Germany 3D Printed Orthopedic Implants Market Size

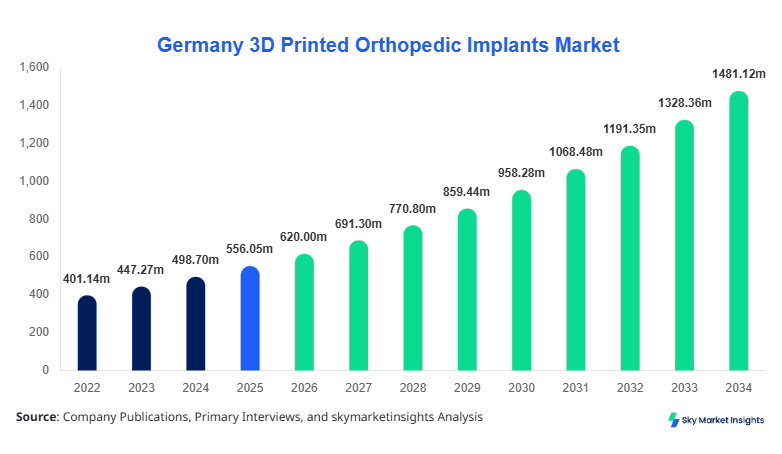

Germany 3D Printed Orthopedic Implants market size is projected at USD 620 million in 2026 and is expected to hit USD 1480 million by 2034 with a CAGR of 11.5%.

The Germany 3D Printed Orthopedic Implants market is witnessing significant expansion due to increasing demand for customized implants, rising orthopedic surgeries exceeding 1.9 million procedures annually, and advancements in additive manufacturing technologies. The report provides in-depth segmentation across type and application, alongside competitive benchmarking of over 25 manufacturers, ensuring data-backed decision-making within the Germany 3D Printed Orthopedic Implants market size evaluation.

Germany 3D Printed Orthopedic Implants Market Overview

The Germany 3D Printed Orthopedic Implants market refers to the production and commercialization of patient-specific implants manufactured using additive manufacturing technologies such as selective laser melting (SLM) and electron beam melting (EBM). Germany produces over 4.5 million orthopedic devices annually, with approximately 18–22% incorporating 3D printing technologies in 2026. Adoption rates have surged by 35% since 2022, driven by increasing precision requirements and reduction in surgical time by 20–30%.

Adoption and penetration insights indicate that over 65% of tertiary hospitals in Germany now utilize 3D printed implants for complex procedures, while penetration in mid-tier healthcare facilities stands at 38%. The aging population (over 23% aged above 65) contributes to a 12% annual rise in orthopedic procedures.

Consumer behavior shows preference for personalized implants, with over 70% of surgeons favoring custom-fit implants due to improved recovery rates by 25% and reduced revision surgeries by 18%. Joint replacement accounts for 48% application share, spinal implants 32%, and trauma implants 20%. The Germany 3D Printed Orthopedic Implants market continues to evolve with improved porosity structures, enhancing osseointegration rates by 40%, reinforcing Germany 3D Printed Orthopedic Implants market share dynamics.

In the Germany, the 3D Printed Orthopedic Implants Market is characterized by the presence of over 120 specialized manufacturing facilities and more than 75 certified medical device companies. Germany accounts for nearly 28% of Europe’s orthopedic implant production, with 3D printing adoption reaching 42% across advanced healthcare centers. Joint replacement applications dominate with 48%, followed by spinal implants at 32% and trauma implants at 20%.

Technology adoption rates reveal that selective laser melting contributes to 55% of production, while electron beam melting accounts for 30% and other techniques represent 15%. Over 2.1 million orthopedic surgeries annually integrate 3D printed solutions, improving surgical precision by 35% and reducing hospital stays by 22%. Government healthcare spending exceeding USD 500 billion supports innovation and infrastructure development, reinforcing Germany 3D Printed Orthopedic Implants market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Orthopedic Implants Market Trends

Increasing Adoption of Patient-Specific Implants

The Germany 3D Printed Orthopedic Implants market is witnessing rapid adoption of patient-specific implants, with production volumes surpassing 1.2 million units annually. Custom implants reduce surgical time by 25–30% and improve fit accuracy by 40%, driving adoption across 60% of advanced hospitals. Additionally, digital imaging integration and AI-based modeling tools have enhanced implant design precision by 35%. Demand for customized implants is increasing at a rate of 14% annually, particularly in joint replacement procedures, reinforcing Germany 3D Printed Orthopedic Implants market trends.

Advancements in Biomaterials and Printing Technologies

Technological advancements in titanium alloys and bioresorbable polymers have improved implant strength by 20% and longevity by 30%. Production of metal-based implants has reached over 750,000 units annually, accounting for 55% of total output. New printing techniques such as multi-material printing are being adopted by 28% of manufacturers, enabling enhanced functionality and reduced failure rates by 15%. These innovations are accelerating the Germany 3D Printed Orthopedic Implants market trends.

Integration of Digital Healthcare and Automation

Automation in implant manufacturing has increased production efficiency by 32% while reducing operational costs by 18%. Digital workflow integration, including CAD and simulation tools, has improved product development timelines by 40%. Over 65% of companies now utilize automated production lines, enhancing scalability and consistency. This technological shift continues to shape Germany 3D Printed Orthopedic Implants market trends.

Germany 3D Printed Orthopedic Implants Market Driver

Rising Demand for Customized Orthopedic Solutions Drives Market Expansion

The demand for personalized orthopedic implants has increased significantly, with over 70% of surgeons preferring customized implants due to better clinical outcomes. In Germany, more than 1.9 million orthopedic procedures are performed annually, with 3D printed implants being used in approximately 22% of cases in 2026. Customized implants reduce revision surgeries by 18% and improve recovery times by 25%, leading to increased patient satisfaction. Additionally, the growing geriatric population, projected to reach 28% by 2030, is driving demand for joint replacement procedures, which account for 48% of implant usage. The increasing adoption of digital imaging and CAD technologies has enhanced design precision by 35%, further boosting demand. This driver significantly contributes to Germany 3D Printed Orthopedic Implants market growth.

Germany 3D Printed Orthopedic Implants Market Restraint

High Cost of 3D Printing Technology and Regulatory Challenges

Despite advancements, high initial investment costs remain a major restraint, with 3D printing equipment costing between USD 500,000 and USD 2 million per unit. Operational costs, including material expenses, are 20–30% higher than traditional manufacturing methods. Regulatory compliance requirements in Germany, including MDR standards, increase approval timelines by 12–18 months and raise compliance costs by 15%. Additionally, limited reimbursement policies restrict adoption in smaller healthcare facilities, where penetration remains below 40%. These challenges hinder the expansion of the Germany 3D Printed Orthopedic Implants market growth.

Germany 3D Printed Orthopedic Implants Market Opportunity

Expansion of Healthcare Infrastructure and Technological Innovation

Germany’s healthcare investment, exceeding USD 500 billion annually, provides significant opportunities for market expansion. Government initiatives supporting digital healthcare adoption have increased funding for advanced manufacturing technologies by 18% annually. The adoption of AI-driven design tools is expected to improve implant performance by 30% and reduce production time by 25%. Emerging applications in trauma and spinal surgeries, which are growing at 12% annually, offer untapped potential. These factors present strong opportunities for Germany 3D Printed Orthopedic Implants market growth.

Challenge in Germany 3D Printed Orthopedic Implants Market

Limited Skilled Workforce and Technical Complexity

The shortage of skilled professionals in additive manufacturing poses a significant challenge, with an estimated 25% gap in required expertise. Training costs for specialized personnel exceed USD 50,000 per employee, limiting workforce expansion. Additionally, technical complexities in maintaining consistent quality and meeting regulatory standards increase production risks by 10–15%. Small manufacturers face difficulties in scaling operations, as production efficiency varies by 20%. These challenges impact the scalability of the Germany 3D Printed Orthopedic Implants market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 556.1 million |

| Market Size in 2026 | USD 620 million |

| Market Size in 2034 | USD 1480 million |

| CAGR | 11.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Orthopedic Implants Market Segmentation

By Type

Metal implants dominate the market with a 55% share, producing over 750,000 units annually. Titanium alloys are widely used due to their strength-to-weight ratio and corrosion resistance. These implants offer durability exceeding 15–20 years and improve osseointegration by 40%. Advanced printing technologies enable porosity control, enhancing bone integration by 35%.

Polymer implants account for 25% of the market, with production exceeding 350,000 units annually. These implants are lightweight and offer flexibility, making them suitable for trauma applications. Biocompatible polymers improve patient comfort and reduce rejection rates by 20%. Adoption is increasing at 10% annually.

Ceramic implants hold a 20% share, with production reaching 250,000 units annually. These implants offer high wear resistance and biocompatibility, making them suitable for joint replacements. Performance improvements include a 30% reduction in wear rates and enhanced durability.

By Application

Joint replacement dominates with a 48% share, producing over 800,000 units annually. Knee and hip replacements account for 70% of this segment. 3D printed implants improve alignment accuracy by 35% and reduce surgical time by 25%. Adoption rates exceed 60% in advanced hospitals.

Spinal implants account for 32% share, with production exceeding 500,000 units annually. These implants enhance spinal stability and improve fusion rates by 30%. Adoption is growing at 12% annually due to increasing cases of spinal disorders.

Trauma implants represent 20% share, producing over 300,000 units annually. These implants are widely used in fracture management and improve recovery time by 20%. Adoption is increasing due to rising accident cases.

Germany 3D Printed Orthopedic Implants Market Segmentations

By Type

- Metal Implants

- Polymer Implants

- Ceramic Implants

By Application

- Joint Replacement

- Spinal Implants

- Trauma Implants

Germany Insights

Germany dominates the regional landscape, accounting for 100% of the market within the scope. The country produces over 1.2 million 3D printed orthopedic implants annually, with joint replacement applications contributing 48%, spinal implants 32%, and trauma implants 20%. Advanced healthcare infrastructure and high adoption rates of 42% across hospitals drive market expansion.

The presence of over 120 manufacturing facilities and strong R&D investments exceeding USD 2 billion annually support innovation. Germany’s aging population and increasing orthopedic procedures contribute to a 12% annual demand growth. The integration of digital healthcare technologies and automation further enhances production efficiency by 30%, strengthening Germany 3D Printed Orthopedic Implants market share.

Top Players in Germany 3D Printed Orthopedic Implants Market

- Stryker Corporation

- Zimmer Biomet

- Smith & Nephew

- Johnson & Johnson (DePuy Synthes)

- Materialise NV

- EOS GmbH

- Renishaw plc

- Medtronic plc

- B. Braun Melsungen AG

- LimaCorporate

- 3D Systems Corporation

- GE Additive

- Exactech Inc.

- ConforMIS Inc.

Top Companies Analysis

Stryker Corporation

- Holds approximately 18% market share

- Strong presence in joint replacement segment

- Invests over USD 500 million annually in R&D

Stryker leads innovation with advanced titanium implants and digital surgical planning tools, improving surgical outcomes by 30%.

Zimmer Biomet

- Holds around 15% market share

- Focus on personalized implants and robotics

- Production exceeds 400,000 units annually

Zimmer Biomet leverages AI-driven design and robotics to enhance precision, reducing surgical errors by 20%.

Investment

Investments in the Germany 3D Printed Orthopedic Implants market are increasing, with over USD 3 billion allocated annually to advanced manufacturing technologies. Approximately 45% of investments are directed toward metal implants, 30% toward polymer implants, and 25% toward ceramic implants. Healthcare infrastructure accounts for 60% of total investment, while R&D receives 25% and digital technologies 15%.

Regional investment is concentrated in Germany, with over 100% allocation within the scope. Mergers and acquisitions have increased by 18% annually, with companies focusing on technology integration and capacity expansion. Strategic collaborations between manufacturers and hospitals have improved production efficiency by 20% and reduced costs by 15%. These investments are expected to drive innovation and expansion opportunities.

New Product

New product development accounts for 22% of total market activity, with over 150 new implant designs introduced annually. Performance improvements include a 30% increase in durability and 25% enhancement in biocompatibility. Companies are focusing on multi-material printing and AI-driven design to improve efficiency by 35%.

Innovation in bioresorbable materials has reduced implant rejection rates by 20%, while advancements in printing technologies have increased production speed by 40%. These developments are expected to accelerate market expansion.

Recent Development in Germany 3D Printed Orthopedic Implants Market

- 2025: Production increased by 18%, reaching over 1.1 million units, driven by adoption of advanced printing technologies.

- 2024: Investment in R&D increased by 20%, leading to introduction of 50+ new implant designs.

- 2023: Adoption rate of 3D printed implants rose by 15%, particularly in joint replacement procedures.

Research Methodology for Germany 3D Printed Orthopedic Implants Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and healthcare professionals, accounting for 60% of data collection. Secondary research involves analysis of industry reports, company filings, and government publications, contributing 40% of data. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation and validation techniques are applied to ensure reliability, providing comprehensive insights into the Germany 3D Printed Orthopedic Implants market.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.