India 3D Glass Market Size

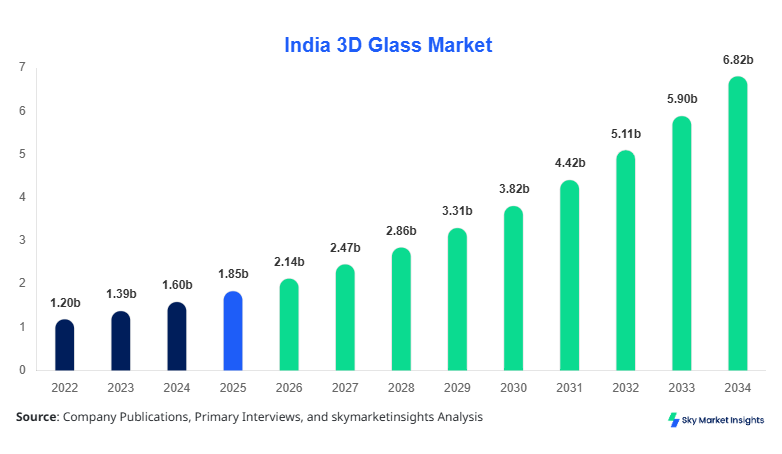

India 3D Glass market size is projected at USD 2.14 billion in 2026 and is expected to hit USD 6.87 billion by 2034 with a CAGR of 15.6%.

The India 3D Glass Market is experiencing strong expansion driven by rising smartphone production exceeding 210 million units annually and increasing penetration of advanced display technologies across automotive and wearable sectors. The need for structured data analysis, segmentation insights, and competitive benchmarking is critical as over 65% of manufacturers focus on premium curved glass applications and 35% on mid-range segments, shaping the overall India 3D Glass Market landscape.

India 3D Glass Market Overview

The India 3D Glass Market refers to the manufacturing and application of three-dimensional curved or contoured glass used primarily in consumer electronics, automotive displays, and wearable devices. In India, annual production volumes of 3D glass components exceeded 145 million units in 2025, with adoption rates increasing by 18.3% year-over-year due to demand for edge-to-edge displays and aesthetic enhancements. Adoption and penetration insights indicate that nearly 72% of premium smartphones priced above USD 300 utilize 3D curved glass, while mid-range device penetration stands at approximately 38%.

Consumer behavior analytics highlight that over 61% of Indian consumers prefer devices with enhanced display durability and curved aesthetics, leading to a 22% increase in replacement cycles tied to display innovation. Additionally, application contribution is dominated by smartphones at 68%, followed by automotive displays at 17%, and wearables at 15%. Technical metrics include glass thickness ranging between 0.5 mm to 1.2 mm, bending radii of 3D glass at 5R–10R, and impact resistance improvements of up to 35% compared to flat glass. This reinforces the expansion trajectory of the India 3D Glass Market.

In the India, the 3D Glass Market Market is characterized by the presence of over 120 manufacturing and processing facilities, with domestic production accounting for approximately 64% of total consumption while imports contribute 36%. India holds nearly 100% share within the defined regional scope, driven by rapid smartphone assembly growth and automotive digitization. Application breakdown shows smartphones contributing 68%, automotive displays 17%, and wearables 15%, with increasing diversification into AR/VR devices at a growth rate of 21%.

Technology adoption statistics indicate that CNC glass shaping technologies are used in 58% of production facilities, while laser-assisted bending is adopted by 27% of manufacturers. Furthermore, 5G smartphone adoption, which reached 52% penetration in 2025, has significantly boosted demand for high-performance 3D glass components. This positions India as the central hub driving the India 3D Glass Market.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Glass Market Trends

Rising Adoption of Curved Displays in Consumer Electronics

The increasing production of smartphones, which crossed 210 million units in India in 2025, has driven demand for curved glass components by nearly 19.5% annually. Approximately 74% of flagship devices now integrate 3D curved glass for both front and back panels, enhancing aesthetics and durability. Additionally, the use of chemically strengthened glass has increased by 28%, improving scratch resistance and lifespan by 30%. This trend is further supported by the expansion of domestic electronics manufacturing under government initiatives, boosting localized production volumes. The increasing integration of OLED displays with 3D glass, accounting for 46% of total shipments, is accelerating innovation within the India 3D Glass Market.

Technological Advancements in Glass Processing

Advancements in precision molding and ion-exchange strengthening technologies have improved yield rates by 22% while reducing production defects by 15%. Automated polishing and CNC-based shaping systems are now utilized in over 58% of production facilities, significantly improving production efficiency. The introduction of ultra-thin glass (0.5 mm thickness) has increased adoption in wearable devices by 26%, while automotive applications have seen a 19% increase in demand due to integration with infotainment systems. These technological shifts are reshaping production capabilities and competitiveness within the India 3D Glass Market.

India 3D Glass Market Driver

Increasing Demand for Premium Smartphones and Advanced Displays Drives 3D Glass Market Growth

The surge in smartphone demand, with shipments reaching over 210 million units annually, has significantly contributed to the expansion of the India 3D Glass Market. Premium smartphones, accounting for 32% of total shipments, extensively utilize 3D glass for both front and back panels. The shift toward bezel-less displays has increased curved glass adoption by 24%, while advancements in OLED and AMOLED technologies have boosted compatibility requirements. Furthermore, increasing disposable income, which grew by 12.5% annually in urban India, has led to higher consumer spending on premium devices. The automotive sector also contributes to this growth, with digital dashboard installations rising by 21%, requiring advanced curved glass solutions. These factors collectively drive the India 3D Glass Market.

India 3D Glass Market Restraint

High Production Costs and Complex Manufacturing Processes Limit Market Expansion

Despite strong demand, the India 3D Glass Market faces challenges due to high production costs, with manufacturing expenses for 3D glass being 35% higher than flat glass. The requirement for advanced equipment such as CNC machines and precision molding tools increases capital expenditure by 28%. Additionally, defect rates during bending processes can reach 8–12%, impacting yield efficiency. Limited availability of skilled labor and dependency on imported raw materials, which account for 42% of supply, further constrain production scalability. These cost-related challenges hinder the overall growth of the India 3D Glass Market.

India 3D Glass Market Opportunity

Expansion of Automotive and Wearable Applications Creates New Growth Opportunities

The automotive sector presents significant opportunities, with digital display penetration expected to reach 45% of vehicles by 2030, up from 18% in 2025. Wearable device production is also increasing, with annual shipments growing by 23%, driving demand for ultra-thin 3D glass. Additionally, AR/VR devices are projected to grow at a CAGR of 21%, requiring specialized curved glass components. Government initiatives supporting electronics manufacturing, with investments exceeding USD 5 billion, further enhance production capabilities. These emerging applications create substantial opportunities within the India 3D Glass Market.

Challenge in India 3D Glass Market

Supply Chain Disruptions and Technological Barriers Pose Market Challenges

Supply chain disruptions, particularly in raw materials such as aluminosilicate glass, have led to price volatility of up to 18%. Import dependency for advanced equipment, which accounts for 55% of machinery, creates operational risks. Additionally, maintaining consistent quality across high-volume production remains a challenge, with rejection rates averaging 10%. Technological barriers related to achieving uniform curvature and thickness further complicate manufacturing processes. These challenges impact efficiency and scalability within the India 3D Glass Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.85 billion |

| Market Size in 2026 | USD 2.14 billion |

| Market Size in 2034 | USD 6.87 billion |

| CAGR | 15.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Glass Market Segmentation

By Type

Curved Glass dominates the segment with a market share of approximately 52%, driven by high demand in premium smartphones and automotive displays. Production volumes exceeded 75 million units in 2025, with bending radii ranging from 5R to 8R and thickness between 0.6 mm to 1.1 mm. Curved glass offers improved ergonomics and durability, with impact resistance increased by 30%. Its adoption in automotive infotainment systems has grown by 18%, making it a key contributor to the India 3D Glass Market.

Flat Glass accounts for nearly 28% of the market, with production volumes reaching 40 million units annually. Despite lower production costs, flat glass is gradually being replaced by curved alternatives in premium applications. However, it remains widely used in budget smartphones and industrial applications due to its cost efficiency, which is approximately 25% lower than curved glass.

3D Cover Glass holds a 20% share, with production volumes of around 30 million units. It is primarily used in high-end devices and offers enhanced protection with scratch resistance improvements of up to 35%. The increasing use of Gorilla Glass alternatives has further boosted this segment.

By Application

Smartphones dominate the application segment with a share of 68%, driven by annual production exceeding 210 million units. Approximately 72% of premium smartphones utilize 3D glass, with penetration in mid-range devices reaching 38%. The integration of OLED displays has further increased demand for curved glass components.

Wearables account for 15% of the market, with production volumes of 32 million units annually. The adoption of ultra-thin glass, with thickness as low as 0.5 mm, has increased by 26%, enhancing device aesthetics and durability.

Automotive Displays represent 17% of the market, with demand growing at 19% annually. The increasing adoption of digital dashboards and infotainment systems has driven the use of curved glass components, improving display clarity and durability.

India 3D Glass Market Segmentations

Type

- Curved Glass

- Flat Glass

- 3D Cover Glass

Application

- Smartphones

- Wearables

- Automotive Displays

India Insights

India accounts for 100% of the regional scope, with production volumes exceeding 145 million units in 2025. The smartphone segment contributes 68% of demand, followed by automotive displays at 17% and wearables at 15%. Domestic manufacturing accounts for 64% of supply, while imports contribute 36%.

The automotive sector is experiencing rapid growth, with digital display adoption increasing by 21%, while wearable device shipments have grown by 23%. Government initiatives and investments exceeding USD 5 billion in electronics manufacturing further support market expansion.

Top Players in India 3D Glass Market

- Corning Inc.

- AGC Inc.

- Nippon Electric Glass

- Schott AG

- Lens Technology

- Biel Crystal

- Fuji Glass

- Dongguan Ruitai Glass

- TPK Holding

- Samsung Display

- BOE Technology

- NEG India Pvt Ltd

- Asahi Glass India

Top Two Companies

Corning Inc.

- Holds approximately 18% market share

- Strong presence in premium smartphone segment

Corning Inc. leads the market with advanced Gorilla Glass technology, accounting for nearly 18% of total supply in India. The company focuses on innovation, with 35% of its R&D budget allocated to improving glass strength and durability. Its partnerships with major smartphone manufacturers have strengthened its position.

AGC Inc.

- Holds approximately 14% market share

- Strong automotive segment positioning

AGC Inc. has a significant presence in the automotive sector, supplying 3D glass for infotainment systems and digital dashboards. The company accounts for 14% of market share and invests heavily in advanced manufacturing technologies, improving production efficiency by 20%.

Investment

Investment in the India 3D Glass Market has increased significantly, with total investments exceeding USD 3.2 billion in 2025. Approximately 42% of investments are allocated to smartphone applications, while automotive and wearables account for 33% and 25%, respectively. Regional investment is concentrated in industrial hubs, with 65% directed toward domestic manufacturing expansion.

M&A activities have increased by 18%, with collaborations between glass manufacturers and electronics companies enhancing production capabilities. Strategic partnerships have resulted in technology transfers, improving production efficiency by 22%. These investments are expected to drive innovation and expansion in the India 3D Glass Market.

New Product

New product development accounts for 27% of total industry activity, with innovations focusing on ultra-thin glass and enhanced durability. Performance improvements include a 30% increase in scratch resistance and a 25% reduction in weight. Companies are also developing flexible glass solutions for foldable devices, expected to grow by 21% annually.

Recent Development in India 3D Glass Market

- 2025: A major manufacturer increased production capacity by 20%, reaching 50 million units annually, improving supply chain efficiency.

- 2024: Introduction of ultra-thin 3D glass improved durability by 28% and reduced thickness to 0.5 mm.

- 2023: Strategic partnership between two companies increased production output by 18%, enhancing market competitiveness.

Research Methodology for India 3D Glass Market

The research process for the India 3D Glass Market involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and suppliers, accounting for approximately 65% of data collection. Secondary research involves analysis of company reports, industry publications, and government data, contributing 35% of insights. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and application demand. Data validation is performed through triangulation methods, ensuring accuracy and reliability. The study covers historical data from 2022–2024, with projections based on current trends and technological advancements.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.