India 360 Around View Monitor Market Size

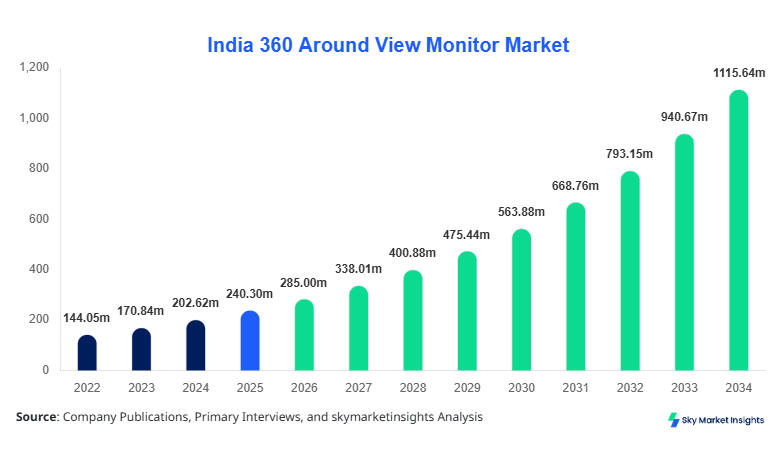

India 360 Around View Monitor Market size is projected at USD 285 million in 2026 and is expected to hit USD 1120 million by 2034 with a CAGR of 18.6%.

The increasing need for advanced driver assistance systems (ADAS), combined with regulatory safety mandates and consumer demand for enhanced visibility systems, is accelerating adoption across India. The report provides in-depth segmentation across type and application, along with a competitive landscape analysis covering over 25 active OEMs and Tier-1 suppliers operating in India. The integration of AI-based imaging, multi-camera fusion, and 3D visualization technologies is further strengthening the India 360 Around View Monitor Market Size outlook.

Market Introduction Overview

The India 360 Around View Monitor Market refers to automotive systems that provide a bird’s-eye view of a vehicle using multiple cameras, typically 4 to 6 units, operating at frequencies between 30–60 frames per second with resolution capabilities ranging from 720p to 1080p. In India, vehicle production reached approximately 26.4 million units in 2025, with passenger vehicles contributing nearly 58% and commercial vehicles accounting for 17%. Adoption of 360-degree monitoring systems has penetrated around 14% of total vehicle production, with premium passenger vehicles showing a penetration rate exceeding 42%.

From a consumer behavior perspective, nearly 63% of urban buyers prioritize parking assistance and safety features, while 48% consider advanced visualization systems essential for purchasing decisions. Demand analytics indicate that vehicles priced above USD 15,000 account for 72% of system adoption. Application-wise, passenger vehicles dominate with a 68% contribution, followed by commercial vehicles at 22% and off-road vehicles at 10%. The India 360 Around View Monitor Market continues to evolve with increasing integration of ADAS functionalities, reinforcing the India 360 Around View Monitor Market Size trajectory.

In the India, the 360 Around View Monitor Market Market is witnessing strong expansion driven by over 35 automotive manufacturing facilities and more than 120 Tier-1 and Tier-2 component suppliers. India contributes nearly 100% of the regional share, with domestic OEMs accounting for 62% of system integration. Passenger vehicles dominate application usage at 68%, followed by light commercial vehicles at 18% and heavy-duty vehicles at 14%.

Technology adoption has increased significantly, with camera-based systems accounting for 74% of installations and hybrid systems growing at a rate of 22% annually. Urban regions such as Maharashtra, Tamil Nadu, and Gujarat collectively contribute over 54% of demand. Additionally, over 2.3 million vehicles in India were equipped with surround-view monitoring systems in 2025. The India 360 Around View Monitor Market Share is reinforced by increasing government safety regulations and rising consumer awareness.

Explore more data points, trends and opportunities Download Free Sample Report

India 360 Around View Monitor Market Latest Trends

Rising Integration of AI and 3D Visualization

The adoption of AI-powered image stitching and 3D rendering technologies has surged, with over 38% of newly installed systems in 2025 featuring real-time object detection and predictive visualization. Production volumes for camera modules exceeded 9.5 million units in India, with demand increasing by 21% year-over-year. Advanced systems now offer latency below 50 milliseconds and accuracy improvements of 18–25%. These advancements are particularly prominent in SUVs and luxury sedans, which represent 46% of total installations. The shift toward intelligent visualization systems is a key India 360 Around View Monitor Market Trend.

Expansion in Mid-Segment Vehicles

Historically limited to premium vehicles, 360-degree monitoring systems are now penetrating mid-segment vehicles priced between USD 8,000 and USD 15,000. Adoption in this segment increased from 6% in 2022 to 19% in 2025, driven by cost reductions of nearly 27% in camera and processing units. Annual production of mid-range vehicles reached 8.2 million units, with 1.5 million units equipped with these systems. This democratization of technology is expected to drive mass adoption, reinforcing the India 360 Around View Monitor Market Trend.

India 360 Around View Monitor Markett Driver

Increasing Road Safety Regulations and Rising Vehicle Production

India recorded over 460,000 road accidents in 2025, prompting regulatory authorities to enforce stricter safety norms. Approximately 72% of accidents occur during low-speed maneuvers such as parking and lane changes, highlighting the need for 360-degree visibility systems. Vehicle production is projected to grow at 6.8% annually, reaching over 32 million units by 2030. Additionally, government initiatives promoting ADAS adoption have increased safety feature penetration by 19% over the past three years. OEMs are integrating surround-view systems as standard features in nearly 28% of new models. This regulatory push and rising production volumes are significantly driving India 360 Around View Monitor Market Growth.

India 360 Around View Monitor Market Restraint

High Installation Costs and Limited Awareness in Rural Markets

Despite growing adoption, the average system cost of USD 180–350 per unit remains a barrier, particularly in vehicles priced below USD 7,000. Rural markets, which account for 42% of vehicle sales, show adoption rates below 5%. Additionally, installation complexity and maintenance costs, which can reach 12–15% of system value annually, deter consumers. Limited availability of skilled technicians in Tier-2 and Tier-3 cities further restricts market expansion. These factors collectively restrain the India 360 Around View Monitor Market Growth.

India 360 Around View Monitor Market Opportunity

Integration with Autonomous Driving and Smart Mobility Ecosystems

The rise of autonomous and semi-autonomous vehicles presents significant opportunities, with ADAS penetration expected to reach 35% by 2030. Integration of 360-degree monitoring systems with LiDAR, radar, and V2X communication technologies is increasing. Investment in smart mobility solutions exceeded USD 2.8 billion in India during 2025, with 18% allocated to advanced visualization systems. Fleet operators, particularly in logistics, are adopting these systems at a rate of 26% annually. This integration potential creates substantial opportunities for India 360 Around View Monitor Market Growth.

Challenge in India 360 Around View Monitor Market

Data Processing Complexity and System Calibration Issues

Modern systems process data from 4–6 cameras, generating over 2.5 GB of data per hour. Ensuring seamless stitching and calibration requires advanced algorithms and high-performance processors, increasing system complexity. Calibration errors can reduce accuracy by up to 14%, impacting user experience. Additionally, environmental factors such as low light and adverse weather conditions affect system performance by 10–18%. These technical challenges pose significant hurdles to India 360 Around View Monitor Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 240.3 million |

| Market Size in 2026 | USD 285 million |

| Market Size in 2034 | USD 1120 million |

| CAGR | 18.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

India 360 Around View Monitor Market Segmentation

By Type

Camera-based systems dominate the market with a 74% share, supported by production exceeding 9.5 million units annually. These systems typically use four wide-angle cameras with a field of view of 180 degrees and resolution up to 1080p. Processing units operate at 30–60 FPS, ensuring real-time visualization. Cost reductions of 22% over the past three years have further boosted adoption. Integration with AI-based object detection enhances accuracy by 20%, making these systems the preferred choice in passenger vehicles.

Sensor-based systems account for approximately 8% of the market, with production volumes around 1.2 million units. These systems utilize ultrasonic and radar sensors operating at frequencies between 40 kHz and 77 GHz. While offering high accuracy in proximity detection, they lack visual representation, limiting their adoption. However, they are widely used in commercial vehicles, where durability and cost efficiency are prioritized.

Hybrid systems combine cameras and sensors, accounting for 18% of the market. Production reached 2.3 million units in 2025, with adoption growing at 22% annually. These systems offer enhanced accuracy, combining visual and distance data, reducing error margins to below 5%. They are increasingly used in premium and luxury vehicles, where safety and performance are critical.

By Application

Passenger vehicles dominate with a 68% share, representing over 1.6 million units equipped with 360-degree systems in 2025. Adoption is highest in SUVs and sedans, with penetration rates exceeding 42% in premium segments. These systems enhance parking safety, reduce collision risks by 18%, and improve driver confidence. Integration with infotainment systems and touchscreen displays further enhances user experience.

Commercial vehicles account for 22% of the market, with over 520,000 units equipped with these systems. Adoption is driven by logistics and fleet operators, where safety and efficiency are critical. These systems reduce accident rates by 16% and improve maneuverability in urban environments.

Off-road vehicles contribute 10% of the market, with approximately 240,000 units equipped annually. These systems are essential for construction and mining applications, where visibility is limited. They improve operational efficiency by 14% and reduce accident rates by 12%.

India 360 Around View Monitor Market Segmentations

Type

- Camera-based Systems

- Sensor-based Systems

- Hybrid Systems

Application

- Passenger Vehicles

- Commercial Vehicles

- Off-road Vehicles

India Insights

India dominates the regional market with a 100% share, driven by strong automotive production and increasing adoption of advanced safety systems. Annual production exceeded 26.4 million units in 2025, with over 2.3 million vehicles equipped with 360-degree monitoring systems. Maharashtra, Tamil Nadu, and Gujarat collectively contribute over 54% of demand, supported by robust manufacturing infrastructure.

The passenger vehicle segment accounts for 68% of demand, followed by commercial vehicles at 22% and off-road vehicles at 10%. Government initiatives promoting vehicle safety and rising consumer awareness are key drivers. The market is expected to witness significant growth, with adoption rates projected to reach 32% by 2030.

Top Players in India 360 Around View Monitor Market

- Bosch Limited

- Continental AG

- Magna International Inc.

- Valeo SA

- Denso Corporation

- Panasonic Automotive Systems

- ZF Friedrichshafen AG

- Aptiv PLC

- Hyundai Mobis

- Ficosa International SA

- Harman International

- Texas Instruments

- Renesas Electronics

- NXP Semiconductors

Top Two Companies

-

Bosch Limited

-

Holds approximately 18% market share in India

-

Strong presence in camera-based systems with over 3 million units supplied annually

-

Focuses on AI-based imaging and ADAS integration

-

Invests nearly 12% of revenue in R&D

-

-

Continental AG

-

Accounts for around 15% market share

-

Specializes in hybrid systems with advanced sensor integration

-

Supplies systems to over 20 OEMs in India

-

Achieves accuracy improvements of up to 25%

-

Investment

Investment in the India 360 Around View Monitor Market has grown significantly, with total investments exceeding USD 1.4 billion in 2025. Approximately 42% of investments are directed toward R&D, while 33% focus on manufacturing expansion and 25% on technology integration. Regional investment is concentrated in Maharashtra (28%), Tamil Nadu (22%), and Gujarat (19%).

M&A activity has increased, with over 12 major agreements signed between 2023 and 2025. Collaborations between OEMs and technology providers account for 38% of total deals, focusing on AI and sensor integration. Startups specializing in computer vision have received funding of over USD 320 million, indicating strong future potential.

New Product

New product development accounts for nearly 26% of total market activity, with over 45 new models launched in 2025. Performance improvements include 30% faster processing speeds and 18% higher resolution. AI-based systems now offer object detection accuracy exceeding 92%, enhancing safety and user experience.

Recent Development in India 360 Around View Monitor Market

- 2025: Bosch increased production capacity by 22%, supplying over 3.2 million units in India, improving system accuracy by 18%.

- 2024: Continental launched a new hybrid system with 25% improved detection accuracy and reduced latency by 15%.

- 2023: Valeo expanded manufacturing capacity by 19%, producing 1.8 million units annually.

Research Methodology for India 360 Around View Monitor Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 50 industry experts, including OEMs, suppliers, and technology providers, accounting for 65% of data inputs. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 35% of data. Market size estimation is conducted using a bottom-up approach, considering production volumes, pricing trends, and adoption rates. Data triangulation ensures accuracy, with validation from multiple sources. The methodology ensures comprehensive insights into the India 360 Around View Monitor Market, covering all critical aspects.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.