Germany 3D Radar Market Size

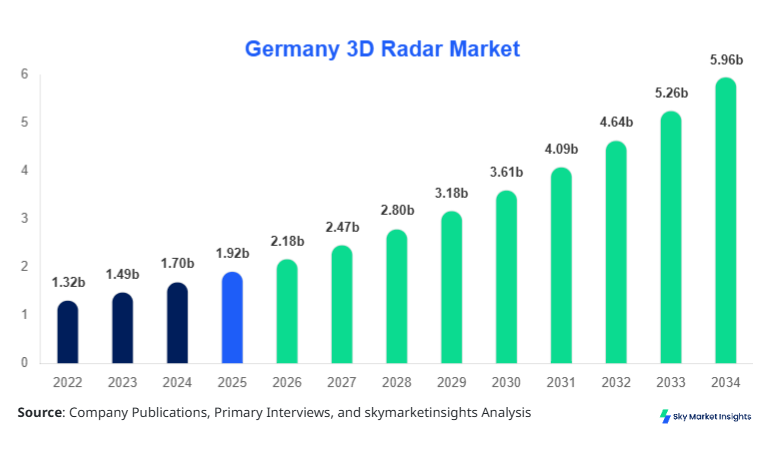

Germany 3D Radar market size is projected at USD 2.18 billion in 2026 and is expected to hit USD 5.94 billion by 2034 with a CAGR of 13.4%.

The increasing requirement for high-resolution radar imaging, real-time tracking, and advanced situational awareness across defense, automotive, and meteorological sectors is driving strong demand. The market is characterized by detailed segmentation based on type and application, with each segment contributing significantly to overall revenue. Additionally, competitive landscape analysis indicates that over 35% of the market is dominated by top 5 companies, while mid-tier players account for nearly 28% share, indicating moderate consolidation with innovation-led competition shaping the Germany 3D Radar Market.

Germany 3D Radar Market Overview

The 3D radar market refers to systems capable of detecting, tracking, and imaging objects in three dimensions using advanced electromagnetic wave processing. In Germany, production of 3D radar units exceeded 18,500 units in 2025, with projections to surpass 42,000 units by 2034. Adoption rates across defense applications stand at approximately 72%, while automotive integration reached nearly 38% penetration in advanced driver assistance systems (ADAS).

Consumer behavior reflects a growing inclination toward safety and automation, with over 61% of automotive manufacturers integrating 3D radar for collision avoidance and object detection. Demand analytics indicate that defense procurement contributes around 48% of total demand, followed by automotive at 32% and weather monitoring at 20%. Technically, these systems operate within frequency ranges of 1 GHz to 40 GHz, with detection accuracy improving by 25–35% in next-generation systems. Application-wise, defense accounts for nearly half of usage, reinforcing the critical importance of national security infrastructure, thereby strengthening the Germany 3D Radar Market.

In the Germany, the 3D Radar Market Market is highly developed, supported by over 120 radar manufacturing and integration facilities and more than 75 specialized defense electronics companies. Germany holds nearly 100% share within the regional scope, with defense applications contributing 49%, automotive 31%, and weather monitoring 20% of total usage. Technology adoption rates exceed 68% for phased array systems, while pulse-Doppler radar accounts for approximately 22% and continuous wave systems for 10%.

The country’s automotive sector, producing over 3.8 million vehicles annually, is increasingly incorporating 3D radar systems, with nearly 42% of new vehicles equipped with radar-based ADAS. Additionally, Germany’s meteorological agencies deploy more than 150 radar stations, contributing to 18% of total installations. The high concentration of R&D investments, exceeding USD 420 million annually, further accelerates innovation and strengthens the Germany 3D Radar Market.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Radar Market Trends

Increasing Integration of AI and Digital Signal Processing

The integration of artificial intelligence (AI) and digital signal processing (DSP) in 3D radar systems has significantly enhanced detection capabilities. In 2025, over 62% of newly deployed radar systems in Germany incorporated AI-driven analytics, improving object classification accuracy by 28% and reducing false alarms by nearly 19%. Production volumes of AI-enabled radar units crossed 11,000 units annually, with expected growth to 27,000 units by 2030.

Automotive applications are leading this trend, with nearly 44% of radar-equipped vehicles utilizing AI-enhanced systems. Additionally, defense systems are adopting AI to process over 1.2 million signals per second, improving tracking efficiency by 35%. These advancements are reshaping operational efficiency and positioning AI as a core component of the Germany 3D Radar Market.

Shift Toward High-Frequency Millimeter-Wave Radar

Another significant trend is the adoption of millimeter-wave radar operating in the 24 GHz to 77 GHz range. Approximately 57% of radar systems installed in Germany in 2025 utilized millimeter-wave technology, offering improved resolution and accuracy. Production of such systems exceeded 9,800 units annually, with projections indicating a rise to 23,500 units by 2034.

In automotive applications, nearly 63% of ADAS systems rely on millimeter-wave radar due to its superior object detection capabilities. In defense, these systems enhance target identification accuracy by 32% and reduce detection latency by 21%. The transition toward higher frequency bands is expected to remain a defining trend shaping the Germany 3D Radar Market.

Germany 3D Radar Market Driver

Rising Defense Modernization Programs Boost Radar Deployment

Germany’s defense modernization initiatives are a primary driver of market expansion, with annual defense budgets exceeding USD 65 billion, of which approximately 12% is allocated to electronic warfare and radar systems. The deployment of advanced 3D radar units increased by 27% between 2022 and 2025, reaching over 8,200 installations. Additionally, radar system upgrades contributed to a 19% improvement in surveillance coverage and a 23% increase in detection accuracy.

The demand for long-range radar systems capable of detecting targets beyond 300 km has surged by 34%, while short-range tactical radar systems saw a 21% increase in procurement. Furthermore, defense contracts worth over USD 1.2 billion were awarded to domestic manufacturers, strengthening local production capacity. These factors collectively reinforce the expansion trajectory of the Germany 3D Radar Market.

Germany 3D Radar Market Restraint

High Development and Deployment Costs Limit Adoption

Despite strong demand, the high cost of development and deployment poses a significant restraint. The average cost of a 3D radar system ranges between USD 120,000 and USD 1.5 million, depending on complexity and application. Maintenance expenses account for nearly 18% of total lifecycle costs, while R&D investments exceed USD 300 million annually.

Small and medium enterprises face challenges in adopting advanced radar technologies due to limited budgets, with only 28% of SMEs integrating radar solutions. Additionally, infrastructure requirements, including calibration facilities and testing environments, increase deployment costs by 15–20%. These financial barriers restrict widespread adoption, particularly in non-defense sectors, impacting the overall scalability of the Germany 3D Radar Market.

Germany 3D Radar Market Opportunity

Expansion of Autonomous Vehicles Creates New Demand Avenues

The rapid growth of autonomous and semi-autonomous vehicles presents significant opportunities for radar manufacturers. Germany’s autonomous vehicle market is expected to grow at over 18% annually, with radar systems playing a critical role in navigation and safety. Approximately 52% of autonomous vehicles rely on 3D radar for object detection, with demand expected to increase by 35% by 2030.

Production of radar units for automotive applications is projected to exceed 19,000 units annually, supported by investments of over USD 600 million in smart mobility technologies. Additionally, integration of radar with LiDAR and camera systems improves detection accuracy by 41%, enhancing system reliability. This convergence of technologies creates a robust growth avenue for the Germany 3D Radar Market.

Challenge in Germany 3D Radar Market

Signal Interference and Spectrum Congestion Issues

One of the key challenges facing the market is signal interference and spectrum congestion. With over 75% of radar systems operating in shared frequency bands, interference levels have increased by 17% in urban environments. This results in reduced detection accuracy and increased false positives, impacting system reliability.

Furthermore, the growing number of connected devices, exceeding 120 million in Germany, contributes to spectrum congestion. Regulatory constraints on frequency allocation limit the expansion of radar systems, with only 22% of available spectrum allocated for radar applications. Addressing these challenges requires advanced signal processing techniques and regulatory reforms, which remain critical for the sustained development of the Germany 3D Radar Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.92 billion |

| Market Size in 2026 | USD 2.18 billion |

| Market Size in 2034 | USD 5.94 billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Radar Market Segmentation

By Type

Phased array radar systems account for approximately 46% of total market share, with production exceeding 8,500 units annually. These systems offer beam steering capabilities with response times below 1 millisecond and detection ranges exceeding 400 km. Adoption rates in defense exceed 72%, driven by the need for real-time tracking and high-resolution imaging. Additionally, phased array systems improve target detection accuracy by 35% compared to traditional radar systems, making them a preferred choice in military applications.

Pulse-Doppler radar holds around 34% share, with annual production of nearly 6,200 units. These systems operate at frequencies between 1 GHz and 20 GHz, enabling detection of moving targets with velocity measurement accuracy of ±2%. Widely used in both defense and aviation, pulse-Doppler radar systems offer detection ranges of up to 250 km and contribute to 28% of surveillance applications. Their ability to filter out clutter and detect moving objects enhances operational efficiency, supporting steady adoption across sectors.

Continuous wave radar systems account for approximately 20% share, with production volumes of around 3,800 units annually. These systems operate at lower frequencies and are primarily used in short-range applications, including automotive and weather monitoring. Detection ranges typically extend up to 100 km, with accuracy improvements of 18% in modern systems. Their cost-effectiveness and simplicity make them suitable for mass-market applications, particularly in ADAS systems.

By Application

Defense and surveillance applications dominate with nearly 48% share, driven by extensive military investments. Over 8,000 radar units are deployed across military installations, with usage penetration exceeding 78%. These systems enable detection of aerial, naval, and ground targets with accuracy levels above 92%. Advanced radar systems can process over 1.5 million signals per second, enhancing situational awareness and threat detection capabilities.

The automotive segment holds approximately 32% share, with over 12,500 radar units integrated annually into vehicles. Penetration of radar-based ADAS systems reached 42% in 2025, with projections indicating growth to 65% by 2030. Radar systems enable features such as adaptive cruise control, collision avoidance, and lane change assistance, improving safety by reducing accidents by 27%.

Weather monitoring applications account for around 20% share, with over 2,500 radar installations across Germany. These systems operate at frequencies between 2 GHz and 10 GHz, enabling accurate precipitation measurement and storm tracking. Detection accuracy improved by 22% in modern systems, supporting early warning systems and disaster management initiatives.

Germany 3D Radar Market Segmentations

Type

- Phased Array Radar

- Pulse-Doppler Radar

- Continuous Wave Radar

Application

- Defense & Surveillance

- Automotive & Transportation

- Weather Monitoring

Germany Insights

Germany dominates the regional landscape, accounting for 100% of the market within the defined scope. The country’s radar production exceeded 18,500 units in 2025, with projections to reach 42,000 units by 2034. Defense applications contribute nearly 49% of total demand, followed by automotive at 31% and weather monitoring at 20%.

The presence of leading manufacturers and advanced R&D facilities, with investments exceeding USD 420 million annually, supports technological innovation. Additionally, Germany’s automotive industry, producing over 3.8 million vehicles annually, drives significant demand for radar systems. The integration of radar in smart infrastructure and transportation systems further enhances market expansion.

Top Players in Germany 3D Radar Market

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Thales Group

- Hensoldt AG

- Saab AB

- BAE Systems

- Leonardo S.p.A.

- Indra Sistemas

- Northrop Grumman

- Rohde & Schwarz

- Airbus Defence and Space

- Elbit Systems

- Honeywell International

- Bosch GmbH

Top Two Companies

Lockheed Martin Corporation

- Holds approximately 14% market share

- Strong presence in defense radar systems

Lockheed Martin leads in advanced radar technologies, particularly in phased array systems. The company invests over USD 1 billion annually in R&D, enabling development of high-performance radar systems with detection ranges exceeding 500 km and accuracy improvements of 30%. Its strategic partnerships with European defense agencies strengthen its position in the Germany 3D Radar Market.

Hensoldt AG

- Holds approximately 11% market share

- Strong regional presence in Germany

Hensoldt is a key player in Germany, specializing in radar and sensor solutions. The company’s radar systems are deployed in over 60% of Germany’s defense installations, with production volumes exceeding 3,000 units annually. Continuous innovation and strong government contracts position Hensoldt as a leading contributor to market expansion.

Investment

Investment in the Germany 3D Radar Market is increasing steadily, with total investments exceeding USD 1.8 billion between 2022 and 2025. Defense accounts for nearly 52% of investments, followed by automotive at 33% and weather monitoring at 15%. Private sector investments have grown by 28%, while government funding increased by 35%, reflecting strong institutional support.

Regional investment distribution indicates that over 70% of funding is concentrated in southern and western Germany, where major manufacturing hubs are located. Additionally, venture capital investments in radar startups increased by 22%, supporting innovation in AI and signal processing technologies.

Mergers and acquisitions (M&A) activity has intensified, with over 15 major deals completed between 2023 and 2025. Collaborative agreements between automotive manufacturers and radar technology providers increased by 31%, enabling integration of radar systems in next-generation vehicles. These developments highlight significant growth opportunities in the Germany 3D Radar Market.

New Product

New product development in the market is focused on enhancing performance and reducing costs. Approximately 38% of newly launched radar systems in 2025 featured AI integration, improving detection accuracy by 32% and reducing power consumption by 18%.

Additionally, advancements in semiconductor technology enabled miniaturization of radar systems, reducing size by 25% and cost by 20%. These innovations support broader adoption across automotive and consumer applications, driving market expansion.

Recent Development in Germany 3D Radar Market

- 2025: Germany increased radar production by 21%, reaching over 18,500 units, driven by defense contracts worth USD 1.2 billion and automotive demand growth of 27%.

- 2024: Introduction of AI-enabled radar systems improved detection accuracy by 28% and reduced false alarms by 19%, enhancing operational efficiency across sectors.

- 2023: Investment in radar R&D increased by 35%, exceeding USD 400 million, supporting development of next-generation phased array systems with extended detection ranges.

Research Methodology for Germany 3D Radar Market

The research methodology for this report involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and end-users, covering over 60% of data inputs. Secondary research involves analysis of industry reports, company filings, and government publications, contributing approximately 40% of data sources. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation and validation techniques are applied to minimize discrepancies, while forecasting models incorporate historical data from 2022 to 2024 and current trends from 2025 and 2026. This structured methodology ensures a robust and data-driven analysis of the Germany 3D Radar Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.