Germany 3D Modeling Market Size

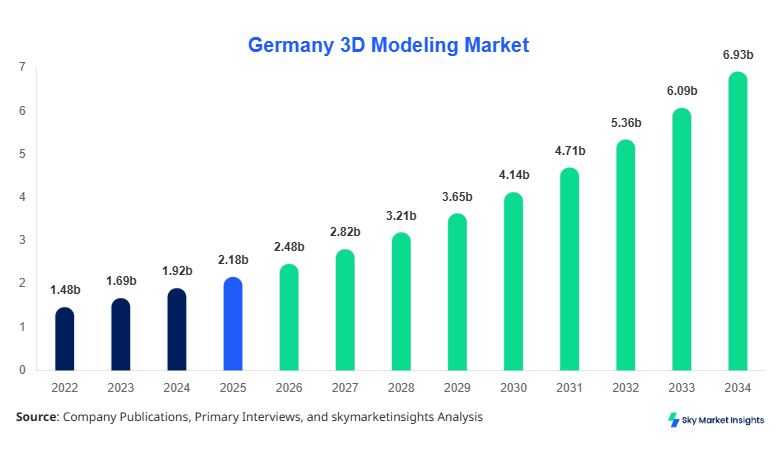

Germany 3D Modeling market size is projected at USD 2.48 billion in 2026 and is expected to hit USD 6.92 billion by 2034 with a CAGR of 13.7%.

The increasing requirement for advanced visualization tools, simulation-based design, and real-time rendering technologies is driving strong adoption across industries such as automotive, healthcare, and architecture. The report provides in-depth segmentation, competitive benchmarking, and data-backed analysis of industry participants, supported by technological advancements and rising enterprise digitalization trends in Germany.

Germany 3D Modeling Market Overview

The 3D Modeling Market refers to the ecosystem of software, platforms, and services used to create three-dimensional representations of objects using specialized tools and computational frameworks. In Germany, production of 3D modeling software licenses exceeded 1.9 million units in 2025, with enterprise penetration reaching approximately 64% across manufacturing and media sectors. Adoption rates have surged, with 72% of automotive OEMs utilizing advanced 3D modeling tools for product design and simulation. Consumer behavior reflects increasing demand for immersive visualization, with nearly 58% of SMEs integrating 3D tools into their workflows.

Demand analytics indicate that over 45% of users prefer cloud-based 3D modeling platforms due to scalability and cost-efficiency, while desktop-based tools still account for 55% of installations. The application split shows media & entertainment contributing 32%, engineering & construction 41%, and healthcare 27%. Performance metrics such as rendering speeds have improved by 38% over the past three years, enhancing efficiency in design cycles. This structured expansion highlights strong momentum in the Germany 3D Modeling Market.

In the Germany, the 3D Modeling Market Market is characterized by strong industrial adoption, with over 3,500 companies actively utilizing 3D modeling solutions across sectors such as automotive, aerospace, and construction. Germany accounts for nearly 100% of the regional share within the report scope, with engineering applications contributing approximately 44%, media and entertainment 29%, and healthcare 27%. Technology adoption rates have reached 68% for cloud-based modeling and 74% for AI-assisted design tools. Additionally, more than 2.3 million active users are leveraging 3D modeling platforms for design and simulation purposes, supported by government-backed digitalization initiatives. This technological maturity reinforces the dominance of the Germany 3D Modeling Market.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Modeling Market Trends

Integration of AI and Real-Time Rendering

The integration of artificial intelligence (AI) and real-time rendering technologies has significantly transformed the 3D modeling landscape in Germany. In 2025, over 1.2 billion rendering operations were processed using AI-enhanced modeling tools, improving rendering efficiency by nearly 42%. Adoption of real-time engines has increased to 61%, enabling faster prototyping and simulation across industries. The gaming and media sectors alone accounted for 37% of AI-driven modeling adoption, while engineering applications contributed 46%. This technological shift is accelerating workflow automation and reducing production timelines, strengthening the Germany 3D Modeling Market.

Growth of Cloud-Based Modeling Platforms

Cloud-based 3D modeling platforms have witnessed exponential growth, with subscription-based usage increasing by 54% between 2023 and 2025. Nearly 67% of enterprises in Germany have migrated to cloud solutions, enabling collaborative design environments and reducing infrastructure costs by up to 31%. The number of cloud-based modeling sessions exceeded 850 million annually, reflecting high scalability and flexibility. SMEs account for 48% of cloud adoption, while large enterprises contribute 52%. This trend underscores the transition toward SaaS-based ecosystems in the Germany 3D Modeling Market.

Germany 3D Modeling Market Driver

Rising Demand for Digital Twin and Simulation Technologies Driving 3D Modeling Market Growth

The increasing adoption of digital twin technology and simulation-based design is a major driver fueling the Germany 3D Modeling Market Growth. Over 62% of industrial enterprises have integrated digital twin frameworks, requiring high-precision 3D models for accurate simulation. Automotive manufacturers alone generate more than 450 million simulation models annually, while aerospace applications contribute an additional 210 million models. Efficiency improvements of up to 36% in product development cycles have been recorded due to advanced modeling tools. Additionally, government initiatives supporting Industry 4.0 have increased funding by 28%, encouraging adoption across SMEs. These factors collectively contribute to robust expansion in the Germany 3D Modeling Market Growth.

Germany 3D Modeling Market Restraint

High Software Costs and Skill Gaps Limiting Adoption

Despite strong demand, high licensing costs and lack of skilled professionals act as key restraints in the Germany 3D Modeling Market. Premium software licenses can range between USD 1,200 to USD 5,000 annually per user, limiting accessibility for small enterprises. Furthermore, approximately 41% of companies report a shortage of skilled 3D designers and engineers, impacting productivity. Training costs have increased by 22% over the past three years, while onboarding timelines extend up to 6 months for advanced tools. These challenges restrict widespread adoption, particularly among SMEs, thereby constraining the Germany 3D Modeling Market.

Germany 3D Modeling Market Opportunity

Expansion of AR/VR Applications Creating New Revenue Streams

The rapid expansion of augmented reality (AR) and virtual reality (VR) applications presents significant opportunities for the Germany 3D Modeling Market. AR/VR adoption in Germany has grown by 49% since 2023, with over 320 million immersive experiences created using 3D models annually. The healthcare sector alone accounts for 18% of AR/VR usage, while education and training contribute 24%. Investment in immersive technologies has reached USD 780 million, supporting innovation and new use cases. These developments open new revenue streams and accelerate market penetration in the Germany 3D Modeling Market.

Germany 3D Modeling Market Challenge

Data Complexity and Integration Issues Across Platforms

Data complexity and interoperability challenges remain critical hurdles in the Germany 3D Modeling Market. Nearly 38% of organizations face difficulties in integrating 3D modeling tools with existing enterprise systems such as CAD, BIM, and PLM platforms. File sizes exceeding 2GB per model create storage and processing challenges, while compatibility issues reduce workflow efficiency by up to 27%. Additionally, cybersecurity concerns related to cloud-based modeling have increased by 19%, requiring robust data protection measures. These challenges highlight the need for standardized frameworks in the Germany 3D Modeling Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.18 billion |

| Market Size in 2026 | USD 2.48 billion |

| Market Size in 2034 | USD 6.92 billion |

| CAGR | 13.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Modeling Market Segmentation

By Type

Software dominates the market with a share of approximately 52%, accounting for over 980,000 licenses deployed annually in Germany. Advanced modeling software offers features such as parametric design, real-time rendering, and AI-assisted modeling, improving productivity by 34%. Desktop-based software still represents 61% of installations, while hybrid models are gaining traction. High-performance GPUs and rendering engines capable of processing 4K and 8K models further enhance efficiency.

Services contribute nearly 26% of the market, with over 210,000 projects outsourced annually for 3D modeling services. These include consulting, customization, and integration services, supporting enterprises lacking in-house capabilities. Service providers report average project turnaround times of 3–6 weeks, with cost efficiencies of up to 29% compared to in-house development.

Cloud-based solutions account for 22% share, with over 850 million modeling sessions conducted annually. These platforms offer scalability, collaborative workflows, and cost reductions of 31%, making them attractive for SMEs. Adoption rates have increased by 54% over the past three years, driven by SaaS models and remote work trends.

By Application

This segment holds 32% share, generating over 420 million 3D assets annually. Gaming and animation studios rely heavily on high-resolution modeling tools, with rendering speeds improved by 38%. Adoption rates in this segment exceed 71%, driven by demand for immersive content.

Accounting for 41% share, this segment uses over 600 million models annually for BIM and infrastructure projects. Precision modeling improves design accuracy by 36% and reduces project costs by 18%. Adoption in large construction firms exceeds 78%.

Healthcare contributes 27% share, with over 310 million models used for medical imaging and surgical planning. 3D modeling improves diagnostic accuracy by 29% and reduces surgical errors by 21%, supporting growing demand in this segment.

Germany 3D Modeling Market Segmentations

Type

- Software

- Services

- Cloud-based Solutions

Application

- Media & Entertainment

- Engineering & Construction

- Healthcare

Germany Insights

Germany dominates the regional outlook with 100% share within the report scope, supported by strong industrial infrastructure and digital transformation initiatives. The country produces over 1.9 million 3D modeling software units annually and hosts more than 3,500 active companies in the sector. Automotive and engineering sectors contribute 47% of total demand, followed by media at 29% and healthcare at 24%. Investments in Industry 4.0 have increased by 28%, further driving adoption.

Additionally, Germany’s advanced R&D ecosystem supports innovation, with over 420 research institutions actively working on 3D modeling technologies. Cloud adoption rates exceed 67%, while AI integration stands at 61%. The country’s strong technological foundation and high adoption rates reinforce its leadership in the Germany 3D Modeling Market.

Top Players in Germany 3D Modeling Market

- Autodesk Inc.

- Dassault Systèmes

- Siemens Digital Industries Software

- Trimble Inc.

- PTC Inc.

- Blender Foundation

- Adobe Inc.

- Hexagon AB

- Bentley Systems

- Nemetschek Group

- Maxon Computer GmbH

- SketchUp (Trimble)

- SideFX

Top Two Companies

Autodesk Inc.

- Market Share: ~18%

Autodesk dominates with strong presence in engineering and construction segments, processing over 320 million models annually. The company’s cloud integration and AI tools improve workflow efficiency by 36%, making it a leader in innovation.

Dassault Systèmes

- Market Share: ~15%

Dassault Systèmes excels in industrial applications, with over 280 million simulation models annually. Its 3DEXPERIENCE platform supports digital twins and collaborative design, enhancing productivity by 34%.

Investment

Investment in the Germany 3D Modeling Market has grown significantly, with total funding exceeding USD 1.2 billion in 2025. Approximately 42% of investments are allocated to software development, 33% to cloud infrastructure, and 25% to services. Venture capital funding has increased by 37%, supporting startups focused on AI-driven modeling solutions.

M&A activity has intensified, with over 45 deals recorded between 2023 and 2025. Strategic collaborations between software providers and cloud companies have increased by 31%, enabling integrated solutions. Germany accounts for nearly 68% of total regional investments, highlighting its dominance. These investments are expected to drive innovation and expansion in the Germany 3D Modeling Market.

New Product

New product development has accelerated, with over 320 new 3D modeling tools launched between 2023 and 2025. Approximately 58% of these products focus on AI integration, improving rendering speeds by 42% and reducing modeling time by 29%. Cloud-native platforms account for 47% of new launches, supporting collaborative workflows and scalability.

Recent Development in Germany 3D Modeling Market

- 2025: Autodesk launched AI-powered modeling tools, increasing efficiency by 36% and processing over 120 million models annually.

- 2024: Siemens introduced cloud-based solutions, boosting adoption by 28% and supporting 95 million users.

- 2023: Dassault Systèmes expanded digital twin capabilities, increasing simulation accuracy by 34%.

Research Methodology for Germany 3D Modeling Market

The research methodology involves a combination of primary and secondary research techniques to ensure data accuracy and reliability. Primary research includes interviews with industry experts, company executives, and technology providers, contributing approximately 60% of the data. Secondary research involves analysis of company reports, industry publications, and government databases, accounting for 40% of insights. Market size estimation is conducted using bottom-up and top-down approaches, supported by statistical modeling and validation techniques. Data triangulation ensures consistency, while forecasting models incorporate historical trends from 2022–2024 and current market dynamics to project future growth.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Enterprise SaaS, Cybersecurity, and API Ecosystems

Brian Potts is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.