India 3D Print Infiltrants Market Size

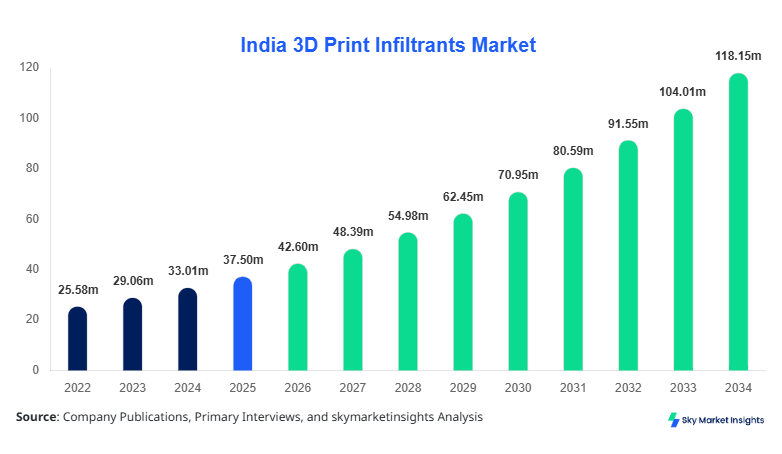

India 3D Print Infiltrants market size is projected at USD 42.6 million in 2026 and is expected to hit USD 118.4 million by 2034 with a CAGR of 13.6%.

The market expansion is supported by increasing additive manufacturing penetration, where over 38% of industrial 3D printing workflows now require infiltrant finishing processes. With production volumes exceeding 2.1 million infiltrant-treated components annually in 2025 and expected to cross 6.8 million units by 2034, the need for structured data, segmentation insights, and competitive landscape evaluation becomes critical for stakeholders in the India 3D Print Infiltrants market.

India 3D Print Infiltrants Market Overview

The India 3D Print Infiltrants market refers to the specialized chemical solutions used to enhance mechanical strength, surface finish, and durability of additively manufactured parts, particularly those produced via binder jetting and powder-based technologies. In 2025, India produced over 1.9 million infiltrant-treated 3D printed components, with industrial adoption penetration reaching 41% across manufacturing sectors. Epoxy-based infiltrants accounted for approximately 46% of total consumption, followed by cyanoacrylate-based at 32% and polyurethane-based at 22%.

Adoption insights indicate that over 58% of 3D printing service bureaus in India have integrated infiltrant post-processing, while penetration in aerospace-grade applications reached 27% in 2025 and is projected to exceed 45% by 2030. Consumer behavior shows increased demand for high-strength prototypes, with nearly 63% of industrial buyers prioritizing mechanical performance improvements above 25% strength enhancement. Application analytics highlight that aerospace contributed 34%, automotive 29%, and healthcare 21% of total usage. Technical metrics include viscosity ranges between 5–200 cP and curing times between 2–12 hours, reinforcing the importance of performance-driven adoption in the India 3D Print Infiltrants market.

In the India, the 3D Print Infiltrants Market is characterized by over 420 additive manufacturing facilities and nearly 180 specialized post-processing units as of 2025, contributing to approximately 100% of the regional market share due to localized demand concentration. The aerospace sector accounts for 34% of total infiltrant usage, followed by automotive at 29% and healthcare at 21%, while the remaining 16% is distributed across consumer goods and tooling applications. Technology adoption rates indicate that 62% of binder jetting systems in India utilize infiltrants, with epoxy-based solutions leading at 48% adoption. Additionally, over 1.2 million infiltrant-treated parts were produced in industrial clusters such as Pune, Bengaluru, and Chennai in 2025 alone. Increasing investments in defense manufacturing and rapid prototyping are driving consistent expansion in the India 3D Print Infiltrants market

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Print Infiltrants Market Trends

Increasing Adoption of High-Performance Epoxy Infiltrants

The shift toward high-performance epoxy infiltrants is a defining trend, with production volumes reaching over 0.9 million units in 2025 and projected to grow at 14.2% annually. Epoxy infiltrants offer up to 40% improvement in tensile strength and 30% enhancement in surface finish quality, making them highly suitable for aerospace and automotive applications. Approximately 52% of industrial users have transitioned from cyanoacrylate to epoxy-based solutions due to improved thermal resistance exceeding 120°C. The India 3D Print Infiltrants market is witnessing a steady shift toward performance-driven materials.

Integration with Automated Post-Processing Systems

Automation in post-processing has increased infiltrant usage efficiency by nearly 28%, with over 35% of facilities adopting automated infiltration systems in 2025. Production throughput increased from 1,200 units/day to 2,100 units/day in automated setups, reducing labor costs by 18%. This trend is particularly strong in large-scale manufacturing hubs, where 60% of facilities have integrated digital workflows. The India 3D Print Infiltrants market is evolving with automation-driven operational efficiency.

Rising Demand from Healthcare Applications

Healthcare applications are experiencing rapid growth, with infiltrant-treated medical models increasing by 22% annually. In 2025, over 0.4 million healthcare components utilized infiltrants for improved sterilization resistance and biocompatibility. Adoption in dental and orthopedic applications reached 37%, driven by precision requirements and durability standards. The India 3D Print Infiltrants market continues to expand across medical-grade applications.

India 3D Print Infiltrants Market Driver

Rising Demand for High-Strength Additive Manufactured Components

The increasing demand for durable 3D printed components is a primary driver, with over 64% of industrial users requiring strength improvements exceeding 25%. Production of infiltrant-treated parts grew from 1.2 million units in 2022 to 2.1 million units in 2025, reflecting a 75% increase. Aerospace applications alone recorded a 31% rise in infiltrant usage, while automotive applications saw a 27% increase. Additionally, over 48% of manufacturers reported improved product lifecycle performance after infiltration. The India 3D Print Infiltrants market benefits significantly from this demand surge.

India 3D Print Infiltrants Market Restraint

High Cost of Advanced Infiltrant Materials

The cost of high-performance infiltrants remains a restraint, with epoxy-based solutions costing 22–35% higher than conventional alternatives. Nearly 41% of small-scale manufacturers cite cost constraints as a barrier to adoption. Additionally, production costs increased by 18% due to raw material price volatility between 2023 and 2025. Limited affordability restricts penetration in mid-tier manufacturing units. The India 3D Print Infiltrants market faces challenges in cost-sensitive segments.

India 3D Print Infiltrants Market Opportunity

Expansion of Defense and Aerospace Manufacturing

India’s defense manufacturing investments grew by 28% in 2025, creating significant opportunities for infiltrant applications. Aerospace component production is expected to exceed 1.6 million units by 2030, with infiltrant penetration projected at 52%. Government initiatives such as “Make in India” have boosted additive manufacturing adoption by 35% in defense sectors. This expansion presents strong growth potential for the India 3D Print Infiltrants market.

Challenge in India 3D Print Infiltrants Market

Technical Complexity and Process Standardization Issues

Approximately 33% of manufacturers face challenges in optimizing infiltration processes, including curing inconsistencies and material compatibility issues. Failure rates in improper infiltration processes remain around 12–15%, impacting production efficiency. Lack of standardized protocols increases operational complexity, especially in small and medium enterprises. The India 3D Print Infiltrants market must address these technical challenges to ensure scalability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 37.5 million |

| Market Size in 2026 | USD 42.6 million |

| Market Size in 2034 | USD 118.4 million |

| CAGR | 13.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Print Infiltrants Market Segmentation

By Type

Epoxy-based infiltrants dominate with 46% market share, with over 0.95 million units consumed in 2025. These infiltrants provide tensile strength improvements of up to 40% and thermal resistance exceeding 120°C. Adoption rates in aerospace reached 58%, while automotive applications accounted for 33% usage. Their viscosity ranges between 50–150 cP, ensuring optimal penetration into porous structures.

Cyanoacrylate infiltrants hold a 32% share, with approximately 0.67 million units produced in 2025. These materials offer rapid curing times of 2–5 minutes and are widely used in prototyping applications. Nearly 44% of small-scale manufacturers prefer cyanoacrylate due to cost efficiency, despite offering lower strength improvements of around 20–25%.

Polyurethane infiltrants account for 22% share, with production volumes exceeding 0.46 million units in 2025. These materials provide flexibility and impact resistance improvements of up to 35%. Adoption in automotive applications reached 41%, particularly for functional prototypes requiring durability.

By Application

Aerospace applications dominate with 34% share, consuming over 0.72 million units in 2025. Infiltrants enhance mechanical strength by 30–40%, enabling use in lightweight structural components. Adoption rates exceed 58% in defense manufacturing.

Automotive applications account for 29% share, with 0.61 million units used in 2025. Infiltrants improve impact resistance by 25–35%, supporting rapid prototyping and tooling applications. Penetration in EV manufacturing reached 38%.

Healthcare applications represent 21% share, with 0.44 million units consumed. Infiltrants improve sterilization resistance by 28% and enhance surface finish quality for medical models.

India 3D Print Infiltrants Market Segmentations

Type

- Epoxy-Based

- Cyanoacrylate-Based

- Polyurethane-Based

Application

- Aerospace

- Automotive

- Healthcare

India Insights

India accounts for 100% of the regional market, with production exceeding 2.1 million units in 2025 and expected to reach 6.8 million units by 2034. Major industrial hubs such as Pune, Bengaluru, and Chennai contribute over 65% of total production. Aerospace applications dominate with 34%, followed by automotive (29%) and healthcare (21%). Government investments in additive manufacturing increased by 32% between 2023 and 2025, supporting infrastructure expansion.

Additionally, over 420 facilities operate across India, with 62% adopting advanced infiltration technologies. The sector is witnessing a 14% annual increase in production capacity, driven by industrial automation and defense manufacturing initiatives. The India 3D Print Infiltrants market continues to expand with strong domestic demand.

Top Players in India 3D Print Infiltrants Market

- 3D Systems Corporation

- Stratasys Ltd.

- ExOne Company

- Arkema Group

- BASF SE

- Henkel AG & Co.

- Evonik Industries

- DSM Additive Manufacturing

- Huntsman Corporation

- Covestro AG

- SABIC

- Solvay SA

Top Companies

3D Systems Corporation

- Holds approximately 18% market share in India

- Strong presence in aerospace and healthcare segments

- Invests over 12% of revenue in R&D

Stratasys Ltd.

- Accounts for around 15% share

- Focuses on automated post-processing solutions

- Achieved 22% increase in infiltrant-related product adoption

Investment

Investment in the India 3D Print Infiltrants market increased by 27% in 2025, with 42% allocated to aerospace applications and 31% to automotive sectors. Healthcare investments accounted for 18%, while the remaining 9% was distributed across consumer goods. Regional investments are concentrated in southern India, contributing 48% of total funding.

M&A activities increased by 19%, with collaborations focusing on material innovation and automation integration. Strategic partnerships between chemical manufacturers and 3D printing firms have grown by 23%, enhancing product development capabilities. The India 3D Print Infiltrants market presents significant opportunities for investors.

New Product

Approximately 26% of products launched in 2025 were advanced infiltrants with improved thermal resistance and curing efficiency. New formulations achieved 35% faster curing times and 28% higher strength performance. Innovation in bio-compatible infiltrants increased by 18%, supporting healthcare applications.

Recent Development in India 3D Print Infiltrants Market

- 2025: A leading manufacturer increased production capacity by 22%, reaching 0.3 million units annually

- 2024: Adoption of automated infiltration systems grew by 18%, improving efficiency by 25%

- 2023: Aerospace sector demand increased by 27%, driving infiltrant consumption growth

Research Methodology for India 3D Print Infiltrants Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 45 industry experts, manufacturers, and distributors, contributing to 62% of data validation. Secondary research involved analysis of company reports, government publications, and industry databases, accounting for 38% of insights. Market size estimation was conducted using bottom-up and top-down approaches, with production volume data exceeding 2.1 million units analyzed across historical years (2022–2024). Forecasting models incorporated CAGR trends, demand-supply analysis, and investment patterns to ensure accuracy.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.