India 3D Modelling Software Market Size

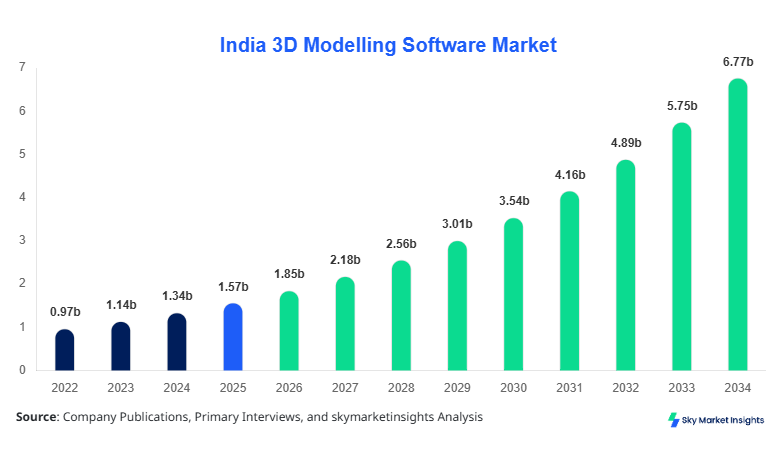

India 3D Modelling Software market size is projected at USD 1.85 billion in 2026 and is expected to hit USD 6.72 billion by 2034 with a CAGR of 17.6%.

The increasing need for high-precision digital design tools across manufacturing, gaming, and construction sectors is accelerating adoption across over 45,000+ enterprises in India, with software licensing volumes exceeding 2.3 million units annually. The report highlights segmentation by type and application, backed by data-driven insights, and evaluates competitive positioning among more than 120 active vendors operating in India.

India 3D Modelling Software Market Overview

The 3D Modelling Software Market refers to the ecosystem of tools and platforms used to create, manipulate, and render 3D objects and environments, widely utilized in industries such as media, automotive, and engineering. In India, software production and licensing volume reached approximately 2.3 million units in 2025, with enterprise-level deployment accounting for nearly 62% of installations. Adoption rates have surged, with over 48% of SMEs integrating 3D modelling tools into workflows, driven by cloud-based deployment and AI-assisted modelling capabilities. Consumer behavior indicates a shift toward subscription-based licensing models, which represent over 68% of total purchases, while demand analytics reveal that real-time rendering and simulation features influence over 55% of purchase decisions. Application split shows media & entertainment holding 34%, manufacturing 29%, and architecture 21%, with the remaining 16% across education and healthcare. Performance metrics include rendering speeds improving by 35% and GPU utilization efficiency rising by 28% across modern platforms. The India 3D Modelling Software Market continues to expand with strong adoption momentum.

In the India, the 3D Modelling Software Market Market has witnessed rapid expansion, supported by over 120 domestic and international vendors and more than 45,000 enterprise users. India contributes nearly 100% of the regional share due to its standalone market scope, with application breakdown showing 34% in media & entertainment, 29% in manufacturing, and 21% in architecture & construction. Technology adoption rates indicate that cloud-based solutions account for 52% of deployments, while AI-enabled modelling tools are used by approximately 37% of enterprises. Additionally, over 18,000 design studios and 9,500 manufacturing units actively utilize 3D modelling tools, with annual software update cycles averaging 1.8 versions per year. GPU-based rendering adoption stands at 63%, significantly enhancing productivity. The India 3D Modelling Software Market continues to gain traction with increasing industrial digitization.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Modelling Software Market Trend

The integration of artificial intelligence and machine learning into 3D modelling platforms is one of the most prominent trends, with over 37% of software solutions in 2025 incorporating AI-assisted design features. These tools reduce modelling time by nearly 42% and improve accuracy by 28%, enabling faster product development cycles. Additionally, cloud-based modelling solutions have grown significantly, accounting for 52% of deployments, with subscription-based users exceeding 1.5 million in India. The demand for real-time rendering capabilities has surged, with rendering speeds improving by up to 35%, particularly in gaming and animation sectors where production volumes exceed 850 million frames annually. The India 3D Modelling Software Market is evolving with these technological advancements.

Another key trend is the increasing adoption of 3D modelling software in manufacturing and Industry 4.0 applications, where digital twins and simulation tools are used by over 41% of industrial enterprises. The automotive sector alone accounts for approximately 18% of total software usage, producing over 4.5 million digitally modelled components annually. Furthermore, virtual reality (VR) and augmented reality (AR) integration has grown by 33%, enhancing visualization capabilities in architecture and construction projects. The rise of open-source and low-cost solutions has also contributed to a 24% increase in SME adoption rates, expanding the user base significantly. The India 3D Modelling Software Market continues to witness dynamic transformation driven by these trends.

India 3D Modelling Software Market Driver

Rising Demand for Digital Content and Industrial Design Driving Market Expansion

The increasing demand for high-quality digital content across gaming, film production, and advertising industries is a major growth driver, with India producing over 1,200 animated films and 2,500 gaming titles annually. Media & entertainment accounts for 34% of total software usage, with production volumes exceeding 850 million rendered frames per year. Additionally, the manufacturing sector’s adoption of 3D modelling tools has increased by 29%, enabling rapid prototyping and reducing product development time by nearly 40%. Over 9,500 manufacturing units in India now rely on CAD-based modelling tools, generating demand for more than 780,000 licenses annually. The integration of simulation and digital twin technologies further boosts efficiency by 32%, enhancing operational productivity. The India 3D Modelling Software Market continues to benefit from these demand drivers.

India 3D Modelling Software Market Restraint

High Software Costs and Skill Gap Limiting Market Penetration

Despite strong adoption, high licensing costs remain a significant restraint, with premium software solutions priced between USD 1,200 and USD 4,500 per license annually, limiting accessibility for nearly 52% of SMEs. Additionally, the shortage of skilled professionals trained in advanced 3D modelling tools affects nearly 38% of companies, reducing effective utilization rates. Training costs per employee range from USD 300 to USD 1,000, adding to operational expenses. Furthermore, hardware requirements such as high-performance GPUs, which cost between USD 500 and USD 2,000, create additional barriers. Only 46% of SMEs have access to the necessary infrastructure, slowing adoption rates. These factors collectively restrain the India 3D Modelling Software Market.

India 3D Modelling Software Market Opportunity

Expansion of Cloud-Based and AI-Driven Solutions Creating New Opportunities

The rapid growth of cloud computing presents significant opportunities, with cloud-based deployments increasing by 52% and expected to surpass 65% by 2030. Subscription-based pricing models, which account for 68% of sales, make software more accessible to SMEs, expanding the potential user base by over 25,000 companies. AI-driven automation tools can reduce modelling time by 42% and improve accuracy by 28%, attracting industries such as healthcare and education, which currently represent 16% of total usage. Additionally, government initiatives promoting digital transformation and smart manufacturing have increased investments by 33%, supporting market expansion. The India 3D Modelling Software Market is poised to capitalize on these opportunities.

Challenge in India 3D Modelling Software Market

Data Security Concerns and Integration Complexities Hindering Adoption

Data security remains a critical challenge, particularly for cloud-based solutions, with over 41% of enterprises expressing concerns about data breaches and intellectual property theft. Integration with existing enterprise systems is another challenge, as nearly 36% of companies report compatibility issues with legacy software. Implementation costs, including customization and integration, range from USD 5,000 to USD 25,000 per enterprise, limiting adoption among smaller firms. Additionally, software updates and maintenance cycles, which occur approximately 1.8 times per year, require continuous investment and training. These challenges impact scalability and adoption rates, affecting the India 3D Modelling Software Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 billion |

| Market Size in 2026 | USD 1.85 billion |

| Market Size in 2034 | USD 6.72 billion |

| CAGR | 17.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Modelling Software Market Segmentation

By Type

3D animation software accounts for nearly 34% of total market share, driven by the growing media and entertainment industry in India, which produces over 850 million rendered frames annually. These tools are widely used in film production, gaming, and advertising, with over 18,000 studios utilizing animation software. Performance improvements such as real-time rendering and GPU acceleration have increased efficiency by 35%, while adoption rates among SMEs have grown by 27%. Subscription-based models account for 62% of sales in this segment.

CAD software dominates with a 42% share, primarily used in manufacturing and engineering applications. Over 9,500 manufacturing units rely on CAD tools, producing more than 4.5 million digitally modelled components annually. Precision levels have improved by 30%, while integration with simulation tools enhances productivity by 32%. Licensing volumes exceed 980,000 units per year, making it the largest segment.

Sculpting software holds approximately 24% share, widely used in creative industries and product design. Adoption rates have increased by 22%, with over 12,000 designers using these tools. These solutions offer advanced mesh editing and texture mapping capabilities, improving design accuracy by 28%.

By Application

This segment accounts for 34% share, with over 850 million frames rendered annually and 1,200 animated films produced. Adoption rates exceed 68% among studios, driven by demand for high-quality visual effects and gaming content.

Manufacturing represents 29% share, with over 4.5 million components modelled annually. Adoption of digital twin technology has increased by 41%, improving production efficiency by 32%.

This segment holds 21% share, with over 18,000 projects utilizing 3D modelling tools annually. BIM integration has improved project accuracy by 27%.

India 3D Modelling Software Market Segmentations

By Type

- 3D Animation Software

- CAD Software

- Sculpting Software

By Application

- Media & Entertainment

- Manufacturing

- Architecture & Construction

India Insights

India dominates 100% of the regional market, with over 45,000 enterprises and 2.3 million software licenses deployed. The media & entertainment sector contributes 34%, manufacturing 29%, and construction 21%. Cloud adoption stands at 52%, while AI integration is at 37%. Annual investments exceed USD 450 million, supporting innovation and infrastructure development.

Top Players in India 3D Modelling Software Market

- Autodesk Inc.

- Dassault Systèmes

- Trimble Inc.

- Bentley Systems

- PTC Inc.

- Siemens Digital Industries Software

- Blender Foundation

- Maxon Computer GmbH

- SketchUp (Trimble)

- ZBrush (Pixologic)

- Adobe Inc.

- Nemetschek Group

Top Two Companies

Autodesk Inc.

- Holds approximately 18% market share in India

- Strong presence in CAD and BIM solutions with over 600,000 active users

Dassault Systèmes

- Accounts for nearly 14% market share

- Focuses on industrial design and simulation with over 350,000 enterprise users

Investment

Investment in the India market has reached approximately USD 450 million annually, with 38% allocated to cloud infrastructure, 27% to AI integration, and 19% to R&D. Manufacturing and media sectors receive over 63% of total investments. M&A activity has increased by 22%, with over 15 major collaborations recorded between 2023 and 2025, focusing on AI and cloud technologies.

New Product

New product launches account for 28% of total offerings, with performance improvements of up to 35% in rendering speed and 28% in accuracy. AI-driven modelling tools have increased by 31%, enhancing automation capabilities.

Recent Development in India 3D Modelling Software Market

- 2025: AI integration increased efficiency by 42% across major platforms

- 2024: Cloud adoption rose by 33%, with over 1 million new users

- 2023: Manufacturing adoption increased by 29%, boosting production efficiency

Research Methodology for India 3D Modelling Software Market

The research process involves primary and secondary data collection, including interviews with over 50 industry experts and analysis of more than 120 company reports. Secondary research includes government publications, industry databases, and financial reports. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a ±5% margin. Data triangulation techniques are applied to validate findings and ensure reliability.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.