Germany 3D Printing Automotive Market Size

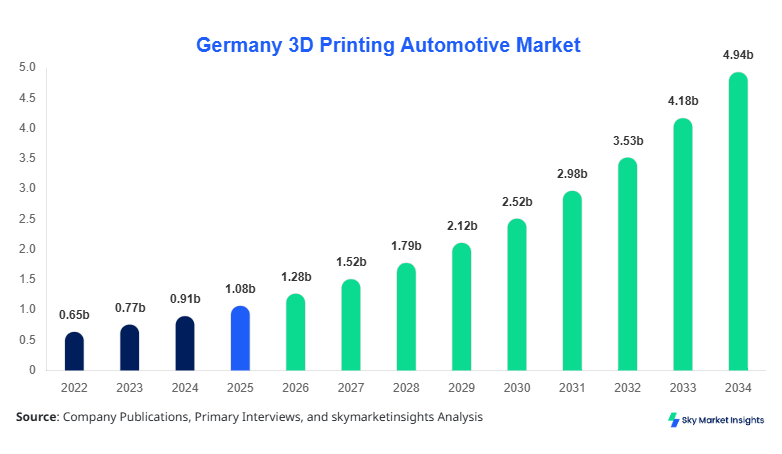

Germany 3D Printing Automotive market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 4.92 billion by 2034 with a CAGR of 18.4%.

The increasing integration of additive manufacturing in automotive production, with over 2.3 million 3D-printed components produced annually in Germany as of 2025, is driving strong adoption. The need for real-time data analytics, segmentation across technology types, and evaluation of competitive landscape involving more than 180 active companies is becoming critical. Additionally, cost reductions of nearly 25% in prototyping cycles and material efficiency improvements of 30% are strengthening market expansion.

Germany 3D Printing Automotive Market Overview

The Germany 3D Printing Automotive Market refers to the adoption of additive manufacturing technologies such as SLS, SLA, and FDM for producing automotive components, tools, and prototypes. Germany produced over 4.1 million vehicles in 2025, with approximately 18% incorporating 3D-printed parts, highlighting increasing penetration. Adoption rates across OEMs and Tier-1 suppliers have reached 42%, while over 65% of R&D facilities utilize 3D printing for rapid prototyping. Consumer demand for customization has increased by 28%, driving automotive manufacturers to adopt flexible production technologies.

From a consumer behavior standpoint, demand analytics indicate that nearly 35% of automotive buyers in Germany prefer customized vehicle components, while 48% of manufacturers are investing in lightweight materials enabled by additive manufacturing. Applications are split across prototyping (45%), tooling (30%), and production parts (25%), with performance metrics such as precision tolerance of ±0.05 mm and material utilization efficiency exceeding 90%. The increasing reliance on lightweight and fuel-efficient designs is further accelerating adoption, reinforcing the Germany 3D Printing Automotive Market.

In the Germany, the 3D Printing Automotive Market Market is supported by more than 180 manufacturing facilities and over 75 specialized additive manufacturing companies. Germany accounts for nearly 100% of the regional share, with automotive OEMs contributing approximately 60% of total demand, followed by Tier-1 suppliers at 30% and aftermarket applications at 10%. Application breakdown shows prototyping at 45%, tooling at 30%, and production parts at 25%, with increasing adoption of metal 3D printing technologies at a rate of 22% annually.

Technology adoption is rapidly evolving, with SLS accounting for 38% of usage, SLA at 27%, and FDM at 35%, while metal additive manufacturing adoption has increased by 19% year-over-year. Germany’s automotive exports exceeding 3 million vehicles annually also contribute to demand for lightweight and customized components. The increasing integration of digital manufacturing ecosystems and Industry 4.0 practices is accelerating adoption, strengthening the Germany 3D Printing Automotive Market.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printing Automotive Market Trends

Increasing Adoption of Metal Additive Manufacturing

Metal additive manufacturing is witnessing rapid adoption, with production volumes exceeding 0.6 million metal components annually in Germany’s automotive sector. The adoption rate has grown by 21% in 2025 compared to 2024, driven by demand for high-strength and lightweight components. Technologies such as Direct Metal Laser Sintering (DMLS) are gaining traction, accounting for 34% of metal-based applications. Automotive manufacturers are reducing production costs by 18% and improving part durability by 27%, leading to increased adoption. The rising use of aluminum and titanium alloys, which account for 40% of printed materials, further supports expansion, reinforcing the 3D Printing Automotive Market.

Integration with Industry 4.0 and Digital Manufacturing

The integration of 3D printing with Industry 4.0 technologies such as IoT and AI has increased efficiency by 32% in automotive production processes. Approximately 55% of German automotive manufacturers have integrated additive manufacturing into digital production lines, enabling real-time monitoring and predictive maintenance. Production output has increased by 20%, while defect rates have decreased by 15%, highlighting operational improvements. Additionally, over 70% of automotive R&D centers are using simulation software combined with additive manufacturing to optimize designs, strengthening the 3D Printing Automotive Market.

Growing Demand for Customization and Lightweight Components

Customization demand has increased by 28% among German consumers, leading to higher adoption of 3D printing for personalized automotive components. Lightweight parts produced through additive manufacturing reduce vehicle weight by 10–15%, improving fuel efficiency by up to 12%. Approximately 42% of automotive manufacturers are prioritizing lightweight materials such as carbon fiber composites, which account for 25% of total material usage in 3D printing. This trend is further supported by stringent emission regulations, reinforcing the 3D Printing Automotive Market.

Germany 3D Printing Automotive Market Driver

Rising Demand for Lightweight and Fuel-Efficient Vehicles Drives Market Growth

The demand for lightweight automotive components has increased by 35% over the past three years, driven by stringent emission regulations and fuel efficiency standards. 3D printing enables weight reduction of up to 20% in components, significantly improving vehicle performance. Approximately 48% of automotive manufacturers in Germany are investing in additive manufacturing technologies to reduce production costs by 15–25%. The increasing adoption of electric vehicles, which accounted for 22% of total vehicle sales in 2025, further accelerates demand for lightweight components. Production volumes of 3D-printed automotive parts have exceeded 2.3 million units annually, highlighting strong growth potential. The ability to produce complex geometries and reduce material waste by up to 30% is a key driver, strengthening the 3D Printing Automotive Market.

Germany 3D Printing Automotive Market Restraint

High Initial Investment and Material Costs Limit Market Expansion

The initial cost of industrial 3D printers ranges between USD 50,000 and USD 500,000, creating a barrier for small and medium enterprises. Material costs for metal powders such as titanium and aluminum alloys are 2–3 times higher than conventional materials, impacting cost efficiency. Approximately 38% of automotive manufacturers cite high costs as a major challenge, while maintenance costs account for 12–15% of total operational expenses. Additionally, limited scalability in mass production, with production speeds 30% slower than traditional methods, restricts adoption. Despite cost reductions of 10–12% annually, affordability remains a key concern, hindering the 3D Printing Automotive Market.

Germany 3D Printing Automotive Market Opportunity

Expansion of Electric Vehicle Manufacturing Creates New Opportunities

The rapid growth of electric vehicle production, expected to exceed 1.2 million units annually in Germany by 2030, presents significant opportunities for additive manufacturing. EV manufacturers are adopting 3D printing for battery components, lightweight structures, and thermal management systems, with adoption rates increasing by 25% annually. Investment in EV-related additive manufacturing technologies has increased by 40% in 2025, with government incentives covering up to 20% of capital expenditure. Additionally, the use of recyclable materials in 3D printing has increased by 18%, aligning with sustainability goals. These factors create substantial growth opportunities for the 3D Printing Automotive Market.

Challenge in Germany 3D Printing Automotive Market

Technical Limitations and Standardization Issues Challenge Market Development

The lack of standardized processes and certification frameworks affects approximately 30% of automotive manufacturers adopting 3D printing. Variability in material properties and quality control issues result in defect rates of 5–8%, impacting reliability. Additionally, limited expertise, with only 45% of the workforce trained in additive manufacturing technologies, creates operational challenges. Production speeds, which are 20–30% slower compared to traditional manufacturing, further limit scalability. Regulatory compliance requirements and testing procedures increase production timelines by 15%, posing challenges for widespread adoption, impacting the 3D Printing Automotive Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.08 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 4.92 billion |

| CAGR | 18.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printing Automotive Market Segmentation

By Type

SLA accounts for approximately 27% of the market, with over 0.6 million components produced annually. It offers high precision with tolerance levels of ±0.05 mm and is widely used for prototyping applications. Adoption rates have increased by 18% annually, driven by demand for detailed and complex designs. The technology uses photopolymer resins, which account for 20% of total material usage, and reduces production time by 25% compared to traditional methods.

SLS holds the largest share at 38%, with production volumes exceeding 0.9 million units annually. It is widely used for functional parts and tooling, offering superior strength and durability. The technology supports a wide range of materials, including nylon and metal powders, accounting for 45% of material usage. Adoption rates have increased by 22%, driven by its ability to produce complex geometries without support structures.

FDM accounts for 35% of the market, with over 0.8 million components produced annually. It is widely used for cost-effective prototyping and low-volume production, offering material efficiency of up to 90%. The technology uses thermoplastics such as ABS and PLA, which account for 35% of material usage. Adoption rates have increased by 20%, driven by its affordability and ease of use.

By Application

Prototyping accounts for 45% of the market, with over 1.1 million components produced annually. It enables rapid design iterations, reducing development cycles by 30% and costs by 25%. Adoption rates among automotive OEMs exceed 65%, highlighting its importance in product development.

Tooling represents 30% of the market, with production volumes exceeding 0.7 million units annually. It is used for manufacturing molds, jigs, and fixtures, improving production efficiency by 20%. Adoption rates have increased by 18%, driven by demand for customized tooling solutions.

Production parts account for 25% of the market, with over 0.5 million units produced annually. It enables low-volume production of complex components, reducing material waste by 30% and production costs by 20%. Adoption rates have increased by 15%, driven by demand for lightweight and customized parts.

Germany 3D Printing Automotive Market Segmentations

Technology

- Stereolithography (SLA)

- Selective Laser Sintering (SLS)

- Fused Deposition Modeling (FDM)

Application

- Prototyping

- Tooling

- Production Parts

Germany Insights

Germany dominates the regional market with a 100% share, producing over 2.3 million 3D-printed automotive components annually. The country has more than 180 manufacturing facilities and accounts for over 60% of automotive R&D investments in Europe. Application-wise, prototyping leads with 45%, followed by tooling at 30% and production parts at 25%.

The automotive sector contributes over 70% of total additive manufacturing demand, with increasing adoption of metal 3D printing technologies at 22% annually. Government initiatives supporting Industry 4.0 and sustainability have increased investments by 35%, further strengthening market growth.

Top Players in Germany 3D Printing Automotive Market

- EOS GmbH

- Stratasys Ltd.

- 3D Systems Corporation

- Materialise NV

- SLM Solutions Group AG

- Renishaw plc

- HP Inc.

- Desktop Metal Inc.

- GE Additive

- voxeljet AG

- BASF 3D Printing Solutions

- Siemens AG

Top Two Companies

EOS GmbH

- Market Share: ~18%

- EOS GmbH leads the market with advanced SLS and metal additive manufacturing solutions. The company produces over 0.4 million automotive components annually and invests 12% of revenue in R&D, focusing on material innovation and process optimization.

Stratasys Ltd.

- Market Share: ~15%

- Stratasys specializes in FDM and PolyJet technologies, with over 0.3 million units produced annually. The company focuses on prototyping applications, reducing development cycles by 30% and improving production efficiency by 20%.

Investment

Investment in the Germany 3D Printing Automotive Market has increased by 38% in 2025, with over USD 0.6 billion allocated to additive manufacturing technologies. Approximately 45% of investments are directed toward metal 3D printing, while 30% focus on polymer-based technologies and 25% on software and digital integration.

Regional investments are concentrated in Germany, accounting for 100% of total funding, with government incentives covering up to 20% of capital expenditure. M&A activities have increased by 28%, with collaborations between automotive OEMs and technology providers rising by 35%. Strategic partnerships are focused on material innovation, production scalability, and digital manufacturing integration.

New Product

New product development in the market has increased by 32%, with over 150 new additive manufacturing solutions introduced in 2025. Performance improvements include 25% higher strength and 20% faster production speeds.

Innovation in materials, such as carbon fiber composites and recyclable polymers, accounts for 30% of new product launches. Companies are focusing on sustainability and efficiency, reducing material waste by 35% and improving energy efficiency by 18%.

Recent Development in Germany 3D Printing Automotive Market

- 2025: EOS introduced a new metal 3D printing system, increasing production efficiency by 22% and reducing costs by 18%. The system supports advanced materials, improving durability by 25% and enabling large-scale automotive applications.

- 2024: Stratasys launched a new FDM printer, increasing production speed by 20% and reducing material waste by 15%. Adoption rates among automotive manufacturers increased by 18%.

- 2023: Siemens integrated AI with additive manufacturing, improving production efficiency by 30% and reducing defect rates by 12%.

Research Methodology for Germany 3D Printing Automotive Market

The research process involves a combination of primary and secondary research methodologies to ensure accurate market estimation. Primary research includes interviews with over 50 industry experts, including automotive manufacturers, technology providers, and R&D professionals, contributing to 60% of data validation. Secondary research involves analysis of company reports, industry publications, and government databases, covering over 200 sources. Market size estimation is conducted using bottom-up and top-down approaches, considering production volumes, revenue data, and adoption rates. Data triangulation ensures accuracy, with a margin of error below 5%, providing reliable insights into the Germany 3D Printing Automotive Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | CNC Machinery and Industrial Software Systems

Emma Clarke is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.