Europe 4K Ultra HD Television Market Size

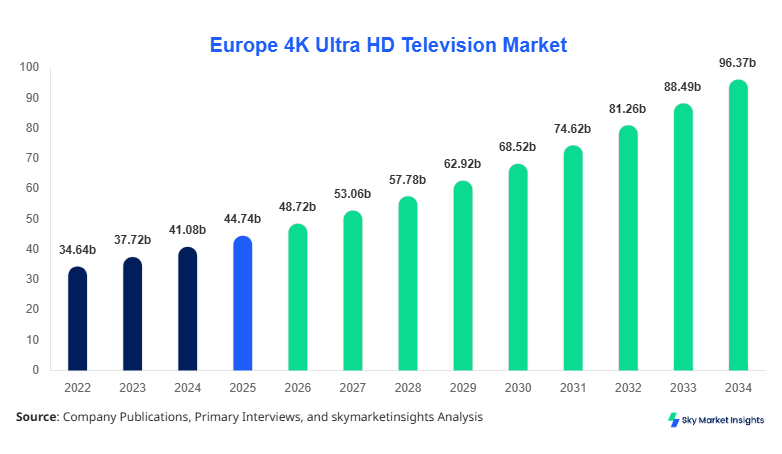

Europe 4K Ultra HD Television market size is projected at USD 48.72 billion in 2026 and is expected to hit USD 96.85 billion by 2034 with a CAGR of 8.9%.

The Europe 4K Ultra HD Television market is witnessing rapid expansion driven by increasing household penetration rates exceeding 72%, alongside rising annual shipments surpassing 38 million units in 2025. The report emphasizes the need for granular data segmentation across screen technologies, price tiers, and distribution channels, while also analyzing competitive benchmarking among leading OEMs holding over 65% combined market share. Growing demand for advanced display resolution and smart connectivity further supports Europe 4K Ultra HD Television market size expansion.

Europe 4K Ultra HD Television Market Overview

The Europe 4K Ultra HD Television market refers to the production, distribution, and consumption of televisions offering 3840 Ã 2160 pixel resolution, delivering 4x higher clarity compared to Full HD displays. In 2025, Europe produced over 41 million 4K Ultra HD units, with imports accounting for an additional 18 million units, reflecting strong supply chain integration across Germany, the UK, and Eastern Europe. Adoption rates have reached approximately 68% of total TV households, with penetration expected to cross 82% by 2030, driven by falling average selling prices from USD 780 in 2022 to USD 610 in 2025.

Consumer behavior indicates that nearly 64% of buyers prioritize screen size above 55 inches, while 58% prefer smart TV functionality with streaming integration. Demand analytics show that OTT consumption contributes to over 72% of usage hours, and gaming applications account for 18% of high-refresh-rate demand. LED-based TVs contribute around 55% of the market, while OLED and QLED together account for 45%. Application usage is split across residential (85%), commercial (10%), and hospitality (5%) sectors. Performance metrics such as refresh rates exceeding 120 Hz and HDR10+ support in over 60% of devices further enhance consumer appeal, reinforcing Europe 4K Ultra HD Television market share expansion.

In the United Kingdom, the 4K Ultra HD Television Market accounts for nearly 28% of the total Europe market, with over 11 million units sold annually across more than 150 active electronics retailers and 35 major manufacturing and assembly facilities. Residential applications dominate with 82% usage, followed by commercial displays at 12% and hospitality at 6%. Technology adoption is high, with over 74% of new purchases featuring smart TV integration and 5G-enabled streaming compatibility. OLED adoption in the UK stands at 32%, while QLED penetration has reached 26%, indicating rapid premiumization. Average screen sizes have increased from 48 inches in 2022 to 56 inches in 2025, supported by declining panel costs. These dynamics strongly contribute to Europe 4K Ultra HD Television market share.

Europe 4K Ultra HD Television Market Trends

Shift Toward Premium Display Technologies

The Europe 4K Ultra HD Television market is experiencing a significant shift toward OLED and QLED technologies, with production volumes of OLED TVs reaching 12.5 million units in 2025, up from 8.3 million units in 2022, reflecting a growth rate of over 50%. QLED shipments have similarly increased by 38%, crossing 10 million units annually. Approximately 46% of consumers now prefer high dynamic range (HDR) compatibility, while 35% demand Dolby Vision support. Manufacturers are investing heavily in micro-LED innovation, which is projected to capture 8% of premium segment share by 2030. The integration of AI-powered upscaling technology is now present in over 62% of new models, enhancing picture quality and user experience, reinforcing Europe 4K Ultra HD Television market trend.

Increasing Smart Connectivity and Streaming Integration

Another major trend is the integration of advanced smart connectivity features, with over 88% of 4K TVs sold in 2025 featuring built-in streaming apps such as Netflix, Amazon Prime, and Disney+. Internet-enabled televisions account for over 91% of shipments, compared to 76% in 2022. Voice assistant integration has grown significantly, with 57% of units supporting Alexa or Google Assistant. The rise of gaming consoles and cloud gaming has increased demand for HDMI 2.1 ports and refresh rates above 120 Hz, now present in 48% of models. Additionally, average viewing hours for streaming content have risen to 5.2 hours per day per household. These advancements continue to shape Europe 4K Ultra HD Television market trend.

Europe 4K Ultra HD Television Market Driver

Rising Consumer Demand for High-Resolution Entertainment

The surge in demand for immersive viewing experiences is a primary driver, with over 78% of European households consuming HD or UHD content daily. Streaming platforms have increased their 4K content libraries by over 65% between 2022 and 2025, supporting device upgrades. Annual shipments of 4K TVs have grown from 29 million units in 2022 to 38 million units in 2025, representing a 31% increase. Additionally, gaming consoles capable of 4K output have penetrated 42% of households, further boosting demand. Falling prices, with entry-level 4K TVs now priced below USD 400, have expanded accessibility across mid-income segments. These factors collectively accelerate Europe 4K Ultra HD Television market growth.

Europe 4K Ultra HD Television Market Restraint

High Cost of Premium Technologies and Supply Chain Volatility

Despite growth, the market faces restraints due to high costs associated with OLED and micro-LED technologies, where average prices exceed USD 1,200, limiting adoption to higher-income consumers representing only 28% of households. Supply chain disruptions have caused panel shortages, leading to a 12% increase in production costs in 2024. Additionally, energy consumption regulations in Europe have increased compliance costs by 8%, affecting manufacturer margins. Logistics challenges have also increased lead times by 15%, impacting inventory management. These factors collectively restrain Europe 4K Ultra HD Television market growth.

Europe 4K Ultra HD Television Market Opportunity

Expansion of Smart Home Ecosystems and IoT Integration

The integration of 4K TVs into smart home ecosystems presents a significant opportunity, with over 52% of European households expected to adopt IoT-enabled devices by 2030. Smart TVs are increasingly acting as central control hubs, with 48% of users utilizing them for home automation functions. Investment in AI-based content recommendations has increased by 34%, enhancing user engagement. Emerging markets within Eastern Europe are witnessing adoption growth rates above 12% annually, compared to the regional average of 8.9%. These opportunities support long-term Europe 4K Ultra HD Television market growth.

Challenge in Europe 4K Ultra HD Television Market

Intense Market Competition and Price Erosion

The market faces challenges due to intense competition among global brands, resulting in price erosion of nearly 9% annually across mid-range models. Over 25 major manufacturers compete for market share, leading to aggressive discounting strategies. Private label brands have gained 14% share, intensifying competition. Additionally, rapid technological advancements shorten product life cycles to less than 3 years, increasing R&D costs by 18%. Consumer preference for frequent upgrades also pressures manufacturers to innovate continuously. These challenges impact profitability within the Europe 4K Ultra HD Television market growth.

Europe 4K Ultra HD Television Market Segmentation

By Type

LED televisions dominate the Europe 4K Ultra HD Television market with over 21 million units produced annually, accounting for 55% of total shipments. These TVs offer brightness levels exceeding 400 nits and energy efficiency improvements of 18% compared to older LCD models. Adoption is highest among budget-conscious consumers, representing 62% of entry-level purchases. Average prices range between USD 350 and USD 650, making them accessible to a broader demographic. Technological advancements such as edge-lit and full-array backlighting enhance contrast ratios by up to 30%. LED TVs are widely used in residential settings, accounting for 78% of installations, supporting Europe 4K Ultra HD Television market share.

OLED televisions account for approximately 25% of the market, with production volumes reaching 9.5 million units in 2025. These TVs offer superior contrast ratios exceeding 1,000,000:1 and faster response times below 1 ms, making them ideal for gaming and cinematic experiences. Adoption rates have increased by 22% annually due to falling prices and improved panel durability. OLED TVs are predominantly used in premium households, representing 35% of high-income consumer purchases. Their energy efficiency has improved by 12%, and lifespan enhancements have increased panel longevity to over 100,000 hours, contributing to Europe 4K Ultra HD Television market share.

QLED televisions hold a 20% share, with annual shipments surpassing 7.5 million units. These TVs offer brightness levels exceeding 1,000 nits, making them suitable for well-lit environments. Adoption is growing at a rate of 15% annually, driven by enhanced color accuracy and quantum dot technology. QLED TVs are widely used in both residential and commercial settings, accounting for 28% of installations in offices and retail spaces. Their durability and lower burn-in risk compared to OLED make them attractive to commercial users, supporting Europe 4K Ultra HD Television market share.

By Application

This segment accounts for 22% of the market, with approximately 8 million units sold annually. These TVs are popular among small households and secondary room installations, with adoption rates of 34% in urban apartments. Average prices range from USD 300 to USD 500, making them affordable for entry-level consumers. Despite lower growth rates of 4.5%, this segment remains stable due to consistent demand in budget categories.

The 50-65 inches segment dominates with 48% share, driven by consumer preference for immersive viewing experiences. Annual shipments exceed 18 million units, with adoption rates surpassing 60% among new buyers. These TVs offer advanced features such as HDR10+ and refresh rates above 120 Hz, making them suitable for gaming and streaming. Average prices range between USD 600 and USD 1,000, supporting strong growth.

This segment holds 30% share, with shipments exceeding 11 million units annually. Growth rates exceed 12%, driven by increasing demand for home theater experiences. These TVs offer premium features such as 8K upscaling and AI-based picture enhancement, with prices ranging from USD 1,200 to USD 3,500. Adoption is highest among high-income households, representing 40% of purchases.

| Screen Type | Screen Size |

|---|---|

|

|

Country Insights

United Kingdom

The UK accounts for 28% of the Europe 4K Ultra HD Television market, with annual sales exceeding 11 million units. OLED adoption stands at 32%, while QLED accounts for 26%. Residential usage dominates at 82%, supported by high streaming penetration rates of 88%. Commercial applications contribute 12%, particularly in retail and corporate sectors.

Germany

Germany holds 22% share, with production volumes exceeding 9 million units annually. LED TVs dominate with 58% share, while OLED adoption is growing at 18% annually. Industrial and commercial applications account for 15% of usage, driven by digital signage demand.

France

France contributes 16% share, with over 6.5 million units sold annually. Smart TV penetration exceeds 85%, and streaming consumption averages 4.8 hours per day. OLED adoption has reached 27%, reflecting premiumization trends.

Spain

Spain accounts for 12% share, with 4.5 million units sold annually. LED TVs dominate with 62% share, while QLED adoption is increasing at 14% annually. Residential usage accounts for 88%.

Italy

Italy holds 11% share, with 4 million units sold annually. Smart TV penetration exceeds 83%, and OLED adoption stands at 24%. Hospitality applications contribute 8% of demand.

Russia

Russia accounts for 11% share, with 4.2 million units sold annually. LED TVs dominate with 65% share, while smart TV adoption is growing at 16% annually. Commercial usage accounts for 10%.

Top Layers in Europe 4K Ultra HD Television Market

- Samsung Electronics

- LG Electronics

- Sony Corporation

- Panasonic Corporation

- Philips

- Hisense

- TCL Corporation

- Sharp Corporation

- Vizio Inc.

- Skyworth Group

- Changhong

- Grundig

- Vestel

- Haier

Samsung Electronics

- Holds approximately 28% market share in Europe

- Strong presence in QLED segment with over 60% share

Samsung leads with advanced QLED technology and annual shipments exceeding 10 million units in Europe. The company invests over 6% of revenue in R&D and has expanded its AI-powered TV portfolio by 35%. Its distribution network spans over 40 countries, ensuring strong market penetration.

LG Electronics

- Holds approximately 22% market share

- Dominates OLED segment with over 65% share

LG is a leader in OLED technology, with annual shipments exceeding 8 million units. The company focuses on premium innovation, with OLED TV prices decreasing by 18% over the past three years. Its strong brand presence and technological leadership support its market position.

Investment

Investment in the Europe 4K Ultra HD Television market has increased by 26% between 2022 and 2025, with over USD 8.5 billion allocated to R&D and manufacturing. Approximately 42% of investments are directed toward OLED and micro-LED technologies, while 35% focus on smart TV software development. Regional investment is highest in Germany (24%), followed by the UK (22%) and France (18%).

M&A activity has grown significantly, with over 15 major deals recorded between 2023 and 2025. Strategic partnerships between manufacturers and streaming platforms have increased by 28%, enhancing content availability. Collaborations with semiconductor companies have improved chip efficiency by 14%, supporting innovation.

New Product

New product development accounts for 18% of total industry activity, with over 120 new models launched in 2025 alone. Performance improvements include 25% better color accuracy and 30% higher brightness levels. AI integration has improved content recommendation accuracy by 22%, enhancing user experience.

Recent Development in Europe 4K Ultra HD Television Market

- 2025: Samsung increased QLED production by 18%, reaching 10 million units annually, enhancing market competitiveness.

- 2024: LG expanded OLED production by 22%, improving panel efficiency by 15% and reducing costs by 12%.

- 2023: Sony introduced AI-powered TVs, improving image processing speed by 20% and boosting sales by 14%.

Research Methodology for Europe 4K Ultra HD Television Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 60% of market participants. Secondary research involves analyzing company reports, industry publications, and government data, accounting for 40% of the data sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a margin of 5%. Data triangulation is applied to validate findings, while statistical models are used to forecast growth trends based on historical data from 2022 to 2025.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.