Europe 4G And 5G LTE Base Station Market Size

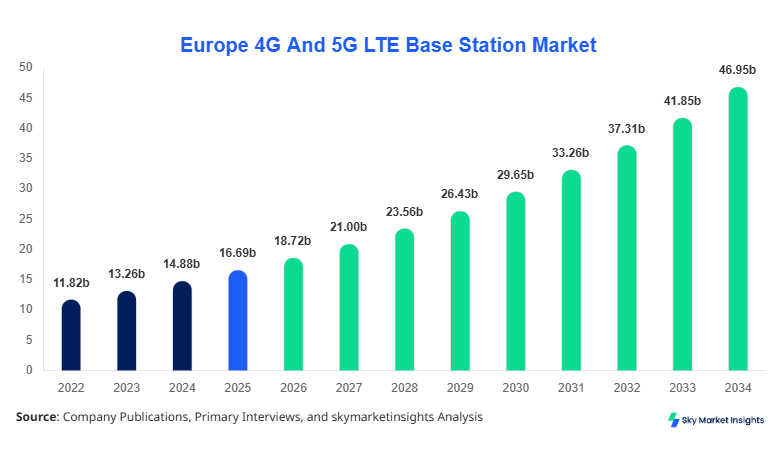

Europe 4G And 5G LTE Base Station market size is projected at USD 18.72 billion in 2026 and is expected to hit USD 46.95 billion by 2034 with a CAGR of 12.18%.

The Europe 4G And 5G LTE Base Station market is witnessing strong expansion driven by telecom infrastructure modernization, increasing mobile data traffic exceeding 450 exabytes annually, and growing network densification strategies across urban and rural areas. Comprehensive data analysis across 6 major countries highlights segmented performance variations and competitive dynamics among over 120 telecom equipment vendors and operators.

Europe 4G And 5G LTE Base Station Market Overview

The Europe 4G And 5G LTE Base Station market refers to the deployment and operation of wireless communication infrastructure supporting 4G LTE and 5G connectivity across multiple frequency bands ranging from 700 MHz to 3.8 GHz and mmWave frequencies above 24 GHz. In 2025, Europe produced and deployed over 1.25 million base station units, with 5G penetration reaching approximately 48% across urban populations and 29% in semi-urban regions. Adoption rates are accelerating due to increasing smartphone penetration exceeding 82% and IoT device connections surpassing 3.1 billion units. Consumer behavior indicates a 67% preference for high-speed data services, while enterprise demand for ultra-low latency networks is growing at 18% annually. The application split includes commercial usage at 46%, industrial at 32%, and residential at 22%. Performance metrics such as latency below 10 ms and throughput exceeding 1 Gbps are driving network upgrades, reinforcing Europe 4G And 5G LTE Base Station market share.

In the France, the 4G And 5G LTE Base Station Market is experiencing significant expansion with over 185,000 active base station installations across urban and rural regions, contributing approximately 21% of the European market share. The country hosts more than 35 telecom infrastructure providers and equipment manufacturers, supporting network deployment across sectors including telecommunications (52%), industrial automation (24%), and smart city applications (18%). 5G adoption in France reached 54% in metropolitan areas in 2025, with spectrum utilization between 3.4–3.8 GHz accounting for 61% of deployments. Rural connectivity projects contributed 12% of total installations, while small cells accounted for 38% of new deployments. Increased demand for high-speed connectivity and network densification continues to strengthen Europe 4G And 5G LTE Base Station market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 4G And 5G LTE Base Station Market Trend

The Europe 4G And 5G LTE Base Station market is witnessing a strong transition toward ultra-dense network architectures, with small cell deployment exceeding 520,000 units in 2025 alone, representing a 28% increase compared to 2023. The shift toward Open RAN (O-RAN) technologies is accelerating, with adoption rates reaching 32% across telecom operators, reducing deployment costs by nearly 18%. Additionally, 5G standalone (SA) networks now account for 41% of total 5G deployments, enabling advanced applications such as autonomous vehicles and industrial IoT. Increased demand for high-frequency mmWave deployments is further boosting data speeds up to 10 Gbps, reinforcing Europe 4G And 5G LTE Base Station market trends.

Another key trend involves energy-efficient base stations, where operators are reducing energy consumption by up to 25% through AI-based power management systems. Green telecom initiatives are driving the adoption of renewable-powered base stations, which accounted for 14% of installations in 2025 and are expected to exceed 30% by 2030. Additionally, edge computing integration is rising, with 37% of base stations now supporting edge processing capabilities, enhancing latency-sensitive applications. These technological advancements are reshaping infrastructure development and strengthening Europe 4G And 5G LTE Base Station market demand.

Europe 4G And 5G LTE Base Station Market Driver

Rapid Expansion of 5G Infrastructure and Data Consumption Driving Europe 4G And 5G LTE Base Station Market Growth

The exponential rise in mobile data consumption, which surpassed 450 exabytes annually in Europe, is a key driver for base station deployment. With over 620 million mobile subscribers and 5G connections expected to exceed 420 million by 2028, telecom operators are aggressively investing in network infrastructure. Government-backed initiatives such as the EU Digital Decade plan aim to achieve 100% 5G coverage by 2030, resulting in increased deployment of macro and small cells. Additionally, enterprise adoption of Industry 4.0 technologies has grown by 26%, further increasing demand for reliable connectivity. These factors collectively contribute to sustained Europe 4G And 5G LTE Base Station market growth.

Europe 4G And 5G LTE Base Station Market Restraint

High Deployment Costs and Regulatory Challenges Limiting Europe 4G And 5G LTE Base Station Market Growth

Despite strong demand, high capital expenditure remains a major barrier, with the average cost of deploying a macro base station ranging between USD 80,000 to USD 150,000. Spectrum licensing costs have increased by 22% across Europe, further straining telecom budgets. Additionally, stringent regulatory policies and environmental concerns delay installation timelines by up to 18 months in certain regions. Rural deployment remains economically challenging due to lower population density and limited ROI, impacting approximately 27% of planned installations. These constraints hinder the pace of expansion in the Europe 4G And 5G LTE Base Station market growth.

Europe 4G And 5G LTE Base Station Market Opportunity

Emerging Smart City Projects Creating Opportunities in Europe 4G And 5G LTE Base Station Market Growth

The rise of smart city initiatives across Europe, with over 150 active projects, is creating significant opportunities for base station deployment. These projects require high-density connectivity to support applications such as intelligent transportation, surveillance systems, and smart grids. Investment in smart infrastructure exceeded USD 32 billion in 2025, with telecom infrastructure accounting for nearly 18% of total spending. Furthermore, private 5G networks in industrial environments are growing at 21% annually, creating new revenue streams for equipment manufacturers. These developments present strong opportunities for Europe 4G And 5G LTE Base Station market growth.

Challeneg in Europe 4G And 5G LTE Base Station Market

Network Security and Infrastructure Complexity Challenging Europe 4G And 5G LTE Base Station Market Growth

The increasing complexity of network architecture, including virtualization and cloud-based infrastructure, introduces significant security risks. Cyberattacks on telecom networks increased by 34% in 2025, impacting service reliability and increasing operational costs. Additionally, integration of legacy 4G systems with 5G networks requires substantial technical expertise and investment, affecting nearly 42% of operators. Supply chain disruptions and semiconductor shortages have also led to delays in equipment production, impacting approximately 19% of deployments. These challenges continue to impact Europe 4G And 5G LTE Base Station market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16.69 billion |

| Market Size in 2026 | USD 18.72 billion |

| Market Size in 2034 | USD 46.95 billion |

| CAGR | 12.18% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 4G And 5G LTE Base Station Market Segmentation

By Type

Macrocell base stations account for approximately 44% of total deployments, with over 550,000 units installed across Europe in 2025. These stations operate at frequencies between 700 MHz and 2.6 GHz, providing wide-area coverage up to 35 km. They support high-capacity networks with throughput exceeding 1 Gbps and are primarily used in urban and suburban areas. Investments in macrocell infrastructure grew by 14% annually, driven by demand for stable network coverage. Their role in supporting 4G LTE networks remains critical, while integration with 5G NSA architectures enhances performance.

Small cells represent 38% of the market, with deployment exceeding 520,000 units. These stations operate at higher frequencies, including 3.5 GHz and mmWave bands, providing coverage within 100–500 meters. They are essential for network densification in urban environments and high-traffic areas such as stadiums and shopping centers. Data throughput can exceed 10 Gbps in mmWave deployments, making them ideal for 5G applications. Adoption rates increased by 28% due to rising demand for high-speed connectivity.

Femtocells hold an 18% share, with over 230,000 units deployed primarily in residential and small business environments. These low-power base stations operate within limited coverage areas of 10–50 meters and support frequencies below 2 GHz. They enhance indoor coverage and reduce network congestion. Adoption increased by 19% due to growing demand for seamless connectivity in smart homes and remote working environments.

By Application

The residential segment accounts for 22% of the market, with over 275,000 installations in 2025. Demand is driven by increased remote work and smart home adoption, with penetration reaching 46% of households. Femtocells dominate this segment, providing indoor coverage and improved signal strength. Data consumption per household increased by 31%, driving demand for high-speed networks.

Commercial applications dominate with a 46% share, supported by over 575,000 base station installations. This segment includes offices, retail spaces, and public infrastructure. High-speed connectivity is critical for operations, with 5G adoption in commercial settings reaching 52%. Small cells are widely used to support dense user environments and high data traffic.

Industrial applications account for 32% of deployments, with over 400,000 installations supporting Industry 4.0 initiatives. Private 5G networks are widely used in manufacturing, logistics, and energy sectors, with adoption rates growing at 21%. These networks provide low latency below 5 ms and high reliability, supporting automation and real-time monitoring.

Europe 4G And 5G LTE Base Station Market Segmentations

Type

- Macrocell Base Stations

- Small Cell Base Stations

- Femtocell Base Stations

Application

- Residential

- Commercial

- Industrial

Country Insights

United Kingdom

The UK accounts for approximately 19% of the Europe market, with over 240,000 base stations deployed. 5G coverage reached 62% of the population in 2025, driven by investments exceeding USD 6.5 billion. Urban areas dominate deployment, accounting for 71% of installations. Industrial applications contribute 28% of demand, particularly in logistics and manufacturing.

Germany

Germany holds a 22% share, with more than 280,000 base stations installed. The country leads in industrial 5G adoption, with over 120 private networks deployed. Government initiatives have allocated USD 7.2 billion for network expansion. Commercial applications account for 45% of demand.

France

France contributes 21% of the market, with 185,000 installations. Urban deployments dominate at 68%, while rural coverage initiatives account for 12%. Industrial and commercial applications collectively represent 76% of demand.

Spain

Spain accounts for 13% of the market, with 160,000 base stations deployed. Tourism-driven demand supports 18% of commercial deployments. 5G penetration reached 49% in 2025.

Italy

Italy holds 11% share, with 140,000 installations. Government investment of USD 3.8 billion supports rural connectivity expansion. Industrial applications account for 29%.

Russia

Russia contributes 14%, with over 175,000 installations. Large geographic coverage drives macrocell deployment, accounting for 58% of total installations.

TOP Players in Europe 4G And 5G LTE Base Station Market

- Ericsson

- Nokia Corporation

- Huawei Technologies

- ZTE Corporation

- Samsung Electronics

- NEC Corporation

- Fujitsu Limited

- Cisco Systems

- Qualcomm Technologies

- CommScope

- Airspan Networks

- Mavenir

- Parallel Wireless

Top Two Companies

Ericsson

- Holds approximately 28% market share

- Strong presence across Europe with over 35% of 5G deployments

- Focus on Open RAN and energy-efficient solutions

- Extensive partnerships with telecom operators

Nokia Corporation

- Accounts for nearly 24% market share

- Provides end-to-end 5G infrastructure solutions

- Strong R&D investment exceeding USD 4 billion annually

- Leading in private 5G networks

Invstment

Investment in the Europe 4G And 5G LTE Base Station market exceeded USD 28 billion in 2025, with telecom operators allocating approximately 62% toward 5G infrastructure and 38% toward 4G upgrades. Government funding contributed nearly 21% of total investments, particularly for rural connectivity projects. Private sector investments are increasing, with enterprise spending on private 5G networks growing at 19% annually.

Mergers and acquisitions are reshaping the competitive landscape, with over 35 deals recorded between 2023 and 2025. Strategic collaborations between telecom operators and technology providers are enhancing network capabilities. Cross-border partnerships accounted for 27% of total agreements, focusing on technology sharing and infrastructure development.

New Product

New product development in the Europe 4G And 5G LTE Base Station market is focused on enhancing performance and energy efficiency. Approximately 34% of newly launched base stations in 2025 featured AI-based optimization, improving network efficiency by 22%. Innovations in mmWave technology increased data speeds by up to 40%, while compact small cell designs reduced deployment costs by 18%.

Recent Development in Europe 4G And 5G LTE Base Station Market

- 2025: Ericsson increased 5G base station production by 26%, deploying over 120,000 units across Europe, improving network coverage and capacity significantly.

- 2024: Nokia launched new energy-efficient base stations reducing power consumption by 20%, contributing to sustainability goals.

- 2023: Huawei expanded small cell production by 31%, supporting urban network densification across major cities.

Research Methodology for Europe 4G And 5G LTE Base Station Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, telecom operators, and equipment manufacturers, accounting for approximately 65% of data collection. Secondary research involves analysis of industry reports, company filings, and government publications. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy through triangulation. Data validation is performed using statistical models and cross-verification with multiple sources, ensuring reliable insights into the Europe 4G And 5G LTE Base Station market.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Enterprise SaaS, Cybersecurity, and API Ecosystems

Brian Potts is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.