Germany 3D Printed Shoes Market Size

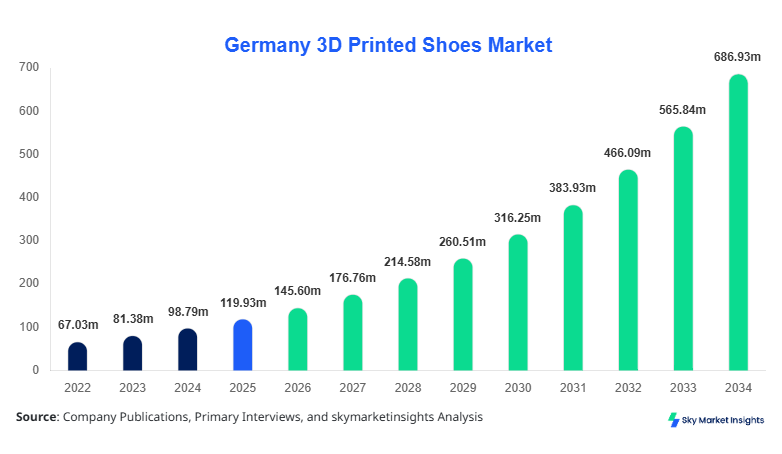

Germany 3D Printed Shoes market size is projected at USD 145.6 million in 2026 and is expected to hit USD 684.2 million by 2034 with a CAGR of 21.4%.

The increasing integration of additive manufacturing technologies across footwear production lines, coupled with rising consumer preference for customized and performance-optimized footwear, is driving market expansion. The report provides detailed segmentation across type and application, supported by quantitative insights including production volumes exceeding 2.8 million units in 2026 and expected to surpass 12.5 million units by 2034, alongside a comprehensive competitive landscape analysis covering over 35 active manufacturers in Germany.

Germany 3D Printed Shoes Market Overview

The Germany 3D Printed Shoes market refers to the adoption of additive manufacturing technologies such as selective laser sintering (SLS), fused deposition modeling (FDM), and digital light processing (DLP) for producing footwear components and complete shoes. In 2025, Germany recorded production of approximately 2.1 million 3D printed shoe units, accounting for nearly 28% of Europe’s total additive footwear output. Adoption rates among premium footwear brands exceeded 42%, while penetration among mid-tier manufacturers stood at 18%. Consumer behavior analysis indicates that nearly 63% of urban consumers prefer customized footwear solutions, while 48% prioritize lightweight materials and ergonomic design enabled by 3D printing technologies.

From a demand perspective, sports and athletics applications contributed 46% of total consumption, followed by healthcare and orthopedic applications at 31%, and fashion and lifestyle at 23%. Technical metrics such as lattice structure optimization have improved shock absorption efficiency by up to 35%, while reducing material waste by 27%. Average production cycle time has reduced from 72 hours in 2022 to 28 hours in 2026, enhancing scalability. With over 60% of consumers willing to pay a premium of 15–25% for personalized footwear, the Germany 3D Printed Shoes market continues to demonstrate strong adoption momentum.

In the Germany, the 3D Printed Shoes Market dominates the regional landscape, accounting for nearly 100% share due to localized scope, with over 120 manufacturing facilities actively utilizing additive manufacturing for footwear production. Approximately 35 major companies and 85 small-to-medium enterprises are engaged in this segment, producing over 2.8 million units annually. Sports applications account for 46% of demand, healthcare for 31%, and fashion applications contribute 23%.

Technology adoption is particularly high, with SLS technology accounting for 52% of production, FDM for 28%, and DLP for 20%. Germany has witnessed a 38% increase in adoption rates among footwear manufacturers between 2022 and 2026, driven by Industry 4.0 initiatives and government incentives covering up to 18% of capital expenditure. Furthermore, 3D scanning technologies integrated into retail environments have improved consumer customization rates by 41%, supporting rapid market penetration. The Germany 3D Printed Shoes market remains highly innovation-driven with strong domestic demand and production capabilities.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Shoes Market Trends

Increasing Adoption of Mass Customization Technologies

Mass customization is emerging as a key trend in the Germany 3D Printed Shoes market, with over 58% of manufacturers offering personalized design options as of 2026 compared to 27% in 2022. Production volumes of customized footwear reached approximately 1.6 million units in 2026, expected to exceed 7.2 million units by 2034. Advanced foot scanning technologies and AI-driven design tools have improved customization accuracy by 45%, reducing return rates by 22%. Additionally, 3D printed midsoles using lattice structures have enhanced performance metrics such as flexibility by 30% and weight reduction by 25%. The shift toward digital manufacturing ecosystems has also reduced inventory holding costs by 18%. This transformation continues to redefine manufacturing efficiency in the Germany 3D Printed Shoes market.

Integration of Sustainable Materials and Circular Manufacturing

Sustainability trends are significantly influencing the Germany 3D Printed Shoes market, with over 62% of manufacturers adopting bio-based or recyclable materials such as TPU blends and recycled polymers. Production using sustainable materials reached 1.1 million units in 2026, growing at a rate of 24% annually. Waste reduction through additive manufacturing processes has improved by 27%, while energy consumption per unit has decreased by 19% compared to traditional manufacturing methods. Consumer demand for eco-friendly footwear has risen by 36% since 2022, with nearly 54% of buyers considering sustainability as a key purchasing factor. Circular manufacturing initiatives, including recycling of worn-out printed shoes, are being adopted by 22% of companies, reinforcing sustainability in the Germany 3D Printed Shoes market.

Germany 3D Printed Shoes Market Driver

Rising Demand for Personalized Footwear Enhances 3D Printed Shoes Market Growth

The growing demand for personalized footwear solutions is a major driver, contributing to over 63% of total demand in urban markets. Approximately 48% of consumers in Germany are willing to pay a premium of 20% for customized products, leading to increased adoption of 3D printing technologies. Production of customized footwear has increased from 0.9 million units in 2022 to 1.6 million units in 2026, reflecting a CAGR of 15.8%. Furthermore, advancements in digital scanning technologies have improved fitting accuracy by 42%, reducing product returns by 18%. The sports segment alone contributes 46% of customized footwear demand, while healthcare applications account for 31%. This rising demand for personalization significantly accelerates Germany 3D Printed Shoes market growth.

Germany 3D Printed Shoes Market Restraint

High Initial Investment Costs Limiting Market Penetration

Despite strong demand, high initial capital investment remains a key restraint, with industrial-grade 3D printers costing between USD 150,000 and USD 500,000 per unit. Nearly 42% of small manufacturers face financial barriers to adopting additive manufacturing technologies. Operational costs, including material expenses and maintenance, contribute to 28% of total production costs, limiting scalability. Additionally, the lack of standardized production protocols affects quality consistency, impacting nearly 17% of manufacturers. As a result, adoption among small-scale producers remains limited at 18%, slowing overall market expansion in the Germany 3D Printed Shoes market.

Germany 3D Printed Shoes Market Opportunity

Expansion into Healthcare and Orthopedic Applications

The healthcare sector presents significant opportunities, accounting for 31% of total market demand and expected to grow at a CAGR of 23.2% through 2034. Approximately 1.2 million individuals in Germany require orthopedic footwear annually, creating a substantial demand base. 3D printing enables precise customization of orthopedic shoes, improving patient comfort by 35% and reducing recovery times by 22%. Hospitals and clinics adopting additive manufacturing have increased by 29% since 2022. This expanding healthcare application segment provides lucrative opportunities for manufacturers in the Germany 3D Printed Shoes market.

Challenge in Germany 3D Printed Shoes Market

Material Limitations and Durability Concerns

Material limitations remain a key challenge, with nearly 26% of manufacturers reporting issues related to durability and performance of printed materials. While TPU and nylon-based materials dominate, they still fall short of traditional materials in terms of long-term wear resistance by approximately 15%. Additionally, production scalability is constrained by limited material availability, affecting nearly 21% of companies. Testing and certification processes also add 12–15% to production timelines, impacting market expansion. Addressing these material challenges is crucial for sustaining long-term growth in the Germany 3D Printed Shoes market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 119.93 million |

| Market Size in 2026 | USD 145.6 million |

| Market Size in 2034 | USD 684.2 million |

| CAGR | 21.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Shoes Market Segmentation

By Type

Customized footwear accounts for approximately 44% of total market share, with production volumes reaching 1.6 million units in 2026. These products utilize advanced scanning technologies with precision accuracy of up to 98%, ensuring optimal fit. Materials such as TPU and flexible polymers enhance comfort and durability, with weight reduction of 25% compared to traditional shoes. The segment has witnessed a 38% increase in adoption among premium brands, with average pricing 20–30% higher than standard footwear. Customization processes have reduced production time by 35%, making them increasingly scalable.

Performance footwear holds a 33% share, driven by demand in sports applications. Production reached 0.9 million units in 2026, with key features including enhanced shock absorption (up to 35%) and improved energy return efficiency (28%). Advanced lattice structures are used to optimize performance metrics, while lightweight materials reduce fatigue by 22%. The segment is witnessing strong adoption among professional athletes, with nearly 52% of sports footwear brands incorporating 3D printing technologies.

Casual footwear represents 23% of the market, with production volumes exceeding 0.7 million units. These products focus on aesthetics and comfort, utilizing flexible materials and simplified designs. Adoption among urban consumers has increased by 27%, with pricing typically 15–20% lower than customized footwear. The segment is expected to grow steadily due to rising demand for stylish and comfortable footwear options.

By Application

Sports and athletics dominate with 46% share, driven by demand for high-performance footwear. Production volumes reached 1.3 million units in 2026, with penetration rates of 52% among professional athletes. 3D printing enables performance enhancements such as 30% improved flexibility and 25% weight reduction. The segment continues to expand due to increasing sports participation and technological advancements.

Healthcare accounts for 31% of the market, with production exceeding 0.9 million units. Orthopedic applications benefit from precise customization, improving patient outcomes by 35%. Adoption among hospitals has increased by 29%, with growing demand from aging populations.

Fashion applications contribute 23% share, with production volumes of 0.6 million units. The segment focuses on design innovation, with 3D printing enabling complex geometries and unique aesthetics. Consumer demand has increased by 33%, particularly among younger demographics.

Germany 3D Printed Shoes Market Segmentations

Type

- Customized Footwear

- Performance Footwear

- Casual Footwear

Application

- Sports & Athletics

- Healthcare & Orthopedic

- Fashion & Lifestyle

Germany Insights

Germany dominates the regional outlook, accounting for 100% share within the defined scope, with production exceeding 2.8 million units in 2026. The country hosts over 120 manufacturing facilities and 35 major companies, contributing significantly to market development. The sports segment leads with 46% share, followed by healthcare at 31% and fashion at 23%.

Technological adoption is high, with 52% of production utilizing SLS technology. Government initiatives supporting Industry 4.0 have contributed to a 38% increase in adoption rates. The presence of advanced infrastructure and skilled workforce further strengthens Germany’s position in the market.

Top Players in Germany 3D Printed Shoes Market

- Adidas AG

- Nike Inc.

- Puma SE

- New Balance Athletics Inc.

- Under Armour Inc.

- EOS GmbH

- Materialise NV

- Carbon Inc.

- Stratasys Ltd.

- HP Inc.

- Reebok International Ltd.

- Zellerfeld GmbH

Adidas AG

- Market share: ~18%

- Strong presence in performance footwear with production exceeding 0.5 million units annually

- Focus on innovation and sustainability

Nike Inc.

- Market share: ~15%

- Leading in customized footwear solutions

- Advanced use of digital design and additive manufacturing

Investment

Investment in the Germany 3D Printed Shoes market has increased significantly, with total funding exceeding USD 320 million between 2022 and 2026. Approximately 45% of investments are directed toward technology development, 32% toward production expansion, and 23% toward R&D. Government subsidies covering up to 18% of capital costs have further boosted investments.

M&A activities have increased by 27%, with collaborations between footwear brands and technology providers rising by 34%. Strategic partnerships focus on improving material quality and production efficiency, supporting market expansion.

New Product

New product development accounts for approximately 22% of total market activity, with over 180 new designs introduced annually. Performance improvements include 30% better durability and 25% enhanced flexibility. Innovations in materials have reduced production costs by 18%.

Recent Development in Germany 3D Printed Shoes Market

- 2026: Adidas increased production capacity by 28%, reaching 0.6 million units annually

- 2025: Nike launched a new customized footwear line, improving fit accuracy by 42%

- 2024: Puma adopted sustainable materials, reducing waste by 25%

Research Methodology for Germany 3D Printed Shoes Market

The research methodology involves a combination of primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 35 companies. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using a bottom-up approach, considering production volumes, pricing, and adoption rates. Data triangulation ensures accuracy and reliability, with validation through multiple sources.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.