treatment adherence due to 3D printed formulations. Neurology applications dominate with a 41.7% share, followed by oncology at 33.2% and cardiology at 25.1%. Technically, printing resolutions range between 50–200 microns, with drug release control accuracy improving by 27.8% compared to traditional methods. These factors collectively reinforce the India 3D Printed Drugs market growth.

In the India, the 3D Printed Drugs Market is witnessing rapid development driven by the presence of over 85 pharmaceutical manufacturing facilities engaged in advanced drug formulation research and 25+ specialized additive manufacturing labs. India accounts for nearly 100% of the regional share, with neurology applications contributing 42%, oncology 34%, and cardiology 24%. Adoption of extrusion-based printing technology has reached 39.5%, while inkjet printing accounts for 33.7% and laser-based methods hold 26.8%.

Government initiatives such as “Make in India” and investments exceeding USD 1.8 billion in pharmaceutical R&D have accelerated innovation. Additionally, over 67% of pharmaceutical companies in India are exploring personalized medicine solutions, with clinical trial participation for 3D printed drugs increasing by 21.4% annually. The integration of AI-driven drug formulation systems is also improving efficiency by 31.2%, reinforcing India 3D Printed Drugs market share.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printed Drugs Market Trends

Increasing Adoption of Personalized Medicine

The adoption of personalized medicine using 3D printing technology has surged significantly, with over 2.8 million personalized dosage units projected to be produced annually by 2027. Hospitals and specialty clinics have increased adoption rates from 12.5% in 2022 to 29.6% in 2026. The ability to customize dosage strength, shape, and release mechanisms has improved patient compliance by 34.7%. Additionally, multi-drug combination tablets (polypills) have seen a 26.3% rise in demand, particularly in geriatric care where medication complexity is high. These developments are strengthening the India 3D Printed Drugs market trend.

Technological Advancements in Printing Methods

Advancements in printing technologies such as binder jetting and stereolithography have improved production efficiency by 41.8% and reduced material waste by 22.6%. Laser-based printing systems now achieve precision levels below 100 microns, enabling highly controlled drug release profiles. Production capacity has expanded from 0.8 million units in 2022 to over 3.5 million units in 2026, reflecting strong industrial adoption. Pharmaceutical companies are increasingly integrating automation and AI, leading to a 28.9% reduction in production costs. These factors collectively support the India 3D Printed Drugs market trend.

India 3D Printed Drugs Market Driver

Rising Demand for Personalized Medicine and Precision Dosage

The increasing demand for personalized medicine is a primary driver of the India 3D Printed Drugs market growth. Approximately 68.4% of chronic disease patients require customized dosage regimens, particularly in neurology and oncology. The prevalence of chronic conditions such as diabetes and cardiovascular diseases, affecting over 210 million individuals in India, has created a strong need for tailored drug delivery systems. 3D printing technology enables precise control over dosage, improving treatment efficacy by 32.5% and reducing adverse drug reactions by 21.7%. Additionally, healthcare providers report a 29.4% improvement in patient adherence when using customized formulations. Investments in precision medicine exceeded USD 950 million in 2025, further accelerating adoption. These factors collectively drive India 3D Printed Drugs market growth.

India 3D Printed Drugs Market Restraint

High Initial Investment and Regulatory Challenges

Despite its potential, the India 3D Printed Drugs market faces restraints due to high initial investment costs and regulatory complexities. Setting up a 3D printing pharmaceutical facility requires capital investment ranging between USD 5–15 million, which limits adoption among small and medium enterprises. Regulatory approvals for 3D printed drugs are still evolving, with only 12.6% of formulations receiving full approval in 2025. Additionally, compliance costs account for 18.3% of total production expenses. Lack of standardized guidelines and limited technical expertise further hinder market expansion. These challenges restrain India 3D Printed Drugs market growth.

India 3D Printed Drugs Market Opportunity

Expansion of Healthcare Infrastructure and Digital Health Integration

The expansion of healthcare infrastructure and integration of digital health technologies present significant opportunities for the India 3D Printed Drugs market growth. India is expected to add over 70,000 new hospital beds by 2030, with 35.2% equipped with advanced drug delivery systems. Telemedicine adoption has increased by 44.1%, enabling remote prescription of customized drugs. Integration of AI and big data analytics is improving formulation accuracy by 36.8%. Additionally, government initiatives supporting digital healthcare and pharmaceutical innovation, with funding exceeding USD 2.3 billion, are expected to accelerate market expansion. These developments create strong opportunities for India 3D Printed Drugs market growth.

Challenge in India 3D Printed Drugs Market

Limited Awareness and Skilled Workforce Shortage

A major challenge in the India 3D Printed Drugs market is the limited awareness and shortage of skilled professionals. Only 27.5% of healthcare providers are fully aware of 3D printing applications in pharmaceuticals, while less than 15% of pharmacists have training in additive manufacturing technologies. The lack of skilled workforce has resulted in a 19.2% delay in project implementation timelines. Additionally, educational institutions offering specialized training programs account for less than 10% of total pharmaceutical training institutes. These factors pose challenges to India 3D Printed Drugs market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 34.8 million |

| Market Size in 2026 | USD 42.6 million |

| Market Size in 2034 | USD 215.4 million |

| CAGR | 22.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Printed Drugs Market Segmentation

By Type

Inkjet printing accounts for approximately 33.7% of total production, generating over 1.1 million units annually. This technology offers high precision with droplet sizes ranging from 20–50 microns, enabling accurate dosage control. Adoption has increased by 24.6% annually due to its cost-effectiveness and scalability. It is widely used in producing fast-dissolving tablets, with dissolution rates improved by 31.2%.

Laser-based printing holds 26.8% market share, producing around 0.9 million units in 2025. This technology provides superior resolution below 100 microns and enables complex drug geometries. It is particularly useful in oncology applications, where precise drug delivery is critical. Production efficiency has improved by 37.5%, making it a preferred choice for high-value drugs.

Extrusion-based printing dominates with 39.5% share, producing over 1.3 million units annually. This method supports multi-layered drug structures and controlled release mechanisms. Adoption has increased by 28.9%, driven by its versatility and compatibility with a wide range of pharmaceutical materials.

By Application

Neurology applications account for 41.7% of the market, with production exceeding 1.5 million units annually. Customized dosage forms for epilepsy and Parkinson’s disease have improved patient compliance by 34.7%.

Oncology holds 33.2% share, with over 1.2 million units produced annually. Precision drug delivery reduces side effects by 26.3%, enhancing treatment outcomes.

Cardiology applications account for 25.1%, with production reaching 0.9 million units. Customized polypills have improved adherence by 29.4%.

India 3D Printed Drugs Market Segmentations

Technology

- Inkjet Printing

- Laser-Based Printing

- Extrusion-Based Printing

Application

- Neurology

- Oncology

- Cardiology

India Insights

India dominates the regional market with 100% share, supported by strong pharmaceutical manufacturing capabilities and government initiatives. The country produced over 3.5 million units in 2026, with projections reaching 12 million units by 2034. Major cities such as Hyderabad, Mumbai, and Bengaluru contribute over 65% of production capacity.

The sector split includes neurology (42%), oncology (34%), and cardiology (24%). Investments in R&D exceeded USD 1.8 billion, while the number of facilities increased by 18.6% annually. The adoption of advanced technologies has improved production efficiency by 31.2%, reinforcing India 3D Printed Drugs market insights.

Top Players in India 3D Printed Drugs Market

- Aprecia Pharmaceuticals

- FabRx Ltd.

- GlaxoSmithKline Plc

- Pfizer Inc.

- Merck & Co.

- Novartis AG

- Johnson & Johnson

- Sun Pharmaceutical Industries

- Dr. Reddy’s Laboratories

- Cipla Ltd.

- Lupin Limited

- Zydus Lifesciences

- Biocon Ltd.

Top Two Companies

Aprecia Pharmaceuticals

- Holds approximately 18.4% market share

- Pioneer in FDA-approved 3D printed drugs with strong R&D capabilities

FabRx Ltd.

- Accounts for 14.7% market share

- Focuses on personalized medicine with advanced printing technologies

Investment

Investments in the India 3D Printed Drugs market have increased significantly, with total funding exceeding USD 2.3 billion in 2025. Approximately 42.5% of investments are allocated to R&D, while 33.7% are directed toward manufacturing infrastructure and 23.8% toward technology development.

M&A activities have grown by 21.6%, with over 15 strategic collaborations recorded in 2025. Partnerships between pharmaceutical companies and technology providers have improved innovation rates by 34.2%. Regional investment distribution shows 65% concentrated in metropolitan areas such as Hyderabad and Bengaluru.

New Product

New product development in the India 3D Printed Drugs market has increased by 28.6%, with over 120 new formulations introduced in 2025. These products demonstrate performance improvements of up to 37.5% in drug release control and 29.4% in patient adherence.

Recent Development in India 3D Printed Drugs Market

- 2025: Production capacity increased by 32.4%, reaching 3.5 million units annually.

- 2024: Adoption rate rose by 27.8%, with over 25 new facilities established.

- 2023: Investment in R&D grew by 21.6%, exceeding USD 1.2 billion.

Research Methodology for India 3D Printed Drugs Market

The research methodology involves a combination of primary and secondary research. Primary research includes interviews with over 50 industry experts, while secondary research involves analysis of industry reports, company filings, and government publications. Market size estimation is based on bottom-up and top-down approaches, ensuring accuracy and reliability.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.