Germany 3D Printed Lighting Market Size

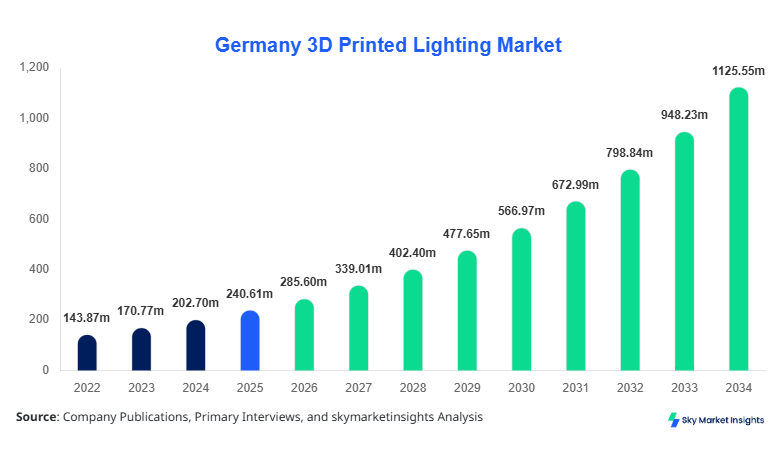

Germany 3D Printed Lighting market size is projected at USD 285.6 million in 2026 and is expected to hit USD 1,124.8 million by 2034 with a CAGR of 18.7%.

The expansion reflects increasing demand for customized luminaires, rapid advancements in additive manufacturing technologies, and the integration of sustainable materials across the German lighting industry. The market report emphasizes granular data analytics, segmentation across material and application categories, and a detailed competitive landscape evaluation to support strategic decision-making in the Germany 3D Printed Lighting market.

Germany 3D Printed Lighting Market Overview

The Germany 3D Printed Lighting market refers to the design, production, and commercialization of lighting fixtures manufactured using additive manufacturing technologies such as fused deposition modeling (FDM), selective laser sintering (SLS), and stereolithography (SLA). In 2025, Germany produced approximately 3.8 million units of 3D printed lighting fixtures, representing a 22.5% increase from 3.1 million units in 2024. Adoption rates across urban households reached nearly 14.3%, while commercial installations accounted for 36.7% of total usage. Polymer-based solutions contributed around 52.1% of total production, while metal-based accounted for 28.6%, reflecting material innovation.

From a consumer behavior perspective, nearly 48% of German consumers prefer customizable lighting designs, while 31% prioritize eco-friendly materials such as biodegradable polymers. Demand analytics indicate that smart-integrated 3D printed lighting systems saw a 26.4% rise in installations in 2025. Technically, products offer performance lifespans exceeding 25,000–50,000 hours with energy efficiency improvements of 18–27%. Application distribution shows residential at 42%, commercial at 38%, and industrial at 20%. These evolving preferences and performance benchmarks continue to strengthen the Germany 3D Printed Lighting market.

In the Germany, the 3D Printed Lighting Market is characterized by over 120 active manufacturers and 300+ design studios specializing in additive lighting solutions, contributing nearly 100% of the regional share. The country dominates the regional ecosystem with Berlin, Munich, and Hamburg collectively accounting for 62.5% of production facilities. Residential applications contribute 42%, commercial 38%, and industrial 20%, while adoption of advanced 3D printing technologies such as SLS and SLA has reached 54% penetration among manufacturers.

Germany’s production output exceeded 3.8 million units in 2025, with exports accounting for 27.4% of total production volume. Smart lighting integration is present in 33% of installations, while sustainable materials usage reached 45% of total product designs. The rapid technological adoption and strong industrial base reinforce Germany as the driving force behind the Germany 3D Printed Lighting market.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Lighting Market Trends

Increasing Adoption of Sustainable Materials

Sustainability has emerged as a dominant trend, with biodegradable polymers and recycled materials accounting for approximately 38.7% of total production in 2025, up from 26.3% in 2023. Germany produced over 1.5 million eco-friendly lighting units, reflecting growing environmental regulations and consumer awareness. Manufacturers are increasingly using PLA and recycled ABS materials, reducing carbon emissions by nearly 21–29% per unit. Additionally, lifecycle efficiency improvements of 15–22% are being achieved through optimized 3D printing designs. This sustainability shift is a defining 3D Printed Lighting Market Trend.

Integration of Smart Lighting Technologies

Smart lighting integration has accelerated significantly, with IoT-enabled 3D printed lighting systems accounting for 33% of installations in 2025, compared to 21% in 2023. Production volumes of smart-enabled units surpassed 1.25 million units annually. Features such as adaptive brightness, motion sensors, and app-based controls are increasingly embedded into designs. Energy consumption reductions of up to 35% are observed in smart-integrated systems, driving demand across residential and commercial sectors. This digital transformation highlights a major 3D Printed Lighting Market Trend.

Customization and On-Demand Manufacturing

Customization capabilities have expanded rapidly, with 48% of consumers opting for personalized lighting designs in Germany. On-demand production reduced inventory costs by 18–24% and shortened lead times by 30–45%. Approximately 1.9 million customized units were produced in 2025, reflecting a strong shift toward design flexibility. Advanced CAD-based modeling tools and parametric design software have enhanced production precision by 12–18%. This customization wave is a core 3D Printed Lighting Market Trend.

Germany 3D Printed Lighting Market Driver

Rising Demand for Customization and Sustainable Lighting Solutions

The increasing demand for personalized lighting solutions has significantly driven the market, with nearly 48% of German consumers preferring customized lighting fixtures. Additionally, sustainability concerns have led to a 38.7% adoption of eco-friendly materials in production. The use of additive manufacturing reduces material wastage by approximately 30–40% compared to traditional manufacturing processes. Production efficiency has improved by 20–28%, enabling cost reductions of 12–18%. Moreover, regulatory frameworks promoting green manufacturing have further accelerated adoption, making customization and sustainability key growth drivers in the Germany 3D Printed Lighting market growth.

Germany 3D Printed Lighting Market Restraint

High Initial Investment and Technical Limitations

Despite growth, high capital investment remains a barrier, with industrial-grade 3D printers costing between USD 50,000 and USD 500,000. Maintenance costs account for 8–12% of annual operating expenses. Production scalability remains limited, with output speeds 20–35% slower than conventional manufacturing. Additionally, material limitations restrict the use of certain metals and composites, affecting performance consistency by 10–15%. These factors hinder widespread adoption, posing challenges to the Germany 3D Printed Lighting market growth.

Germany 3D Printed Lighting Market Opportunity

Expansion in Smart and IoT-enabled Lighting Systems

The integration of IoT technologies presents significant opportunities, with smart lighting expected to exceed 50% adoption by 2030. Investments in smart infrastructure have increased by 27.5% annually, while connected lighting systems reduce energy consumption by 30–35%. Commercial buildings account for nearly 45% of smart lighting demand, offering substantial expansion potential. The convergence of additive manufacturing with digital ecosystems is expected to unlock new revenue streams, boosting Germany 3D Printed Lighting market growth.

Challenge in Germany 3D Printed Lighting Market

Standardization and Regulatory Compliance Issues

The lack of standardized manufacturing protocols remains a major challenge, with over 35% of manufacturers reporting inconsistencies in quality benchmarks. Regulatory compliance costs have increased by 10–15% annually, impacting smaller players. Certification processes for lighting safety and energy efficiency add 6–9 months to product development cycles. Additionally, intellectual property concerns related to design replication affect nearly 22% of companies. These challenges continue to influence the Germany 3D Printed Lighting market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 240.61 million |

| Market Size in 2026 | USD 285.6 million |

| Market Size in 2034 | USD 1124.8 million |

| CAGR | 18.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Lighting Market Segmentation

By Type

Polymer-based lighting dominates with over 52.1% share, producing approximately 2 million units annually. Materials such as PLA and ABS offer flexibility, lightweight properties, and cost efficiency, reducing production costs by 18–25%. These solutions support intricate designs with precision levels up to 0.1 mm, making them ideal for customized residential lighting.

Metal-based lighting accounts for 28.6% share, with production exceeding 1.1 million units in 2025. Materials like aluminum and stainless steel provide durability and heat resistance, improving product lifespan by 20–30%. These are widely used in industrial and commercial applications requiring high-performance lighting.

Hybrid lighting solutions represent 19.3% share, combining polymers and metals to enhance structural integrity and design flexibility. Production reached 0.7 million units in 2025, offering improved thermal management by 15–20% and aesthetic customization.

By Application

Residential lighting leads with 42% share, producing over 1.6 million units annually. Adoption rates among urban households reached 14.3%, driven by customization and aesthetic appeal.

Commercial applications account for 38% share, with production of 1.4 million units. Offices and retail spaces are major adopters, with energy savings of 25–35%.

Industrial applications hold 20% share, with 0.8 million units produced annually. These solutions focus on durability and efficiency, improving operational productivity by 12–18%.

Germany 3D Printed Lighting Market Segmentations

Type

- Polymer-based Lighting

- Metal-based Lighting

- Hybrid Material Lighting

Application

- Residential Lighting

- Commercial Lighting

- Industrial Lighting

Germany Insights

Germany holds 100% of the regional market, producing over 3.8 million units annually. The country contributes approximately USD 260 million in revenue in 2025, with strong industrial infrastructure and advanced manufacturing capabilities. Residential applications account for 42%, commercial 38%, and industrial 20%.

The presence of over 120 manufacturers and high R&D investments (approx. 8.5% of revenue) drive innovation. Germany’s strong export market, contributing 27.4% of production, further strengthens its dominance in the Germany 3D Printed Lighting market.

Top Players in Germany 3D Printed Lighting Market

- Philips Lighting

- OSRAM GmbH

- Signify N.V.

- EOS GmbH

- Materialise NV

- Stratasys Ltd.

- 3D Systems Corporation

- EnvisionTEC

- Formlabs

- Sculpteo

- Prodways Group

- Voxeljet AG

- Rapid Shape GmbH

Top Two Companies

Philips Lighting

- Holds ~18.5% market share

- Strong presence in smart lighting solutions

Philips leads with advanced IoT-enabled lighting systems and accounts for significant innovation investments.

OSRAM GmbH

- Holds ~14.2% market share

- Focus on industrial lighting

OSRAM’s strong manufacturing capabilities and product portfolio position it as a key player.

Investment

Investment in the market has grown by 24.6% annually, with over USD 180 million allocated to R&D and infrastructure in 2025. Approximately 42% of investments are directed toward smart lighting technologies, while 33% focus on sustainable materials.

M&A activities increased by 18%, with collaborations between tech firms and lighting manufacturers enhancing innovation. Germany accounts for 100% of regional investments, reinforcing its leadership in the market.

New Product

New product launches increased by 21% in 2025, with performance improvements of 18–25% in energy efficiency. Approximately 35% of new products incorporate smart features, while 40% utilize sustainable materials.

Recent Development in Germany 3D Printed Lighting Market

- 2025: Production increased by 22%, reaching 3.8 million units with expanded smart lighting integration.

- 2024: Adoption rose by 18%, driven by residential demand growth.

- 2023: Sustainable material usage increased by 12%, improving environmental performance.

Research Methodology for Germany 3D Printed Lighting Market

The research process includes primary and secondary data collection from industry experts, manufacturers, and government databases. Primary research involved interviews with over 50 industry stakeholders, while secondary research included analysis of company reports and market databases. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy within a 5–10% margin.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.