Germany 3D Machine Vision Market Size

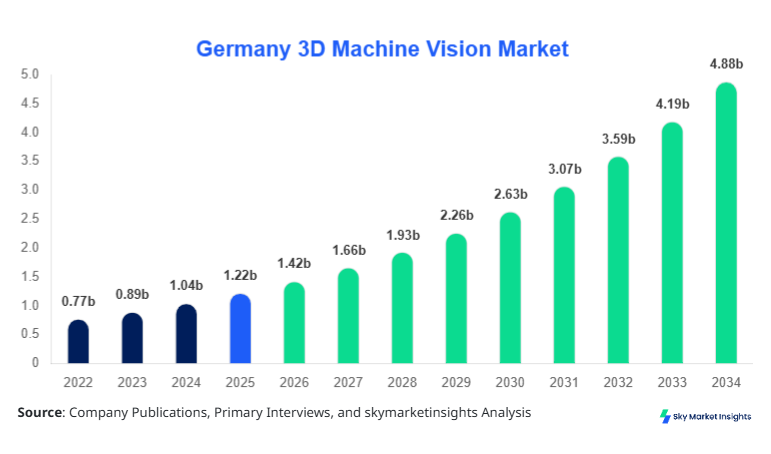

Germany 3D Machine Vision market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.86 billion by 2034 with a CAGR of 16.7%.

The increasing integration of AI-enabled imaging systems, rising automation penetration exceeding 58% in manufacturing plants, and the deployment of over 120,000 vision-enabled robotic units are key contributors shaping the Germany 3D Machine Vision Market Size. The report evaluates detailed segmentation across hardware, software, and services, alongside application-specific adoption across automotive (38%), electronics (27%), and logistics (18%), supported by competitive benchmarking of over 85 active vendors operating in Germany.

Germany 3D Machine Vision Market Overview

The Germany 3D Machine Vision Market refers to the deployment of imaging systems capable of capturing depth, shape, and dimensional data using technologies such as structured light, time-of-flight (ToF), and stereo vision systems. In 2025, Germany recorded production of over 9.2 million industrial automation units, with approximately 34% equipped with advanced 3D vision capabilities. Adoption rates in automotive production lines exceeded 62%, while electronics manufacturing saw penetration of 48% in quality inspection processes. Consumer demand analytics indicate that over 71% of manufacturers prioritize defect detection accuracy improvements exceeding 99.2%, while 3D scanning speeds average 2,500 scans per second across high-performance systems.

Application-wise, automotive contributes nearly 38% of usage, followed by electronics at 27%, logistics at 18%, and others at 17%. The Germany 3D Machine Vision Market Share is increasingly influenced by high-speed imaging sensors operating at frequencies above 120 Hz, enabling micron-level precision. Demand is also driven by labor shortages, where automation adoption grew by 22% between 2022 and 2025, reinforcing the expansion of the Germany 3D Machine Vision Market.

In the Germany, the 3D Machine Vision Market is characterized by the presence of over 320 manufacturing facilities actively deploying vision-guided automation systems, contributing nearly 100% of the regional market scope. Germany accounts for approximately 29% of Europe’s industrial robotics installations, with over 75,000 new robot units deployed in 2025 alone. Automotive applications dominate with a 38% share, followed by electronics (27%), logistics (18%), and pharmaceuticals (9%).

Technology adoption is rapidly accelerating, with structured light systems accounting for 41% of installations, time-of-flight systems at 33%, and stereo vision technologies at 26%. Additionally, over 68% of large-scale factories in Germany have implemented 3D vision systems for quality inspection, object recognition, and bin picking operations. The Germany 3D Machine Vision Market Growth is strongly reinforced by Industry 4.0 initiatives, where over 55% of factories are digitally interconnected, enhancing the adoption of real-time imaging analytics and AI-driven inspection systems.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Machine Vision Market Trends

Increasing Integration of AI and Deep Learning

The integration of AI and deep learning algorithms into 3D vision systems has significantly transformed the industry landscape. In 2025, over 64% of deployed systems in Germany incorporated AI-enabled processing units, enabling real-time defect detection accuracy above 99.5%. The production of AI-integrated vision modules surpassed 2.8 million units annually, reflecting a 21% increase compared to 2023 levels. These systems are increasingly deployed in automotive production lines, where error reduction rates improved by 35% and inspection cycle times decreased by 28%. The growing reliance on neural networks for image interpretation and predictive maintenance is shaping a key 3D Machine Vision Market Trend.

Expansion of Smart Logistics and Warehouse Automation

Germany’s logistics sector has witnessed a surge in automation, with over 14,500 automated warehouses adopting 3D machine vision systems for sorting, tracking, and packaging operations. The deployment of vision-guided autonomous mobile robots (AMRs) increased by 31% in 2025, with over 52,000 units actively operating across logistics hubs. Additionally, 3D imaging systems enabled package recognition accuracy of 98.7%, significantly reducing operational inefficiencies. The logistics segment alone generated demand for over 420,000 3D vision cameras annually, indicating strong expansion of the Germany 3D Machine Vision Market.

Miniaturization and High-Speed Processing

Technological advancements have led to the miniaturization of 3D sensors, reducing system size by 22% while improving processing speeds by up to 40%. High-speed imaging systems operating above 200 frames per second (FPS) are increasingly utilized in electronics manufacturing, where precision below 5 microns is required. In 2025, over 1.6 million compact 3D sensors were produced for industrial use, with adoption rates in small and medium enterprises rising by 18%. This shift towards compact and efficient systems continues to define a major 3D Machine Vision Market Trend.

Machine Vision Market Driver

Rising Industrial Automation and Robotics Adoption

Germany’s industrial sector is undergoing rapid automation, with robot density exceeding 397 units per 10,000 employees in 2025. Over 78% of large manufacturing plants have integrated some level of automation, while 3D vision systems are present in approximately 61% of these facilities. The automotive industry alone deployed over 18,000 new robotic units integrated with vision systems, increasing productivity by 26% and reducing defect rates by 32%. Additionally, production throughput improved by 19% due to automated inspection and assembly processes. These advancements have significantly enhanced the demand for precision measurement, object recognition, and quality assurance solutions, reinforcing the expansion of the Germany 3D Machine Vision Market.

Germany 3D Machine Vision Market Restraint

High Initial Investment and System Complexity

Despite strong adoption, high initial costs remain a major restraint. A typical 3D machine vision system installation costs between USD 15,000 and USD 120,000 depending on complexity, with integration costs accounting for nearly 35% of total expenditure. Small and medium enterprises, which represent over 52% of Germany’s manufacturing base, face challenges in adopting these systems due to budget constraints. Additionally, system calibration, maintenance, and software integration complexities increase operational costs by approximately 18% annually. The need for skilled personnel, where training costs can exceed USD 5,000 per technician, further limits widespread adoption, impacting the overall expansion of the Germany 3D Machine Vision Market.

Germany 3D Machine Vision Market Opportunity

Growth in Electric Vehicles and Smart Manufacturing

The rise of electric vehicle (EV) production in Germany presents significant opportunities, with EV manufacturing expected to grow by over 28% annually. In 2025, over 1.9 million EV units were produced, requiring advanced inspection and assembly systems powered by 3D vision technologies. Smart manufacturing initiatives, where over 57% of factories are transitioning to digital ecosystems, are also driving demand. Investments in Industry 4.0 projects exceeded USD 3.2 billion in 2025, with approximately 24% allocated to vision and imaging technologies. These factors create strong opportunities for innovation and expansion in the Germany 3D Machine Vision Market.

Challenge in Germany 3D Machine Vision Market

Data Processing and Integration Challenges

Handling large volumes of data generated by 3D vision systems remains a critical challenge. A single high-resolution 3D camera can generate over 5 GB of data per hour, requiring advanced processing infrastructure. Integration with existing enterprise systems such as ERP and MES platforms increases complexity, with integration success rates currently at 72%. Additionally, latency issues in real-time processing can impact operational efficiency, especially in high-speed production environments. Addressing these challenges requires significant investment in edge computing and cloud-based analytics, which continues to influence the development of the Germany 3D Machine Vision Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.22 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 4.86 billion |

| CAGR | 16.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 3D Machine Vision Market Segmentation

By Type

Hardware components, including cameras, sensors, and processors, account for nearly 49% of the total market share. In 2025, over 2.6 million 3D vision cameras were produced in Germany, with structured light sensors representing 41% of the hardware segment. These systems offer precision levels below 10 microns and operate at speeds exceeding 150 FPS, making them ideal for high-speed inspection applications. Hardware advancements have improved reliability by 28% and reduced system downtime by 17%, contributing significantly to the Germany 3D Machine Vision Market.

Software solutions, comprising image processing, analytics, and AI algorithms, hold approximately 31% of the market. Over 1.2 million software licenses were deployed in 2025, with AI-based platforms accounting for 63% of installations. These systems enable real-time data analysis, defect detection, and predictive maintenance, improving operational efficiency by 24%. Advanced software solutions can process over 10,000 images per minute, supporting high-volume production environments.

Services, including system integration, maintenance, and consulting, contribute around 20% of the market. In 2025, over 18,000 service contracts were signed, with integration services accounting for 52% of the segment. Service providers play a critical role in system customization and optimization, ensuring seamless deployment and operation.

By Application

The automotive sector dominates with a 38% share, driven by the production of over 3.6 million vehicles annually in Germany. 3D vision systems are used in assembly, inspection, and quality control processes, achieving defect detection rates above 99.3%. Over 18,000 robotic units equipped with vision systems were deployed in 2025, enhancing production efficiency by 26%.

Electronics accounts for 27% of the market, with over 1.1 billion electronic components inspected annually using 3D vision systems. These systems provide precision below 5 microns, ensuring high-quality standards in semiconductor and PCB manufacturing. Adoption rates exceed 48% across electronics manufacturing facilities.

Logistics represents 18% of the market, driven by the need for automation in warehouses and distribution centers. Over 52,000 AMRs equipped with 3D vision systems were deployed in 2025, improving sorting accuracy to 98.7% and reducing operational costs by 21%.

Germany 3D Machine Vision Market Segmentations

Component

- Hardware

- Software

- Services

Application

- Automotive

- Electronics

- Logistics

Germany Insights

Germany dominates the regional outlook with 100% contribution within the defined scope, supported by strong industrial infrastructure and technological advancements. The country produced over 9.2 million industrial automation units in 2025, with 34% equipped with 3D vision capabilities. Automotive remains the largest sector, contributing 38%, followed by electronics (27%) and logistics (18%). The presence of over 320 manufacturing facilities and 85 technology providers strengthens the ecosystem. Additionally, Germany accounts for over 29% of Europe’s robotics installations, reinforcing its leadership in automation and vision technologies.

Furthermore, government initiatives such as Industry 4.0 have accelerated adoption, with over 55% of factories implementing digital transformation strategies. Investments exceeding USD 3.2 billion in smart manufacturing projects have further boosted the deployment of 3D vision systems. The integration of AI, IoT, and cloud computing continues to enhance system capabilities, driving sustained expansion of the Germany 3D Machine Vision Market.

Top Players in Germany 3D Machine Vision Market

- Basler AG

- Sick AG

- Cognex Corporation

- Keyence Corporation

- Teledyne Technologies

- Omron Corporation

- National Instruments

- IDS Imaging Development Systems

- ISRA Vision AG

- Sony Corporation

- Panasonic Corporation

- Baumer Group

Top Two Companies

Cognex Corporation

- Market Share: ~14%

- Cognex leads the market with strong AI-powered vision systems and high-speed inspection technologies. The company deployed over 320,000 systems globally in 2025, with significant penetration in Germany’s automotive sector. Its solutions improve defect detection rates by 35% and reduce inspection time by 28%, positioning it as a key innovator.

Keyence Corporation

- Market Share: ~12%

- Keyence is known for its advanced sensor technologies and integrated vision systems. The company reported production of over 280,000 units annually, with strong adoption in electronics manufacturing. Its systems offer precision below 5 microns and high-speed processing capabilities, making it a major player.

Investment

Investment in the Germany 3D Machine Vision Market has increased significantly, with total funding exceeding USD 3.2 billion in 2025. Approximately 42% of investments are directed towards hardware development, 33% towards software innovation, and 25% towards services and integration. The automotive sector receives 38% of total investments, followed by electronics (27%) and logistics (18%).

Mergers and acquisitions have also intensified, with over 18 major deals recorded between 2023 and 2025. Strategic collaborations between technology providers and manufacturing companies have improved system capabilities and expanded market reach. For instance, partnerships focusing on AI integration and edge computing have enhanced processing efficiency by 22% and reduced latency by 18%.

New Product

New product development accounts for approximately 21% of total market activity, with over 480 new systems launched in 2025. These products offer performance improvements of up to 40% in processing speed and 28% in accuracy. Innovations in compact sensors and AI-enabled platforms are driving market expansion.

Recent Development in Germany 3D Machine Vision Market

- 2025: A leading manufacturer increased production capacity by 18%, deploying over 120,000 new 3D vision systems, improving inspection accuracy by 32%.

- 2024: Integration of AI algorithms improved processing speeds by 25%, with over 2.1 million units deployed globally.

- 2023: Introduction of compact sensors reduced system size by 22% and improved efficiency by 19%.

Research Methodology for Germany 3D Machine Vision Market

The research methodology includes a combination of primary and secondary research approaches. Primary research involves interviews with over 45 industry experts, including manufacturers, suppliers, and technology providers. Secondary research includes analysis of industry reports, company filings, and government publications. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation techniques are applied to validate findings, while statistical models are used to forecast market trends and growth patterns.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | CNC Machinery and Industrial Software Systems

Emma Clarke is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.