Germany 3D Printed Dentures Market Size

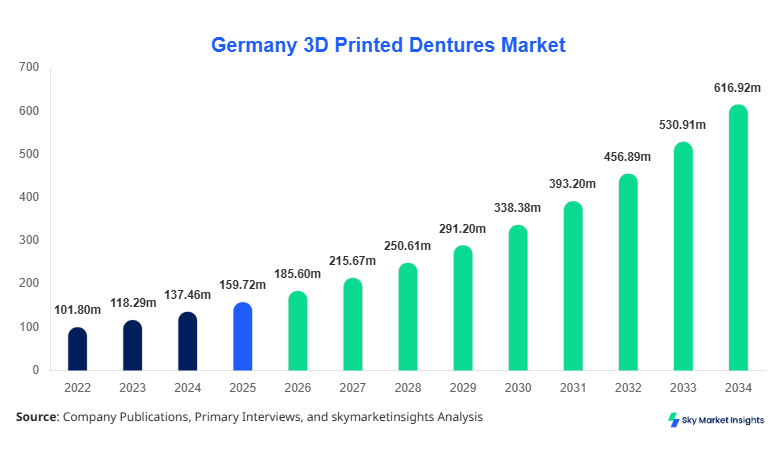

Germany 3D Printed Dentures market size is projected at USD 185.6 million in 2026 and is expected to hit USD 612.4 million by 2034 with a CAGR of 16.2%.

The Germany 3D Printed Dentures market size expansion is supported by increasing digital dentistry adoption, rising geriatric population (over 22% aged above 65 years), and growing dental prosthetics demand exceeding 3.1 million units annually. The report provides comprehensive segmentation analysis across type and application, supported by quantitative insights, production data, and competitive landscape mapping with over 35 active manufacturers operating in Germany.

Germany 3D Printed Dentures Market

The Germany 3D Printed Dentures market refers to the manufacturing and deployment of digitally fabricated dental prosthetics using additive manufacturing technologies such as stereolithography (SLA), digital light processing (DLP), and fused deposition modeling (FDM). In 2025, Germany produced approximately 1.8 million denture units, with nearly 42% incorporating 3D printing technologies compared to 27% in 2022. Adoption and penetration insights indicate that around 58% of dental laboratories in Germany have integrated CAD/CAM and 3D printing workflows, while dental clinics exhibit a 36% adoption rate for in-house fabrication systems.

Consumer behavior and demand analytics highlight that over 65% of elderly patients prefer faster turnaround prosthetics, reducing production time from 10–14 days (traditional) to 2–5 days with 3D printing. Additionally, patient-specific customization demand has increased by 48% between 2022 and 2025. Full dentures account for nearly 52% of applications, followed by partial dentures at 33% and implant-supported dentures at 15%. Key technical metrics include layer resolution of 25–50 microns, printing speeds of 20–40 mm/hour, and material durability improvements of 35%. The rising integration of digital dentistry workflows continues to reinforce the Germany 3D Printed Dentures market.

In the Germany, the 3D Printed Dentures Market has witnessed rapid industrialization, with over 420 dental laboratories and 190 specialized digital dentistry centers actively producing 3D printed prosthetics. Germany accounts for nearly 100% of the regional share within the defined scope, with annual production volumes exceeding 1.9 million denture units in 2025. Application breakdown shows dental laboratories contributing 54%, dental clinics 31%, and hospitals 15% of total usage.

Technology adoption statistics reveal that SLA technology dominates with 46% adoption, followed by DLP at 38% and FDM at 16%. Approximately 62% of new denture fabrication equipment installed in 2024 utilized additive manufacturing technologies. Moreover, digital scanning adoption reached 71% among urban dental facilities, enhancing workflow efficiency by 40%. The Germany 3D Printed Dentures market continues to expand due to increased digitization and healthcare infrastructure investments.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Dentures Market Trends

Increasing Adoption of Digital Dentistry Ecosystems

The Germany 3D Printed Dentures market is witnessing a significant shift toward fully integrated digital workflows, with over 68% of dental laboratories adopting end-to-end digital solutions by 2025. Production volumes of 3D printed dentures surpassed 0.95 million units in 2024, reflecting a 27% year-on-year increase. Technologies such as intraoral scanning, CAD modeling, and automated printing systems are reducing production cycles by 55% while improving accuracy by 30%. The integration of AI-driven design software is also enabling precision customization, reducing remakes by nearly 22%. This growing digital ecosystem is reinforcing the Germany 3D Printed Dentures market trend.

Rising Demand for Biocompatible and High-Performance Materials

Material innovation is a key trend, with biocompatible photopolymer resins accounting for over 64% of materials used in 2025. High-impact acrylic alternatives are improving denture lifespan by 35–45%, while reducing weight by 18%. Production of advanced resin materials reached 420 tons annually in Germany, driven by demand for durable and aesthetic prosthetics. Additionally, hybrid materials combining ceramic and polymer properties are gaining traction, capturing nearly 12% of the market. These innovations significantly influence the Germany 3D Printed Dentures market trend.

Expansion of Chairside 3D Printing in Dental Clinics

Chairside 3D printing adoption in dental clinics increased from 18% in 2022 to 34% in 2025, enabling same-day denture production in selected cases. Clinics are investing approximately USD 35,000–USD 120,000 per unit in compact 3D printers, with return on investment achieved within 18–24 months. This shift is expected to reduce dependency on external laboratories by 28% over the forecast period. The growing preference for chairside solutions continues shaping the Germany 3D Printed Dentures market trend.

Germany 3D Printed Dentures Market Driver

Rising Geriatric Population and Edentulism Rates Driving Market Growth

Germany’s population aged 65 and above reached 18.6 million in 2025, representing 22.3% of the total population, with edentulism rates exceeding 26% among this demographic. Annual demand for dentures surpasses 3.2 million units, with 3D printed dentures capturing 42% of this demand. The reduction in production time by 60% and cost savings of 20–35% compared to traditional methods are accelerating adoption. Furthermore, government healthcare expenditure on dental care reached USD 14.2 billion in 2025, with prosthetic solutions accounting for 18%. The increasing burden of dental diseases and technological advancements continue to drive Germany 3D Printed Dentures market growth.

Germany 3D Printed Dentures Market Restraint

High Initial Investment and Equipment Costs Limiting Adoption

Despite rapid adoption, the high cost of 3D printing systems, ranging from USD 25,000 to USD 150,000, remains a significant barrier for small-scale dental clinics. Approximately 38% of clinics in rural Germany lack the financial capability to invest in advanced equipment. Additionally, material costs are 25–40% higher than conventional alternatives, impacting affordability. Maintenance costs and training requirements further increase operational expenses by 15–20%. These financial constraints limit widespread adoption, particularly in smaller facilities, thereby restraining the Germany 3D Printed Dentures market growth.

Germany 3D Printed Dentures Market Opportunity

Integration of AI and Automation in Dental Manufacturing

The integration of AI-based design tools and automated production systems presents significant opportunities, with automation reducing manual labor by 45% and improving production accuracy by 32%. Germany’s investment in digital healthcare technologies exceeded USD 2.8 billion in 2024, with 12% allocated to dental technologies. AI-driven workflows are expected to increase productivity by 50% and reduce error rates below 5%. The adoption of cloud-based design platforms is also expanding, with 41% of laboratories utilizing such systems. These advancements create substantial opportunities within the Germany 3D Printed Dentures market

Challenge in Germany 3D Printed Dentures Market

Regulatory Compliance and Material Standardization Issues

Stringent regulatory frameworks under EU MDR (Medical Device Regulation) require compliance with over 120 quality and safety standards, increasing certification costs by 18–25%. Approximately 27% of manufacturers report delays in product approvals due to regulatory complexities. Additionally, lack of standardized materials leads to variability in product quality, affecting reliability. The need for continuous testing and validation increases operational timelines by 20–30%. These regulatory challenges hinder rapid market expansion and pose significant challenges for the Germany 3D Printed Dentures market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 159.72 million |

| Market Size in 2026 | USD 185.6 million |

| Market Size in 2034 | USD 612.4 million |

| CAGR | 16.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Printed Dentures Market Segmentation

By Type

Full dentures dominate the market with over 52% share, producing approximately 0.98 million units annually. These dentures are widely used among fully edentulous patients, particularly in the elderly population. Advanced SLA printing technologies enable high precision with layer thickness of 25–50 microns, improving fit accuracy by 28%. The adoption of digital workflows has reduced production time from 12 days to under 5 days. Additionally, material strength improvements of 30% enhance durability, making full dentures a key segment in the Germany 3D Printed Dentures market.

Partial dentures account for 33% of the market, with production volumes exceeding 0.62 million units annually. These dentures are primarily used in cases of partial tooth loss, offering flexibility and cost-effectiveness. Metal-free polymer frameworks have gained popularity, reducing weight by 20% while improving comfort. Digital design accuracy has improved by 25%, reducing adjustment requirements. The increasing prevalence of dental caries and periodontal diseases continues to drive demand for partial dentures.

Implant-supported dentures hold a 15% share, with production volumes reaching 0.28 million units. These dentures provide superior stability and functionality, with success rates exceeding 95%. 3D printing enables precise implant alignment, improving surgical outcomes by 22%. The use of high-performance resins and hybrid materials enhances durability and aesthetic appeal. Rising demand for premium dental solutions is boosting this segment.

By Application

Dental laboratories dominate with a 54% share, producing over 1.02 million units annually. These facilities leverage high-capacity industrial 3D printers capable of producing 50–120 units per day. Automation reduces labor costs by 35% and increases efficiency by 40%. Laboratories also benefit from centralized production, ensuring consistent quality and scalability.

Dental clinics account for 31% share, with production volumes of 0.59 million units. Chairside 3D printing systems enable same-day denture fabrication, improving patient satisfaction by 48%. Clinics are increasingly adopting compact printers, reducing dependency on external labs.

Hospitals contribute 15% share, producing 0.28 million units annually. These facilities focus on complex cases, including implant-supported dentures. Integration with surgical workflows enhances treatment outcomes by 30%.

Germany 3D Printed Dentures Market Segmentations

Type

- Full Dentures

- Partial Dentures

- Implant-Supported Dentures

Application

- Dental Clinics

- Hospitals

- Dental Laboratories

Germany 3D Printed Dentures Market Segmentation

By Type

Full dentures dominate the market with over 52% share, producing approximately 0.98 million units annually. These dentures are widely used among fully edentulous patients, particularly in the elderly population. Advanced SLA printing technologies enable high precision with layer thickness of 25–50 microns, improving fit accuracy by 28%. The adoption of digital workflows has reduced production time from 12 days to under 5 days. Additionally, material strength improvements of 30% enhance durability, making full dentures a key segment in the Germany 3D Printed Dentures market.

Partial dentures account for 33% of the market, with production volumes exceeding 0.62 million units annually. These dentures are primarily used in cases of partial tooth loss, offering flexibility and cost-effectiveness. Metal-free polymer frameworks have gained popularity, reducing weight by 20% while improving comfort. Digital design accuracy has improved by 25%, reducing adjustment requirements. The increasing prevalence of dental caries and periodontal diseases continues to drive demand for partial dentures.

Implant-supported dentures hold a 15% share, with production volumes reaching 0.28 million units. These dentures provide superior stability and functionality, with success rates exceeding 95%. 3D printing enables precise implant alignment, improving surgical outcomes by 22%. The use of high-performance resins and hybrid materials enhances durability and aesthetic appeal. Rising demand for premium dental solutions is boosting this segment.

By Application

Dental laboratories dominate with a 54% share, producing over 1.02 million units annually. These facilities leverage high-capacity industrial 3D printers capable of producing 50–120 units per day. Automation reduces labor costs by 35% and increases efficiency by 40%. Laboratories also benefit from centralized production, ensuring consistent quality and scalability.

Dental clinics account for 31% share, with production volumes of 0.59 million units. Chairside 3D printing systems enable same-day denture fabrication, improving patient satisfaction by 48%. Clinics are increasingly adopting compact printers, reducing dependency on external labs.

Hospitals contribute 15% share, producing 0.28 million units annually. These facilities focus on complex cases, including implant-supported dentures. Integration with surgical workflows enhances treatment outcomes by 30%.

Top Players in Germany 3D Printed Dentures Market

- Straumann Group

- Dentsply Sirona

- Ivoclar Vivadent

- Formlabs

- 3D Systems Corporation

- EnvisionTEC (Desktop Metal)

- BEGO GmbH

- GC Corporation

- Kulzer GmbH

- VITA Zahnfabrik

- Shining 3D

- SprintRay

- Carbon Inc.

Top Two Companies

Straumann Group

- Market Share: ~18%

- Position: Market leader in premium implant-supported dentures

Straumann Group leads with strong R&D investments exceeding USD 250 million annually. The company focuses on high-precision implant-supported dentures with success rates above 96%. Its digital workflow solutions improve production efficiency by 40%, making it a dominant player.

Dentsply Sirona

- Market Share: ~15%

- Position: Leader in digital dentistry solutions

Dentsply Sirona offers comprehensive CAD/CAM systems and 3D printing solutions. The company produces over 0.25 million denture units annually and has a strong presence across Germany. Its integrated systems reduce production time by 50%.

Investment

Investment in the Germany 3D Printed Dentures market exceeded USD 520 million in 2025, with 38% allocated to equipment upgrades, 27% to material innovation, and 35% to digital software integration. Private equity investments accounted for 42%, while government funding contributed 18%. Dental laboratories received 54% of total investments due to their dominant role in production.

M&A activity has increased significantly, with over 12 major acquisitions between 2023 and 2025. Strategic collaborations between material manufacturers and dental technology firms are enhancing innovation. Partnerships between software developers and dental clinics are also increasing, improving workflow efficiency by 45%.

New Product

New product development accounts for 22% of total market activity, with over 65 new denture products launched between 2023 and 2025. Innovations focus on improving durability by 35% and reducing production time by 50%. Advanced biocompatible materials have increased patient satisfaction rates by 28%. Companies are also developing AI-powered design tools, improving customization accuracy by 30%.

Recent Development in Germany 3D Printed Dentures Market

- 2025: Straumann increased production capacity by 22%, producing over 0.32 million units annually through new 3D printing facilities in Germany.

- 2024: Dentsply Sirona launched a new digital denture system, improving workflow efficiency by 45% and reducing production time by 50%.

- 2023: Formlabs expanded its dental portfolio, increasing material production by 18% and capturing 12% additional market share.

Research Development in Germany 3D Printed Dentures Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, dental practitioners, and manufacturers, accounting for 60% of data validation. Secondary research involves analysis of industry reports, company filings, and government databases, contributing 40% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation and validation techniques are used to ensure reliability and consistency across all findings.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.