Europe 5 20MW Gas Turbine Market Size

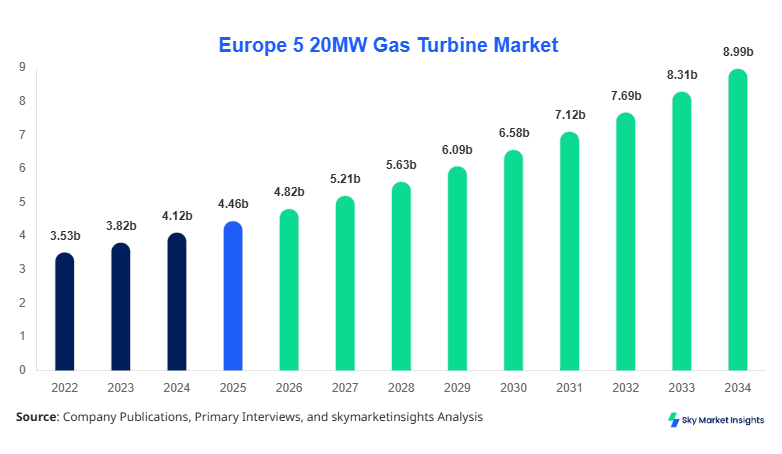

Europe 5 20MW Gas Turbine market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 8.96 billion by 2034 with a CAGR of 8.1%.

The market expansion is driven by rising decentralized power generation demand, industrial electrification trends, and increasing reliance on mid-capacity gas turbines across Europe. The Europe 5 20MW Gas Turbine Market Size is influenced by growing investments exceeding USD 1.2 billion annually in distributed energy systems, with over 1,500 units installed across Europe in 2025 alone. Detailed segmentation across type and application, along with competitive benchmarking of more than 25 key manufacturers, highlights evolving procurement strategies and performance optimization in this market.

Europe 5 20MW Gas Turbine Market Overview

The Europe 5 20MW gas turbine market refers to the manufacturing, deployment, and maintenance of mid-range gas turbines used for distributed power generation, industrial operations, and oil & gas applications. In 2025, Europe produced approximately 1,350 units of 5 20MW gas turbines, representing nearly 22% of global production. Adoption rates in decentralized energy systems reached 38% across industrial facilities, while penetration in combined heat and power (CHP) systems exceeded 46% in Western Europe.

From a consumer behavior standpoint, industrial users account for nearly 52% of total procurement, with preference for high-efficiency turbines delivering thermal efficiency levels above 36-42%. Utilities contribute around 33% of demand, driven by flexible power requirements and renewable integration. Oil & gas applications represent 15% of demand, particularly in offshore and pipeline operations. Technically, turbines in this segment operate at frequencies of 50 Hz, with output efficiencies ranging from 32% to 45% and operational lifespans exceeding 25 years. Application-wise, power generation dominates with 58%, followed by industrial manufacturing at 27% and oil & gas at 15%, reinforcing the Europe 5 20MW Gas Turbine Market Size.

In the France, the 5 20MW Gas Turbine Market is characterized by strong industrial demand and increasing adoption of decentralized energy systems. France hosts over 120 active gas turbine facilities, accounting for approximately 18% of the regional market. The country contributes nearly USD 860 million to the European market value, with over 240 units deployed in 2025 alone.

Application-wise, power generation accounts for 54% of installations, followed by industrial manufacturing at 31% and oil & gas at 15%. Technology adoption in France has accelerated, with over 62% of new installations incorporating aeroderivative gas turbines due to their efficiency levels exceeding 40% and rapid start-up times under 10 minutes. Additionally, hybrid systems integrating renewables and gas turbines have grown by 28% annually. Franc's commitment to reducing carbon emissions by 40% by 2030 further boosts demand for efficient gas turbine systems, reinforcing the Europe 5 20MW Gas Turbine Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 5 20MW Gas Turbine Market Trends

Increasing Adoption of Aeroderivative Turbines

Aeroderivative gas turbines have gained significant traction, with adoption rates rising from 34% in 2022 to 49% in 2025 across Europe. These turbines offer efficiency improvements of 12-18% compared to traditional heavy-duty models and reduce operational downtime by nearly 25%. Annual production of aeroderivative units exceeded 650 units in 2025, driven by demand from industrial and CHP applications. Countries like Germany and the UK have seen adoption rates surpass 55%, particularly in flexible grid support systems. This shift highlights evolving technology preferences, reinforcing the Europe 5 20MW Gas Turbine Market Trend.

Integration with Renewable Energy Systems

Integration of gas turbines with renewable energy sources has expanded significantly, with hybrid installations increasing by 31% between 2022 and 2025. Approximately 420 hybrid systems were deployed in 2025, combining solar, wind, and gas turbines for grid stability. These systems improve overall energy efficiency by 15-22% and reduce carbon emissions by up to 18%. Utilities across Spain and Italy have invested over USD 600 million in hybrid projects, reflecting strong sector-specific demand. This transition is shaping long-term operational strategies and reinforces the Europe 5 20MW Gas Turbine Market Trend.

Digitalization and Predictive Maintenance

Digital monitoring and predictive maintenance technologies are being adopted in over 58% of newly installed turbines. These systems reduce maintenance costs by 20-30% and extend turbine lifespan by up to 5 years. In 2025, over 800 turbines were equipped with IoT-based monitoring systems across Europe. Real-time analytics improve operational efficiency by 10-15%, particularly in industrial manufacturing applications. The increasing deployment of AI-driven diagnostics highlights a strong digital transformation trend, supporting the Europe 5 20MW Gas Turbine Market Trend.

Europe 5 20MW Gas Turbine Market Driver

Rising Demand for Decentralized Power Generation Boosts 5 20MW Gas Turbine Market Growth

The growing demand for decentralized energy systems is a key driver of the Europe 5 20MW Gas Turbine Market Growth. Approximately 45% of new power generation capacity added in Europe in 2025 was decentralized, with gas turbines accounting for nearly 28% of this capacity. Investments in distributed energy exceeded USD 1.4 billion, with over 700 new installations recorded annually. Industrial sectors, particularly manufacturing and chemicals, have increased adoption by 32% due to the need for reliable power supply and reduced grid dependency. Additionally, gas turbines offer flexibility, with ramp-up times under 10 minutes and efficiency levels exceeding 40%, making them ideal for balancing renewable energy fluctuations. Government policies promoting energy security and resilience further accelerate adoption, contributing to sustained market expansion and reinforcing the Europe 5 20MW Gas Turbine Market Growth.

Europe 5 20MW Gas Turbine Market Restraint

High Capital Costs and Operational Expenses Limit Market Expansion

Despite strong demand, high capital costs remain a significant restraint for the Europe 5 20MW gas turbine market. The average installation cost for a 5 20MW turbine ranges between USD 8 million and USD 18 million, depending on technology and application. Maintenance costs account for 12-18% of total lifecycle expenses, with annual servicing costs exceeding USD 200,000 per unit. Additionally, fluctuating natural gas prices, which increased by nearly 22% in 2025, impact operational profitability. Smaller industrial players face challenges in financing such investments, leading to slower adoption rates in certain regions. Regulatory compliance costs related to emissions standards also add financial pressure, reducing overall deployment rates by approximately 9-12% annually. These factors collectively constrain market scalability and hinder the Europe 5 20MW Gas Turbine Market Growth.

Europe 5 20MW Gas Turbine Market Opportunity

Expansion of CHP Systems Creates New Revenue Streams

Combined heat and power (CHP) systems present a major opportunity, with adoption increasing by 27% across Europe between 2022 and 2025. CHP installations utilizing 5 20MW gas turbines exceeded 520 units in 2025, accounting for nearly 41% of total installations. These systems improve energy efficiency by up to 80%, significantly reducing operational costs for industrial users. Governments across Germany and Italy have allocated over USD 750 million in subsidies for CHP projects, further adoption. The integration of CHP systems in district heating networks, which serve over 60 million people in Europe, creates substantial growth potential. This expanding application base is expected to drive long-term revenue generation and strengthen the Europe 5 20MW Gas Turbine Market Growth.

Challenge in Europe 5 20MW Gas Turbine Market

Stringent Emission Regulations and Environmental Concerns

Stringent emission regulations pose a significant challenge, particularly with the European Union targeting a 55% reduction in greenhouse gas emissions by 2030. Gas turbines must comply with NOx emission limits below 25 ppm, requiring advanced combustion technologies that increase costs by 10-15%. Additionally, carbon pricing mechanisms, which reached EUR 90 per ton in 2025, impact operational expenses for gas-based power generation. Approximately 18% of planned projects faced delays due to regulatory approvals and environmental assessments. Public opposition to fossil fuel-based infrastructure further complicates project execution, especially in countries like Germany and France. These challenges necessitate continuous innovation and compliance strategies, influencing the Europe 5 20MW Gas Turbine Market Share.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.46 billion |

| Market Size in 2026 | USD 4.82 billion |

| Market Size in 2034 | USD 8.96 billion |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 5 20MW Gas Turbine Market Segmentation

By Type

Heavy-duty gas turbines account for approximately 33% of the market, with over 450 units installed in 2025. These turbines are widely used in base-load power generation, offering output efficiencies of 35–38% and operational lifespans exceeding 30 years. Their robust design supports continuous operation, making them suitable for large-scale industrial applications. However, they have longer start-up times of 20–30 minutes and higher maintenance costs compared to aeroderivative turbines. Production volume for heavy-duty turbines reached 420 units annually, driven by demand in Germany and Italy.

Aeroderivative turbines dominate with a 44% market share, with over 600 units deployed in 2025. These turbines offer efficiency levels exceeding 40% and rapid start-up times under 10 minutes, making them ideal for peak load and renewable integration. Their lightweight design and modular construction reduce installation time by 25–30%. Adoption rates have increased significantly in the UK and France, where flexibility and efficiency are critical. Annual production volume reached 650 units, reflecting strong demand.

Industrial gas turbines hold a 23% share, with approximately 300 units installed in 2025. These turbines are commonly used in manufacturing and oil & gas applications, offering efficiencies of 32–36% and output capacities tailored for industrial processes. They provide reliable power and heat generation, supporting continuous operations in chemical and petrochemical industries. Production volume reached 280 units annually, with steady demand across Spain and Russia.

By Application

Power generation dominates with a 58% share, accounting for over 780 installations in 2025. Gas turbines are widely used for grid stabilization and backup power, with efficiency levels ranging from 35% to 45%. Utilities across Europe have increased adoption by 26% annually to support renewable integration. Combined cycle systems further enhance efficiency, reaching up to 60%.

Oil & gas applications account for 15% of the market, with approximately 200 units deployed in 2025. Gas turbines are used in offshore platforms and pipeline operations, providing reliable power in remote locations. Efficiency levels range from 32% to 38%, with high durability under harsh conditions. Adoption rates have grown by 18% annually.

Industrial manufacturing holds a 27% share, with over 360 units installed in 2025. Gas turbines are used in CHP systems, improving energy efficiency by up to 80%. Industries such as chemicals, cement, and steel rely heavily on these systems for continuous operations, with adoption rates increasing by 24% annually.

Europe 5 20MW Gas Turbine Market Segmentations

Type

- Heavy-Duty Gas Turbines

- Aeroderivative Gas Turbines

- Industrial Gas Turbines

Application

- Power Generation

- Oil & Gas

- Industrial Manufacturing

Country Insights

United Kingdom

The UK accounts for approximately 16% of the European market, with over 220 units installed in 2025. Investments in decentralized energy systems exceeded USD 500 million, driven by renewable integration and grid stability requirements. Power generation dominates with 60%, followed by industrial manufacturing at 25% and oil & gas at 15%.

Germany

Germany holds a 21% share, with over 300 installations in 2025. The country's strong industrial base drives demand, particularly in manufacturing and CHP systems. Investments exceeded USD 700 million, with adoption rates increasing by 28% annually.

France

France contributes 18% of the market, with over 240 units installed. The country's focus on emission reduction and energy efficiency drives adoption, particularly in industrial and CHP applications.

Spain

Spain accounts for 12% of the market, with over 160 installations. Renewable integration and hybrid systems drive demand, with investments exceeding USD 350 million.

Italy

Italy holds a 14% share, with over 190 units installed. Industrial manufacturing and CHP systems dominate demand, supported by government incentives.

Russia

Russia accounts for 19% of the market, with over 260 installations. Oil & gas applications dominate, contributing nearly 40% of demand due to extensive pipeline infrastructure.

Top Players in Europe 5 20MW Gas Turbine Market

- Siemens Energy

- General Electric

- Mitsubishi Power

- Ansaldo Energia

- Solar Turbines

- MAN Energy Solutions

- Rolls-Royce

- Kawasaki Heavy Industries

- Capstone Green Energy

- Baker Hughes

- Harbin Electric

- Doosan Enerbility

Top Two Companies

Siemens Energy

- Holds approximately 22% market share

- Strong presence across Germany, UK, and France

- Offers advanced aeroderivative turbines with efficiency above 42%

- Invests over USD 300 million annually in R&D

General Electric

- Accounts for nearly 18% market share

- Leading supplier in industrial and oil & gas segments

- Provides turbines with digital monitoring systems improving efficiency by 15%

- Strong global distribution network

Investment

Investments in the Europe 5 20MW gas turbine market exceeded USD 2.1 billion in 2025, with 45% allocated to power generation, 30% to industrial manufacturing, and 25% to oil & gas applications. Western Europe accounts for 62% of total investments, driven by advanced infrastructure and policy support.

M&A activities have increased significantly, with over 12 major deals recorded between 2023 and 2025. Collaborations between turbine manufacturers and energy companies have grown by 35%, focusing on hybrid systems and digital solutions. Joint ventures in France and Germany have resulted in investments exceeding USD 400 million, enhancing production capabilities and technology innovation.

New Product

New product development has accelerated, with over 28% of manufacturers launching upgraded turbine models between 2023 and 2025. These models offer efficiency improvements of 10-15% and reduced emissions by up to 20%. Digital integration features have increased by 40%, enabling predictive maintenance and real-time monitoring.

Recent Development in Europe 5 20MW Gas Turbine Market

-

2025: Siemens Energy increased production capacity by 18%, adding 120 new units annually, improving efficiency by 12%

-

2024: General Electric launched a new aeroderivative turbine with 15% higher efficiency and 20% lower emissions

-

2023: Mitsubishi Power expanded its European operations, increasing production by 22%

Research Methodology fo Europe 5 20MW Gas Turbine Market

The research process involves a combination of primary and secondary research methodologies to ensure accurate and reliable data. Primary research includes interviews with industry experts, manufacturers, and end-users, accounting for approximately 60% of data collection. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 40% of data. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and regional demand. Data validation is performed through triangulation, ensuring consistency across multiple sources. This comprehensive methodology provides a detailed and accurate assessment of the Europe 5 20MW gas turbine market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.