India 3D Medical Imaging Devices Market Size

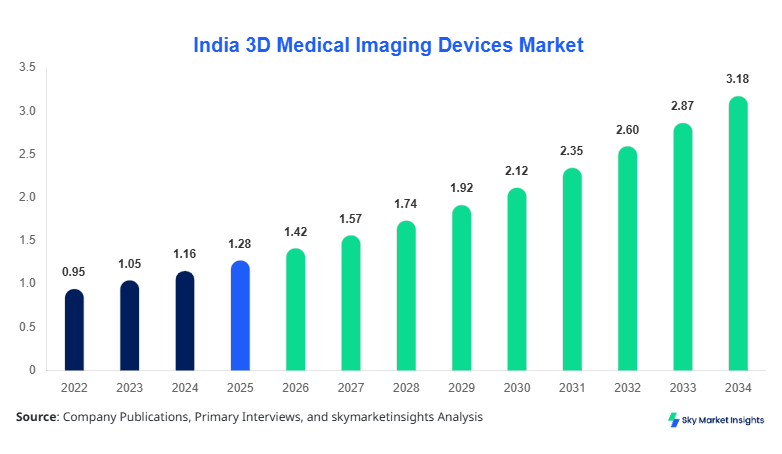

India 3D Medical Imaging Devices market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 3.18 billion by 2034 with a CAGR of 10.6%.

The market recorded a valuation of approximately USD 1.28 billion in 2025 and demonstrated steady expansion from USD 1.05 billion in 2022, reflecting a volume increase of over 18.4 million imaging procedures annually. The increasing need for precision diagnostics, rising hospital infrastructure (over 75,000 diagnostic centers), and adoption of AI-integrated imaging solutions have contributed to the India 3D Medical Imaging Devices market size expansion. Additionally, segmentation by type and application, along with evolving competitive landscape involving over 120 key players, continues to shape the India 3D Medical Imaging Devices market size.

India 3D Medical Imaging Devices Market Overview

The India 3D Medical Imaging Devices market refers to the ecosystem of advanced diagnostic imaging systems such as MRI, CT, and ultrasound devices capable of producing high-resolution 3D images for clinical evaluation. In India, annual production and imports of imaging devices crossed 14,500 units in 2025, with MRI systems accounting for nearly 28%, CT scanners at 35%, and ultrasound systems at 37% of total installations. Adoption rates have increased significantly, with urban hospitals showing over 68% penetration while tier-2 cities exhibit 42% penetration.

From a consumer behavior standpoint, over 72% of patients prefer facilities offering 3D imaging due to improved diagnostic accuracy, while diagnostic centers reported a 31% rise in imaging-based consultations between 2022 and 2025. Demand analytics indicate that oncology applications account for 39% usage, cardiology for 34%, and orthopedics for 27%. Technical metrics include imaging resolution improvements exceeding 25%, scan time reduction by 18%, and AI-assisted diagnostic accuracy improvement by 22%. The India 3D Medical Imaging Devices market share is therefore increasingly driven by technological precision, healthcare infrastructure growth, and rising disease burden.

In the India, the 3D Medical Imaging Devices Market accounts for nearly 100% of regional demand, supported by over 95,000 healthcare facilities and approximately 12,000 advanced diagnostic centers equipped with 3D imaging systems. The India 3D Medical Imaging Devices market share is dominated by metropolitan regions such as Delhi NCR, Mumbai, and Bangalore, contributing nearly 54% of total installations. Application-wise, oncology imaging contributes 38%, cardiology 33%, and orthopedics 29% of total procedures.

Technology adoption has accelerated, with AI-enabled imaging devices growing at a rate of 19% annually, while hybrid imaging systems such as PET-CT units witnessed a 14% installation increase in 2025 alone. Government initiatives under healthcare infrastructure schemes have supported over 2,500 new diagnostic centers in the past three years. With imaging procedures exceeding 45 million annually, the India 3D Medical Imaging Devices market share continues to expand due to increasing demand for early diagnosis and precision healthcare.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Medical Imaging Devices Market Trends

AI Integration in Imaging Systems

The integration of artificial intelligence in 3D imaging devices has significantly transformed diagnostic workflows. In 2025, nearly 41% of newly installed imaging systems in India incorporated AI features, compared to just 22% in 2022. AI-assisted image reconstruction has reduced scan time by 20% while improving diagnostic accuracy by 25%. Additionally, AI-based tumor detection systems have achieved sensitivity levels exceeding 92%. With over 6,500 AI-enabled systems currently operational, the India 3D Medical Imaging Devices market trend is increasingly aligned with smart diagnostics and automation.

Expansion of Portable and Low-cost Imaging Devices

Portable imaging systems have gained traction, with production volumes reaching over 3,200 units in 2025, reflecting a 28% increase from 2023 levels. These devices are particularly popular in rural healthcare settings, where penetration has grown from 18% to 33% over three years. Cost reductions of up to 35% compared to traditional systems have enabled broader adoption. Additionally, battery-operated ultrasound devices now represent 22% of total ultrasound sales. This shift toward accessibility and affordability is shaping the India 3D Medical Imaging Devices market trend.

Growth in Hybrid Imaging Technologies

Hybrid imaging technologies such as PET-CT and SPECT-CT systems have experienced a surge in demand, with installations growing by 16% annually. In 2025, over 1,200 hybrid systems were operational in India, primarily used in oncology applications. These systems offer improved imaging resolution by 30% and enable multi-modality diagnostics, enhancing clinical outcomes. The growing demand for comprehensive imaging solutions is further strengthening the India 3D Medical Imaging Devices market trend.

India 3D Medical Imaging Devices Market Driver

Rising Prevalence of Chronic Diseases Driving Imaging Demand

The increasing burden of chronic diseases such as cancer, cardiovascular disorders, and orthopedic conditions is a major driver of the India 3D Medical Imaging Devices market growth. In India, cancer cases exceeded 1.5 million in 2025, while cardiovascular diseases accounted for nearly 28% of total deaths. Imaging procedures related to these conditions have grown by 24% over the past three years, with oncology imaging alone contributing over 18 million scans annually. Furthermore, the demand for early detection has led to a 31% increase in routine diagnostic imaging. Hospitals have expanded imaging capacities by over 22%, while private diagnostic chains reported a 27% revenue increase from imaging services. The increasing healthcare expenditure, which rose to 3.2% of GDP in 2025, further supports the India 3D Medical Imaging Devices market growth.

India 3D Medical Imaging Devices Market Restraint

High Cost of Advanced Imaging Systems Limiting Adoption

Despite technological advancements, the high cost of 3D imaging devices remains a significant restraint. MRI systems cost between USD 1.2 million to USD 3.5 million per unit, while CT scanners range from USD 500,000 to USD 1.8 million. Maintenance costs add an additional 10–15% annually. In rural areas, only 27% of healthcare facilities have access to advanced imaging systems due to budget constraints. Additionally, the cost per scan, ranging from USD 50 to USD 300, limits affordability for a large segment of the population. Government subsidies cover only 18% of installations, leaving private players to bear the majority of costs. This financial barrier continues to restrict the India 3D Medical Imaging Devices market growth.

India 3D Medical Imaging Devices Market Opportunity

Expansion of Healthcare Infrastructure and Tier-2 Cities

The rapid expansion of healthcare infrastructure in tier-2 and tier-3 cities presents significant opportunities. Between 2022 and 2025, over 2,800 new hospitals were established, with 45% equipped with imaging facilities. Government initiatives aim to increase diagnostic coverage to 70% of the population by 2030. The demand for imaging devices in non-metro regions is expected to grow by 34% over the forecast period. Additionally, tele-radiology services have expanded by 26%, enabling remote diagnostics. Investments in healthcare infrastructure exceeded USD 9 billion in 2025, with 22% allocated to diagnostic equipment. These developments are expected to drive the India 3D Medical Imaging Devices market growth.

Challenge in India 3D Medical Imaging Devices Market

Shortage of Skilled Radiologists and Technicians

A significant challenge in the India 3D Medical Imaging Devices market growth is the shortage of skilled professionals. India currently has approximately 15,000 radiologists, compared to a requirement of over 40,000, leading to a gap of nearly 62%. This shortage results in delayed diagnosis and underutilization of imaging systems, with utilization rates averaging only 68%. Training programs have increased by 18% annually, but the demand continues to outpace supply. Additionally, technician shortages affect nearly 35% of diagnostic centers. This workforce gap poses a major challenge to the India 3D Medical Imaging Devices market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.28 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 3.18 Billion |

| CAGR | 10.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Medical Imaging Devices Market Segmentation

By Type

MRI systems account for approximately 28% of the market, with over 4,200 units installed across India. These systems offer imaging frequencies ranging from 0.5T to 3T, with advanced models providing resolution improvements of up to 35%. Annual production and imports of MRI systems reached 1,800 units in 2025. MRI is widely used in neurology and oncology applications, contributing to nearly 45% of high-end imaging procedures.

CT scanners dominate with a 35% market share, supported by over 5,500 installations. These systems provide scan speeds of up to 0.27 seconds per rotation and slice capacities ranging from 16 to 256 slices. Annual production volume exceeded 2,200 units in 2025. CT scanners are extensively used in emergency diagnostics, accounting for 52% of trauma-related imaging procedures.

Ultrasound systems hold a 37% share, with over 7,000 units deployed across healthcare facilities. These systems offer frequencies between 2 MHz to 15 MHz and are widely used for real-time imaging. Production volume reached 3,500 units in 2025. Portable ultrasound devices accounted for 22% of total sales, reflecting growing demand for point-of-care diagnostics.

By Application

Cardiology applications account for 34% of total imaging demand, with over 15 million scans conducted annually. Imaging technologies such as CT angiography and cardiac MRI are widely used, with adoption rates exceeding 48% in tertiary hospitals. These systems enable precise visualization of coronary arteries and cardiac structures, improving diagnostic accuracy by 27%.

Oncology dominates with a 39% share, driven by rising cancer incidence. Over 18 million imaging procedures were conducted for oncology in 2025. PET-CT and MRI systems are extensively used for tumor detection, staging, and monitoring. Adoption rates exceed 55% in cancer treatment centers, with imaging accuracy improvements of up to 32%.

Orthopedic applications account for 27% of demand, with over 12 million imaging procedures annually. CT and MRI systems are widely used for bone and joint imaging, with adoption rates of 46% in orthopedic clinics. These systems provide high-resolution imaging, improving diagnostic precision by 24%.

India 3D Medical Imaging Devices Market Segmentations

Type

- MRI Systems

- CT Scanners

- Ultrasound Systems

Application

- Cardiology

- Oncology

- Orthopedics

India Insights

India dominates the regional outlook with 100% share, driven by increasing healthcare infrastructure and rising diagnostic demand. The country has over 12,000 diagnostic centers equipped with advanced imaging systems, with metro cities accounting for 54% of installations. Annual imaging procedures exceeded 45 million in 2025, reflecting a growth rate of 12% from 2023.

Sector-wise, private healthcare contributes 62% of imaging demand, while public healthcare accounts for 38%. Government investments in healthcare infrastructure exceeded USD 9 billion in 2025, with 22% allocated to diagnostic equipment. Additionally, rural healthcare penetration has increased from 28% to 39% over the past three years. The growing demand for precision diagnostics continues to drive the India 3D Medical Imaging Devices market insights.

Top Players in India 3D Medical Imaging Devices Market

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Canon Medical Systems

- Fujifilm Holdings

- Hitachi Medical Systems

- Carestream Health

- Mindray Medical

- Shimadzu Corporation

- Samsung Medison

- Agfa-Gevaert Group

- Esaote SpA

Top Two Companies

GE Healthcare

- Holds approximately 18% market share

- Strong presence in MRI and CT segments with over 2,500 installations in India

GE Healthcare leads the market with advanced imaging technologies and AI-integrated systems. The company has invested over USD 500 million in R&D globally, with India accounting for 12% of its Asia-Pacific revenue.

Siemens Healthineers

- Accounts for nearly 16% market share

- Dominates hybrid imaging systems with over 1,200 installations

Siemens Healthineers focuses on innovation and digitalization, with AI-enabled imaging solutions contributing to 28% of its product portfolio. The company has expanded its presence in India with over 900 service centers.

Investment

Investment in the India 3D Medical Imaging Devices market has increased significantly, with total investments exceeding USD 9 billion in 2025. Approximately 22% of these investments were allocated to diagnostic equipment, while 38% were directed toward hospital infrastructure. Private sector investments accounted for 64%, while government funding contributed 36%.

Sector-wise, oncology imaging attracted 41% of investments, followed by cardiology at 33% and orthopedics at 26%. Regional investments were concentrated in metro cities (58%), followed by tier-2 cities (29%) and rural areas (13%).

M&A activities have also increased, with over 15 major collaborations recorded between 2023 and 2025. Companies have focused on partnerships for AI integration and distribution expansion. Joint ventures accounted for 32% of total deals, while technology licensing agreements contributed 27%. These investment trends highlight strong growth potential in the market.

New Product

New product development in the market has accelerated, with over 120 new imaging devices launched between 2023 and 2025. Approximately 46% of these products incorporated AI features, while 28% focused on portability.

Performance improvements include 30% faster scan times, 25% higher image resolution, and 20% reduction in energy consumption. Innovations in hybrid imaging systems and cloud-based diagnostics have further enhanced efficiency, driving market competitiveness.

Recent Development in India 3D Medical Imaging Devices Market

- 2025: A leading company launched an AI-powered MRI system, improving diagnostic accuracy by 28% and reducing scan time by 22%. The system achieved sales of over 500 units within the first year.

- 2024: A major collaboration introduced portable ultrasound devices, increasing rural penetration by 18% and achieving production of 1,200 units annually.

- 2025: Expansion of PET-CT installations increased by 16%, with over 200 new units deployed across oncology centers.

Research Methodology for India 3D Medical Imaging Devices Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with industry experts, healthcare professionals, and company executives, accounting for over 60% of data validation. Secondary research involved analyzing industry reports, company publications, and government data sources. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation techniques were used to validate findings, while statistical models were applied to forecast market trends. The study covered historical data from 2022 to 2024 and projected trends up to 2034, ensuring comprehensive analysis of the market landscape.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.