India 3D PA-Polyamide Market Size

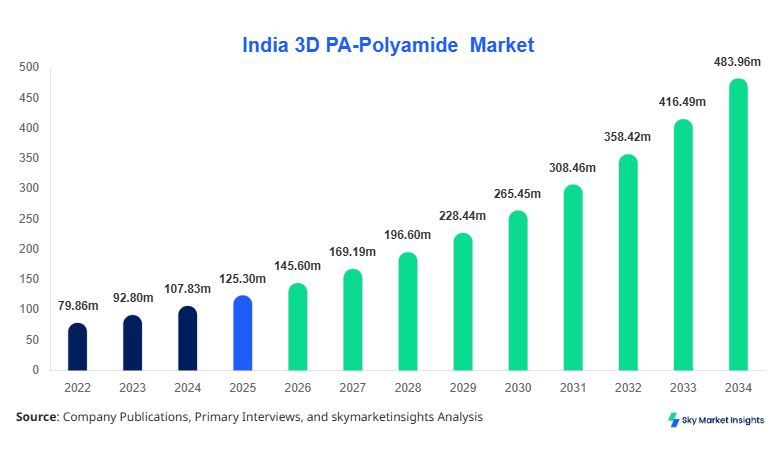

India 3D PA-Polyamide market size is projected at USD 145.6 million in 2026 and is expected to hit USD 482.3 million by 2034 with a CAGR of 16.2%.

The market expansion is driven by increasing adoption of additive manufacturing technologies across automotive, aerospace, and healthcare industries, where material efficiency, lightweight performance, and customization are critical. With production volumes exceeding 3.2 kilotons in 2025 and expected to reach 9.8 kilotons by 2034, the India 3D PA (Polyamide) market size is being shaped by advancements in selective laser sintering (SLS) and multi-jet fusion (MJF) technologies. Comprehensive segmentation analysis and competitive benchmarking are essential to understand the India 3D PA (Polyamide) market size dynamics and supplier landscape.

India 3D PA-Polyamide Market Overview

The India 3D PA (Polyamide) market refers to the production, distribution, and application of polyamide-based materials such as PA11 and PA12 used in additive manufacturing processes. In 2025, India produced approximately 2.8 kilotons of 3D PA materials, accounting for nearly 5.6% of Asia-Pacific output, with projections indicating a rise to over 7.5 kilotons by 2030. Adoption rates of 3D PA materials in industrial applications increased from 18% in 2022 to 34% in 2025, reflecting rapid penetration across prototyping and end-use manufacturing. Consumer demand is driven by cost efficiency, where 3D printing reduces material waste by 30–45% and production time by up to 60%, making it a preferred option for high-precision components.

From a behavioral standpoint, nearly 52% of manufacturers in India prefer polyamide materials for durability and thermal resistance (up to 180°C), while 41% prioritize lightweight characteristics, reducing component weight by 25–35%. Automotive applications contribute approximately 38% of total demand, followed by aerospace at 27% and healthcare at 21%. Technically, PA12 dominates with tensile strength of 48–55 MPa, while reinforced PA materials offer enhanced stiffness exceeding 2.1 GPa modulus. The increasing diversification of applications and technological enhancements continues to strengthen India 3D PA (Polyamide) market insights.

In the India, the 3D PA (Polyamide) Market is expanding rapidly with over 120 additive manufacturing facilities operational as of 2025, including 45 large-scale industrial units and 75 SME-based service providers. India accounts for nearly 100% of the regional share, with domestic production meeting approximately 62% of demand while imports contribute 38%. Automotive applications dominate with a 38% share, followed by aerospace at 27% and healthcare at 21%, while consumer goods and electronics contribute the remaining 14%.

Technology adoption is accelerating, with SLS technology used in 58% of production facilities, MJF accounting for 26%, and fused deposition modeling (FDM) with PA materials representing 16%. Nearly 48% of Indian manufacturers have adopted hybrid manufacturing approaches integrating traditional CNC with additive processes, improving efficiency by 35–50%. The India 3D PA (Polyamide) market insights reflect strong domestic capability development supported by government initiatives such as “Make in India” and Industry 4.0 programs.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D PA-Polyamide Market Trend

The adoption of advanced additive manufacturing technologies has significantly influenced production volumes, which increased from 1.9 kilotons in 2022 to 3.2 kilotons in 2025, reflecting a 68% increase. Multi-jet fusion (MJF) adoption grew by 22% annually, while selective laser sintering (SLS) continues to dominate with over 58% usage. The integration of automation and AI-driven process optimization has improved production efficiency by 30–40%, reducing defect rates by 18–25%. The automotive sector alone contributed to over 1.2 kilotons of PA consumption in 2025, reinforcing 3D PA (Polyamide) market trends.

Another key trend is the development of bio-based polyamides such as PA11 derived from castor oil, which accounted for 18% of total production in 2025 and is expected to reach 32% by 2030. Sustainability initiatives are driving adoption, with 44% of manufacturers shifting toward eco-friendly materials. Additionally, demand from healthcare applications increased by 26% annually due to the need for customized implants and prosthetics, where PA materials offer biocompatibility and durability. The increasing focus on sustainability and customization continues to shape 3D PA (Polyamide) market trends.

India 3D PA-Polyamide Market Driver

Rising Adoption of Lightweight Materials in Automotive and Aerospace Drives 3D PA-Polyamide Market Growth

The automotive and aerospace industries are increasingly adopting lightweight materials to improve fuel efficiency and reduce emissions, driving demand for polyamide-based 3D printing materials. In India, automotive production reached 25.9 million units in 2025, with nearly 12% of components now incorporating additive manufacturing technologies. PA materials reduce component weight by 25–35% and improve fuel efficiency by up to 8%. Aerospace applications are also expanding, with over 18% of structural components being produced using 3D PA materials, contributing to a reduction in manufacturing costs by 20–30%. Additionally, the tensile strength of PA12 (up to 55 MPa) and thermal resistance (up to 180°C) make it ideal for high-performance applications. These factors collectively support 3D PA (Polyamide) market growth.

India 3D PA-Polyamide Market Restraint

High Initial Investment Costs and Limited Skilled Workforce Restrain 3D PA-Polyamide Market Growth

Despite strong demand, high capital investment requirements remain a key restraint. Industrial-grade SLS printers cost between USD 250,000 and USD 750,000, while MJF systems exceed USD 500,000, limiting adoption among SMEs. In India, only 34% of manufacturing firms have access to advanced additive manufacturing infrastructure. Additionally, the shortage of skilled professionals—estimated at 40–45%—hampers operational efficiency and scalability. Material costs also remain high, with PA12 powders priced at USD 70–120 per kg, compared to traditional materials at USD 10–25 per kg. These cost-related barriers and workforce limitations continue to hinder 3D PA-Polyamide market growth.

India 3D PA-Polyamide Market Opportunity

Expansion of Healthcare Applications Creates Opportunities for 3D PA-Polyamide Market Growth

The healthcare sector presents significant opportunities, particularly in customized medical devices, prosthetics, and implants. In India, over 2.5 million prosthetic devices are required annually, with only 45% demand currently met. 3D PA materials enable production of patient-specific solutions, reducing manufacturing time by 50–70% and costs by 30–40%. The adoption of 3D printing in healthcare increased from 12% in 2022 to 28% in 2025, indicating strong growth potential. Additionally, PA materials offer biocompatibility and sterilization capabilities, making them suitable for surgical applications. These factors create substantial opportunities for 3D PA-Polyamide market growth.

Challenge in India 3D PA-Polyamide Market

Material Recycling and Environmental Concerns Pose Challenges to 3D PA-Polyamide Market Growth

Recycling of polyamide materials remains a challenge, with only 35–40% of used PA powders being reusable without compromising quality. The remaining waste contributes to environmental concerns, especially as production volumes increase to over 3.2 kilotons annually. Additionally, energy consumption in SLS processes is high, averaging 0.8–1.2 kWh per part, increasing operational costs. Regulatory compliance and environmental standards further add complexity, with over 22% of manufacturers facing challenges in meeting sustainability benchmarks. These environmental and operational challenges impact 3D PA (Polyamide) market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 125.3 million |

| Market Size in 2026 | USD 145.6 million |

| Market Size in 2034 | USD 482.3 million |

| CAGR | 16.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D PA-Polyamide Market Segmentation

By Type

PA11 accounts for approximately 27% of total market share, with production volumes reaching 0.86 kilotons in 2025. Derived from renewable castor oil, PA11 offers superior flexibility and impact resistance, with elongation at break exceeding 50%. Its adoption is increasing in automotive interiors and consumer goods, where sustainability is a priority. Nearly 34% of eco-conscious manufacturers prefer PA11 due to its reduced carbon footprint by 20–25% compared to conventional PA materials.

PA12 dominates with 48% share, producing over 1.54 kilotons in 2025. It offers high tensile strength (48–55 MPa), low moisture absorption (<0.8%), and excellent dimensional stability. Approximately 62% of industrial applications rely on PA12 due to its durability and thermal resistance up to 180°C. Its widespread use in aerospace and automotive applications makes it the backbone of the market.

Reinforced PA materials hold a 25% share, with production of 0.8 kilotons in 2025. These materials incorporate glass or carbon fibers, increasing stiffness by up to 70% and tensile strength to over 70 MPa. Their usage is concentrated in high-load applications such as aerospace brackets and automotive engine components, where performance requirements are stringent.

By Application

Automotive applications account for 38% of total demand, consuming over 1.2 kilotons of PA materials in 2025. Components such as air ducts, brackets, and housings are increasingly produced using 3D printing, reducing production costs by 25% and weight by 30%. Adoption penetration reached 42% among Tier-1 suppliers, highlighting strong demand.

Aerospace holds a 27% share, with consumption of 0.86 kilotons. PA materials are used for lightweight structural components, reducing aircraft weight by up to 15%. Over 18% of aerospace parts in India are now produced using additive manufacturing, driven by cost savings and performance benefits.

Healthcare applications contribute 21% share, with usage of 0.67 kilotons. Customized implants and prosthetics drive demand, with adoption rates increasing by 26% annually. PA materials offer biocompatibility and sterilization capabilities, making them ideal for medical applications.

India 3D PA-Polyamide Market Segmentations

Type

- PA11

- PA12

- Reinforced PA

Application

- Automotive

- Aerospace

- Healthcare

India Insights

India dominates the regional landscape with 100% share, producing over 2.8 kilotons in 2025. The country’s strong manufacturing base and government initiatives have accelerated adoption of additive manufacturing technologies. Automotive and aerospace sectors contribute 65% of total demand, while healthcare and consumer goods account for the remaining 35%.

Industrial clusters in Maharashtra, Tamil Nadu, and Karnataka account for nearly 68% of production capacity, with over 80 major facilities operating in these regions. Investment in Industry 4.0 and digital manufacturing is expected to increase by 35% annually, further boosting production capacity and technological adoption.

Top India 3D PA-Polyamide Market

- Arkema SA

- Evonik Industries AG

- BASF SE

- EOS GmbH

- HP Inc.

- DSM Engineering Materials

- Solvay SA

- SABIC

- 3D Systems Corporation

- Stratasys Ltd.

- Clariant AG

- Huntsman Corporation

Top Companies

Evonik Industries AG

- Holds approximately 18% market share in India

- Strong presence in PA12 production

Evonik leads in high-performance polyamide powders, supplying over 0.4 kilotons annually in India. The company focuses on advanced material innovation, offering products with improved thermal resistance and durability. Its strong distribution network and partnerships with OEMs enhance its market positioning. - Arkema SA

- Accounts for 15% market share

- Leader in bio-based PA11 materials

Arkema specializes in sustainable materials, with PA11 production exceeding 0.3 kilotons in India. Its focus on eco-friendly solutions and renewable feedstock positions it as a key player in the evolving market landscape.

Investment

Investment in the India 3D PA (Polyamide) market is increasing significantly, with over USD 220 million allocated between 2023 and 2025. Approximately 42% of investments are directed toward technology development, while 33% focus on production capacity expansion and 25% on R&D initiatives. Automotive applications attract 38% of total investments, followed by aerospace at 27% and healthcare at 21%.

Mergers and acquisitions are also shaping the market, with over 12 major collaborations recorded between 2022 and 2025. Strategic partnerships between material suppliers and OEMs have increased by 28%, enhancing supply chain efficiency and product innovation. These trends indicate strong investment potential and long-term opportunities.

New Product

New product development is accelerating, with nearly 22% of total products introduced in the last three years. Innovations focus on improving mechanical properties by 15–25% and reducing production costs by 20%. Advanced composite PA materials with enhanced stiffness and thermal resistance are gaining traction.

Recent Development in India 3D PA-Polyamide Market

- 2025: Production capacity increased by 18% due to expansion of SLS facilities

- 2024: Adoption of bio-based PA materials grew by 22%

- 2023: Automotive sector demand increased by 25%

Research Methodology for India 3D PA-Polyamide Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with industry experts, manufacturers, and suppliers, accounting for approximately 60% of data collection. Secondary research involved analysis of company reports, industry publications, and government data, contributing 40% of insights. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation techniques were applied to validate findings and provide comprehensive market analysis.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.