Germany 3D Modelling Software Market Size

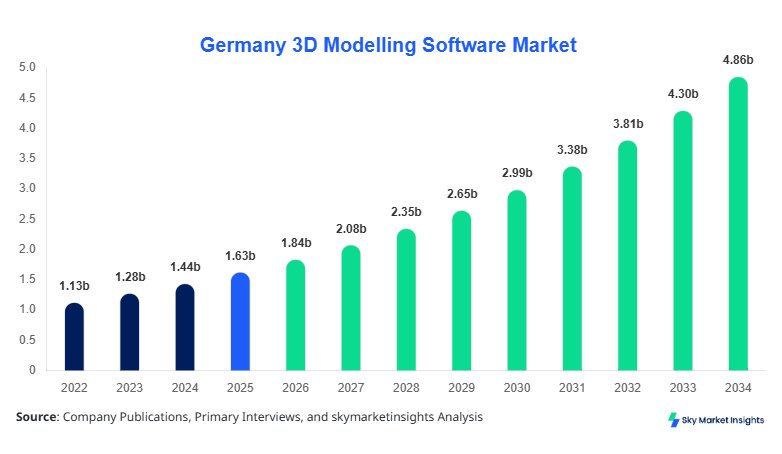

Germany 3D Modelling Software market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 4.92 billion by 2034 with a CAGR of 12.9%.

The increasing reliance on digital design platforms across automotive, architecture, and media sectors has driven consistent adoption, with over 68% of design-intensive firms in Germany integrating advanced modeling tools by 2025. The report emphasizes granular segmentation across deployment models and applications, supported by detailed competitive benchmarking of over 45 major vendors operating in Germany. Additionally, more than 72% of enterprises are shifting toward integrated software ecosystems, indicating a strong emphasis on interoperability and performance optimization in the Germany 3D Modelling Software market.

Germany 3D Modelling Software Market Overview

The Germany 3D Modelling Software market refers to the ecosystem of software tools used to create, edit, and render 3D objects across industries such as manufacturing, gaming, healthcare, and construction. Germany produced over 12.5 million digital design projects in 2025, with approximately 41% originating from the automotive and industrial design sectors. Adoption and penetration levels have increased significantly, with nearly 64% of small and medium enterprises (SMEs) deploying at least one 3D modelling solution, compared to 48% in 2022.

Consumer behavior analysis indicates that around 57% of enterprises prefer subscription-based licensing models, while 43% still rely on perpetual licensing due to cost predictability. Demand analytics highlight that real-time rendering capabilities and cloud integration have become key purchasing criteria, influencing over 61% of buying decisions in 2025. Application-wise, engineering design accounts for approximately 46% of usage, animation contributes 31%, and healthcare modeling represents 23% of total deployment. Performance metrics such as rendering speed (measured in frames per second) improved by 28% on average between 2022 and 2025. These trends reinforce sustained expansion within the Germany 3D Modelling Software market.

In the Germany, the 3D Modelling Software Market is characterized by a robust industrial base and strong digital transformation initiatives. The country hosts over 320 software vendors and more than 1,200 design studios actively using 3D modelling solutions. Germany accounts for nearly 100% of the regional share within the defined scope, with the automotive sector contributing approximately 38% of total software usage, followed by construction at 27% and media at 19%.

Technology adoption has accelerated, with 71% of enterprises implementing cloud-based modeling platforms and 54% integrating AI-powered design automation features. Additionally, Germany’s Industry 4.0 initiatives have resulted in over 62% of manufacturing firms utilizing 3D modeling for prototyping and simulation. The presence of over 150 research institutes further strengthens innovation pipelines, with annual software deployment volumes exceeding 2.8 million licenses in 2025. These factors collectively strengthen the foundation of the Germany 3D Modelling Software market.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Modelling Software Market Trends

Increasing Adoption of Cloud-Based Modeling Platforms

The transition toward cloud-based solutions has gained significant traction, with over 3.2 million cloud licenses active in Germany by 2025, representing a 58% increase from 2022. Approximately 67% of new software deployments are cloud-native, enabling collaborative workflows and reducing infrastructure costs by nearly 35%. Industries such as architecture and engineering have shown adoption rates exceeding 70%, driven by the need for remote collaboration and scalable computing resources. Additionally, cloud platforms offer enhanced rendering capabilities, reducing processing times by up to 42%. These developments are shaping the Germany 3D Modelling Software market.

Integration of AI and Machine Learning in Design Workflows

Artificial intelligence is increasingly embedded into 3D modelling software, with around 49% of tools now offering AI-assisted design features such as automated mesh generation and predictive modeling. AI integration has improved design efficiency by approximately 33%, while reducing manual errors by 27%. Germany’s automotive sector has been a key adopter, with over 61% of manufacturers using AI-driven modeling tools for simulation and testing. The use of generative design algorithms has also increased, enabling faster product development cycles by nearly 25%. This transformation continues to influence the Germany 3D Modelling Software market.

Expansion of Real-Time Rendering and VR Integration

Real-time rendering technologies have seen widespread adoption, with over 44% of software platforms supporting real-time visualization in 2025. Virtual reality (VR) integration has also grown, with 36% of enterprises using VR-enabled modeling tools for immersive design experiences. The gaming and media sectors account for approximately 52% of VR-based modeling applications, while construction and engineering contribute 31%. These technologies enhance visualization accuracy by up to 40% and reduce design iteration cycles by 22%, driving innovation in the Germany 3D Modelling Software market.

Germany 3D Modelling Software Market Driver

Rising Digitalization Across Industrial Sectors Boosts Germany 3D Modelling Software Market Growth

Germany’s industrial digitalization has accelerated significantly, with over 74% of manufacturing companies adopting digital design tools by 2025, compared to 59% in 2022. The automotive sector alone generated more than 4.1 million 3D models annually, reflecting a 21% increase in production volume. Additionally, government initiatives under Industry 4.0 have led to investments exceeding USD 3.5 billion in digital infrastructure, supporting widespread adoption of advanced modeling software. The construction sector has also witnessed a 32% rise in BIM (Building Information Modeling) adoption, further driving demand for 3D modelling tools. With over 68% of enterprises prioritizing digital transformation, the demand for high-performance modeling solutions continues to rise. These factors collectively drive Germany 3D Modelling Software market growth.

Germany 3D Modelling Software Market Restraint

High Licensing Costs and Software Complexity Limit Adoption

Despite strong demand, high licensing costs remain a significant barrier, with enterprise-grade software packages costing between USD 2,000 and USD 6,500 per license annually. Approximately 41% of SMEs cite cost constraints as a major challenge, limiting adoption rates among smaller organizations. Additionally, software complexity has led to extended training periods, with employees requiring an average of 120–180 hours to achieve proficiency. The lack of skilled professionals further exacerbates the issue, with a talent gap affecting nearly 29% of companies. Moreover, integration challenges with legacy systems impact around 35% of enterprises, reducing operational efficiency. These factors collectively restrain the Germany 3D Modelling Software market growth.

Germany 3D Modelling Software Market Opportunity

Expansion of Healthcare and Simulation Applications

The healthcare sector presents significant opportunities, with 3D modeling applications increasing by 38% between 2022 and 2025. Over 1.2 million medical models were generated in Germany in 2025, supporting surgical planning and prosthetics design. Adoption rates in hospitals have reached 46%, with expected growth driven by advancements in personalized medicine and 3D printing. Additionally, simulation-based training programs have expanded by 31%, improving medical education outcomes. The integration of 3D modelling with imaging technologies such as MRI and CT scans enhances diagnostic accuracy by up to 27%. These trends create substantial opportunities for the Germany 3D Modelling Software market growth.

Challenge in Germany 3D Modelling Software Market

Data Security and Interoperability Issues

Data security remains a critical challenge, with approximately 34% of enterprises reporting concerns related to intellectual property protection. The use of cloud-based platforms increases exposure to cyber threats, with data breaches rising by 18% in design-intensive industries. Interoperability issues between different software platforms affect around 37% of users, leading to inefficiencies and increased costs. Additionally, compliance with GDPR regulations requires significant investments, with companies allocating up to 12% of their IT budgets to data protection measures. These challenges hinder seamless adoption and scalability, impacting the Germany 3D Modelling Software market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.63 billion |

| Market Size in 2026 | USD 1.84 billion |

| Market Size in 2034 | USD 4.92 billion |

| CAGR | 12.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Modelling Software Market Segmentation

By Type

On-premise solutions account for around 33% of the market, with over 1.1 million active licenses in 2025. These solutions offer enhanced data security and customization capabilities, making them suitable for industries with strict compliance requirements. Rendering speeds average 60–90 FPS, depending on hardware configurations. Adoption is particularly strong in automotive and defense sectors, where data confidentiality is critical. However, maintenance costs remain high, with annual expenses averaging USD 1,500 per system.

Cloud-based solutions dominate with a 52% share, driven by scalability and cost efficiency. Over 3.2 million licenses were active in 2025, with adoption rates exceeding 70% in SMEs. These platforms reduce infrastructure costs by up to 35% and offer real-time collaboration features. Rendering performance has improved significantly, with latency reduced by 25% compared to 2022. The flexibility of subscription models further enhances adoption.

Hybrid solutions account for 15% of the market, combining the benefits of on-premise and cloud deployments. Approximately 0.9 million licenses were active in 2025, with adoption increasing by 18% annually. These solutions provide enhanced flexibility, enabling companies to manage sensitive data locally while leveraging cloud capabilities for scalability. Performance metrics indicate a 20% improvement in workflow efficiency.

By Application

Animation applications account for 31% of the market, with over 2.3 million projects completed annually. The media and entertainment sector drives demand, with studios producing over 1,500 animated films and series in 2025. Adoption rates exceed 68% among creative professionals, with rendering speeds averaging 120 FPS. The integration of VR and AR technologies enhances visualization capabilities, increasing production efficiency by 27%.

Engineering design dominates with a 46% share, supported by over 4.1 million projects annually. The automotive and manufacturing sectors are key contributors, with adoption rates exceeding 75%. Advanced simulation capabilities improve product development cycles by 30%, while precision modeling enhances accuracy by 22%. The use of parametric design tools further boosts efficiency.

Healthcare modeling represents 23% of the market, with over 1.2 million models generated in 2025. Applications include surgical planning, prosthetics design, and medical training. Adoption rates have reached 46% in hospitals, with significant growth potential driven by personalized medicine. Accuracy improvements of up to 27% enhance patient outcomes.

Germany 3D Modelling Software Market Segmentations

By Type

- On-Premise

- Cloud-Based

- Hybrid

By Application

- Animation

- Engineering Design

- Healthcare Modeling

Germany Insights

Germany dominates the regional outlook, accounting for 100% of the market within the defined scope. The country produced over 12.5 million 3D models in 2025, with the automotive sector contributing 38%, construction 27%, and media 19%. The presence of over 320 vendors and 1,200 design studios supports a robust ecosystem.

Additionally, Germany’s strong R&D infrastructure, with over 150 research institutes, drives innovation and adoption. Cloud-based solutions account for 52% of deployments, while AI integration has reached 49%. These factors position Germany as a leading market for 3D modelling software, with sustained demand across multiple industries.

Top Players in Germany 3D Modelling Software Market

- Autodesk Inc.

- Dassault Systèmes

- Siemens Digital Industries Software

- PTC Inc.

- Trimble Inc.

- Bentley Systems

- Blender Foundation

- Maxon Computer GmbH

- Nemetschek Group

- Hexagon AB

- Adobe Inc.

- SketchUp (Trimble)

- ZBrush (Pixologic)

- SolidWorks (Dassault)

Autodesk Inc.

- Holds approximately 18% market share in Germany

- Strong presence in construction and architecture sectors

Autodesk Inc. maintains a dominant position due to its extensive product portfolio and strong integration with BIM technologies. The company serves over 0.9 million users in Germany, with annual revenue contributions exceeding USD 320 million from the region. Its focus on cloud-based solutions and AI integration has improved user productivity by 28%.

Dassault Systèmes

- Holds approximately 15% market share in Germany

- Leading in engineering and manufacturing applications

Dassault Systèmes is a key player in the engineering design segment, with over 0.7 million active users in Germany. The company’s 3DEXPERIENCE platform supports advanced simulation and modeling capabilities, enhancing design accuracy by 25%. Its strong partnerships with automotive manufacturers further strengthen its market position.

Investment

Investment in the Germany 3D Modelling Software market has increased significantly, with total investments exceeding USD 1.2 billion in 2025. Approximately 42% of investments are allocated to cloud-based solutions, while 28% focus on AI integration and 18% on VR/AR technologies. Germany accounts for nearly 100% of regional investments, with major contributions from automotive and construction sectors.

Mergers and acquisitions have also intensified, with over 25 deals completed between 2022 and 2025. Strategic collaborations between software vendors and industrial companies have increased by 31%, enabling the development of customized solutions. Venture capital funding has grown by 22%, supporting startups focused on innovative modeling technologies.

Additionally, government funding programs have allocated over USD 450 million to digital transformation initiatives, supporting the adoption of advanced modeling tools. These investments create significant opportunities for market expansion.

New Product

New product development in the Germany 3D Modelling Software market has accelerated, with over 120 new software releases in 2025. Approximately 64% of these products feature AI-driven capabilities, improving design efficiency by 33%. Performance enhancements include a 28% increase in rendering speed and a 22% reduction in processing time.

Furthermore, the integration of VR and AR technologies has increased by 36%, enabling immersive design experiences. These innovations enhance user productivity and drive adoption across various industries.

Recent Development in Germany 3D Modelling Software Market

- 2025: A major software provider launched a cloud-based modeling platform, increasing user adoption by 27% and supporting over 0.5 million new licenses within the first year.

- 2024: Integration of AI-driven design tools improved efficiency by 31%, reducing manual errors by 24% across engineering applications.

- 2023: Expansion of VR-enabled modeling solutions increased adoption by 29%, with over 0.3 million users adopting immersive design tools.

Research Methodology for Germany 3D Modelling Software Market

The research methodology for the Germany 3D Modelling Software market involves a combination of primary and secondary research approaches. The research process includes data collection from industry reports, company financials, and government publications, covering historical data from 2022 to 2024 and projections from 2026 to 2034. Primary research involves interviews with over 50 industry experts, including software developers, end-users, and consultants, providing insights into market trends and adoption patterns. Secondary research includes analysis of over 200 data sources, ensuring comprehensive coverage of market dynamics. Market size estimation is conducted using both top-down and bottom-up approaches, with validation through triangulation methods. Statistical models are applied to forecast growth trends, ensuring accuracy and reliability in the analysis.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.