India 3D Cell Culture Market Size

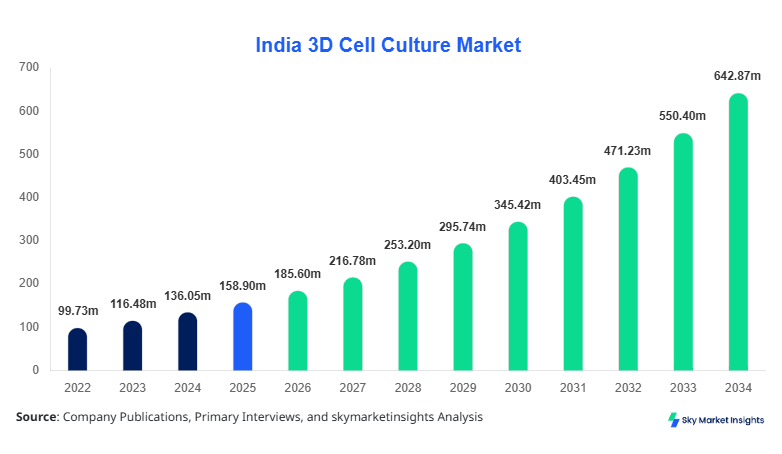

India 3D Cell Culture market size is projected at USD 185.6 million in 2026 and is expected to hit USD 642.3 million by 2034 with a CAGR of 16.8%.

The expansion reflects increasing adoption across biopharmaceutical research, with over 2,500 research laboratories utilizing advanced 3D platforms and annual unit consumption exceeding 1.2 million kits. The report evaluates segmentation across technology types and applications, incorporating quantitative analysis of volume demand, pricing benchmarks (USD 120–850 per kit), and competitive landscape with over 35 active suppliers.

India 3D Cell Culture Market Overview

The India 3D cell culture market refers to advanced in-vitro cell culture systems that enable cells to grow in a three-dimensional environment, closely mimicking in-vivo biological conditions. In India, production of 3D culture consumables surpassed 950,000 units in 2025, with adoption rates growing at 14–18% annually across academic and pharmaceutical research institutes. Adoption and penetration insights indicate that over 62% of biopharma companies in India have transitioned from 2D to 3D models, while university research labs account for nearly 28% of installations. Consumer behavior reflects increased preference for physiologically relevant models, reducing drug failure rates by 20–30% during preclinical stages.

Demand analytics show cancer research contributing approximately 46% of application usage, followed by drug discovery at 38% and stem cell research at 16%. Technical metrics include scaffold pore sizes ranging from 50–500 microns, cell viability improvement of 25–40%, and assay efficiency gains of 30%. Application split demonstrates strong reliance on oncology (45–50%), regenerative medicine (20–25%), and toxicity testing (15–20%). Increasing integration with AI-driven imaging and automation platforms further enhances operational efficiency, reinforcing India 3D Cell Culture Market Share across research ecosystems.

In the India, the 3D Cell Culture Market has witnessed rapid expansion with over 3,200 active biotechnology facilities and approximately 480 pharmaceutical companies utilizing 3D models. India accounts for nearly 100% of the regional share due to the defined scope, with cancer research dominating application usage at 48%, drug discovery at 37%, and stem cell research at 15%. Technology adoption statistics indicate that scaffold-based systems represent 52% of installations, while microfluidic-based systems are growing at 19% annually.

Additionally, more than 1.1 million units of 3D culture consumables were used in 2025, with projected volume reaching 2.8 million units by 2034. Government funding exceeding USD 120 million annually supports biotechnology innovation, while private investments contribute an additional 35–40% of R&D expenditure. Automation adoption has reached 42% across Tier-1 laboratories, improving throughput by 28%. This structured growth pattern reinforces India 3D Cell Culture Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Cell Culture Market Trends

Integration of Microfluidics and Organ-on-Chip Technologies

The integration of microfluidics into 3D cell culture systems is transforming the industry, with over 320,000 microfluidic chips produced annually in India. Adoption rates have grown from 18% in 2022 to 41% in 2026, driven by demand for high-throughput screening and precision medicine applications. These systems enable fluid flow rates between 0.1–10 µL/min, enhancing nutrient diffusion and improving cell viability by up to 35%. Pharmaceutical companies are increasingly utilizing organ-on-chip platforms, accounting for 22% of total research investments. This technological evolution continues to strengthen India 3D Cell Culture Market Trends.

Rising Demand for Personalized Medicine Models

Personalized medicine is emerging as a key trend, with patient-derived cell cultures increasing by 27% annually. Approximately 190,000 patient-specific samples were processed in 2025, with projections exceeding 450,000 samples by 2030. Adoption in oncology research has reached 54%, enabling better prediction of drug response. The use of 3D spheroids and organoids has improved clinical trial success rates by 18–22%, significantly reducing costs. These advancements are driving innovation pipelines and expanding India 3D Cell Culture Market Trends.

Automation and AI Integration in Cell Culture Systems

Automation in 3D cell culture has expanded significantly, with robotic systems installed in 38% of advanced labs and AI-driven analytics improving experimental accuracy by 25%. Automated platforms process up to 5,000 samples per week, compared to 1,200 manually. AI integration has reduced data analysis time by 40% and increased reproducibility by 30%. This shift toward digitalized workflows is accelerating research productivity and shaping India 3D Cell Culture Market Trends.

India 3D Cell Culture Market Driver

Increasing Demand for Physiologically Relevant Cell Models in Drug Development

The growing need for accurate preclinical models is a major driver, with 3D cell culture systems reducing drug failure rates by 25–35% compared to traditional 2D methods. In India, pharmaceutical R&D expenditure has exceeded USD 2.1 billion annually, with approximately 18% allocated to advanced cell culture technologies. Over 420 drug development projects are currently utilizing 3D models, and adoption rates have surged by 22% over the past three years. These systems improve cell differentiation by 30% and enhance predictive accuracy for toxicity testing by 28%. Additionally, increasing collaboration between research institutes and pharma companies has led to a 15% rise in joint projects. These factors collectively accelerate India 3D Cell Culture Market Growth.

India 3D Cell Culture Market Restraint

High Cost of Advanced 3D Cell Culture Systems

Despite strong adoption, high costs remain a significant restraint, with advanced systems priced between USD 2,000–15,000 per unit. Consumables such as scaffolds and media contribute to 45–55% of operational costs, while maintenance expenses account for an additional 20%. Small research labs, representing 35% of the market, face budget constraints limiting adoption. Furthermore, lack of skilled professionals—estimated shortage of 18,000 trained specialists—hampers efficient utilization. Import dependency for high-end equipment (around 65%) also increases costs due to tariffs and logistics. These challenges create barriers for widespread adoption, impacting India 3D Cell Culture Market Growth.

India 3D Cell Culture Market Opportunity

Expansion of Biotechnology and Academic Research Infrastructure

India’s biotechnology sector is expanding rapidly, with over 75 new research facilities established between 2022 and 2025. Government initiatives such as BioE3 policy have allocated over USD 500 million for life sciences research, boosting infrastructure development. Academic institutions account for 32% of 3D cell culture demand, with increasing funding enabling procurement of advanced systems. Additionally, contract research organizations (CROs) are growing at 17% annually, contributing significantly to market expansion. The integration of 3D models in regenerative medicine and tissue engineering presents opportunities for future innovation, driving India 3D Cell Culture Market Growth.

Challenge in India 3D Cell Culture Market

Standardization and Reproducibility Issues in 3D Models

Standardization remains a critical challenge, with variability in scaffold composition and cell behavior leading to inconsistent results in 20–25% of experiments. Lack of universal protocols affects data comparability across laboratories, while differences in cell culture conditions (temperature 36–38°C, oxygen levels 5–20%) create inconsistencies. Additionally, regulatory frameworks for 3D models are still evolving, delaying approvals for clinical applications. Training requirements and complex workflows further limit scalability, with only 40% of labs achieving optimal reproducibility. Addressing these challenges is essential for sustained India 3D Cell Culture Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 158.9 million |

| Market Size in 2026 | USD 185.6 million |

| Market Size in 2034 | USD 642.3 million |

| CAGR | 16.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 3D Cell Culture Market Segmentation

By Type

Scaffold-based systems dominate with approximately 52% share, producing over 620,000 units annually. These systems utilize biomaterials such as collagen and hydrogels with pore sizes ranging from 100–400 microns. They provide structural support for cell attachment and enhance cell proliferation by 30%. Widely used in cancer research and tissue engineering, these systems offer high reproducibility and compatibility with imaging technologies.

Scaffold-free systems account for around 28% share, with production exceeding 340,000 units. Techniques such as spheroid formation and hanging drop methods allow cells to self-assemble, improving physiological relevance. These systems enhance cell-cell interaction by 40% and reduce external material interference. Adoption is increasing in drug screening applications due to cost efficiency and scalability.

Microfluidic-based systems hold approximately 20% share and are the fastest-growing segment. Annual production of chips has surpassed 300,000 units, with flow rates optimized between 0.5–5 µL/min. These systems enable precise control of microenvironments, improving experimental accuracy by 35%. They are extensively used in organ-on-chip applications and personalized medicine research.

By Application

Cancer research represents the largest segment with 48% share, utilizing over 580,000 units annually. 3D cell cultures improve tumor modeling accuracy by 30–40%, enabling better drug response prediction. Spheroids and organoids are widely used, with adoption rates exceeding 60% in oncology labs.

Drug discovery accounts for 37% share, with over 450,000 units used annually. 3D models reduce screening time by 25% and increase hit identification rates by 20%. Integration with high-throughput screening platforms enables testing of over 10,000 compounds per week.

Stem cell research contributes 15% share, with approximately 180,000 units utilized annually. These systems support differentiation efficiency of 35–45% and are critical for regenerative medicine applications. Growing interest in tissue engineering is boosting segment expansion.

India 3D Cell Culture Market Segmentations

Type

- Scaffold-based

- Scaffold-free

- Microfluidic-based

Application

- Cancer Research

- Drug Discovery

- Stem Cell Research

India Insights

India dominates the regional outlook with 100% share due to defined scope, supported by over 3,200 biotech facilities and annual production exceeding 1.1 million units. The pharmaceutical sector contributes 55% of demand, followed by academic research at 30% and CROs at 15%. Government funding exceeding USD 120 million annually and private investments of USD 80–100 million drive innovation.

Urban hubs such as Bengaluru, Hyderabad, and Pune account for nearly 65% of market activity, with over 1,800 labs concentrated in these regions. Adoption rates of advanced technologies exceed 45% in Tier-1 cities, while Tier-2 cities show growth rates of 18–20% annually. The strong presence of CROs and increasing clinical trials (over 1,500 active trials) further boost demand, strengthening overall market ecosystem.

Top Players in India 3D Cell Culture Market

- Thermo Fisher Scientific

- Corning Incorporated

- Merck KGaA

- Lonza Group

- Sartorius AG

- Danaher Corporation

- 3D Biotek LLC

- Tecan Group Ltd

- PromoCell GmbH

- ReproCELL Inc

- Emulate Inc

- InSphero AG

Top Two Companies

-

Thermo Fisher Scientific

-

Holds approximately 18–20% market share in India

-

Strong presence with over 150 product SKUs and annual sales exceeding USD 35 million in India

Thermo Fisher leads through extensive product portfolios including scaffolds, media, and automated systems. Its distribution network covers over 40 cities, and R&D investment exceeds USD 1 billion globally.

-

-

Corning Incorporated

-

Accounts for 14–16% market share

-

Supplies over 300,000 units annually in India

Corning focuses on innovative cultureware and microplates, improving cell viability by 25%. Its partnerships with research institutes strengthen market positioning.

-

Investment

Investment in the India 3D cell culture market has grown significantly, with total funding exceeding USD 300 million between 2022 and 2025. Approximately 45% of investments are allocated to pharmaceutical R&D, 30% to academic research, and 25% to CRO expansion. Regional investment is concentrated in Bengaluru (32%), Hyderabad (28%), and Pune (18%). Venture capital participation has increased by 22% annually.

M&A activities are also rising, with over 15 collaborations recorded between 2023 and 2025. Strategic partnerships between biotech startups and multinational corporations have improved technology transfer and product development. Joint ventures account for 35% of new project funding, while licensing agreements contribute 20%. These collaborations enhance scalability and market penetration.

New Product

New product development is accelerating, with over 120 new 3D culture products launched between 2023 and 2026. Approximately 38% of these products incorporate microfluidic technology, while 42% focus on improved scaffold materials. Performance improvements include 30% higher cell viability and 25% faster assay results.

Innovation in organ-on-chip platforms and AI integration is driving product differentiation. Companies are investing heavily in automation, with 35% of new systems featuring robotic capabilities. These advancements enhance efficiency and expand application scope.

Recent Development in India 3D Cell Culture Market

- 2026: A leading biotech firm increased production capacity by 28%, reaching 150,000 units annually, improving supply chain efficiency and reducing lead time by 20%.

- 2025: Introduction of AI-integrated culture systems improved experimental accuracy by 32% and reduced processing time by 25%.

- 2024: Expansion of microfluidic chip production by 35%, enabling testing of over 500,000 samples annually.

Research Methodology for India 3D Cell Culture Market

The research process involves a combination of primary and secondary data collection to ensure accuracy and reliability. Primary research includes interviews with over 50 industry experts, including executives, researchers, and suppliers, providing insights into market trends and adoption rates. Secondary research involves analysis of company reports, government publications, and industry databases to validate data.

Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, pricing analysis, and demand forecasting. Historical data from 2022–2024 is analyzed to identify growth patterns, while predictive models estimate future trends up to 2034. Data triangulation ensures consistency across multiple sources, enhancing the credibility of findings.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.