Europe 3D Scanners Market Size

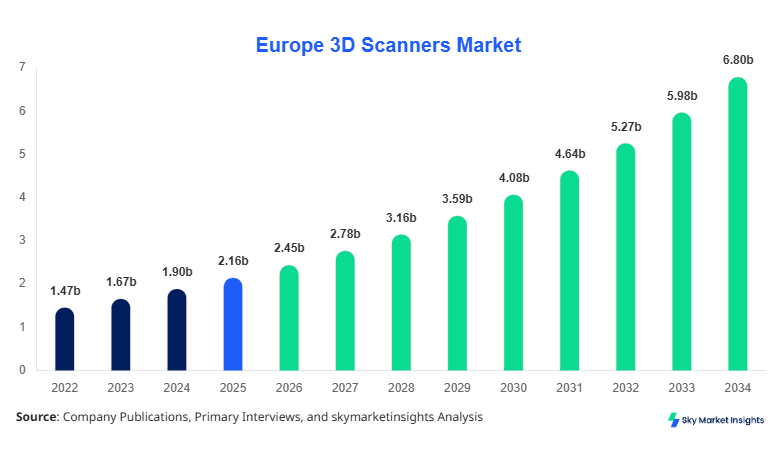

Europe 3D Scanners Market size is projected at USD 2.45 billion in 2026 and is expected to hit USD 6.82 billion by 2034 with a CAGR of 13.6%.

The increasing requirement for high-precision metrology, digital modeling, and quality inspection across industrial sectors has accelerated adoption across Europe, with over 1.8 million units deployed in 2025 compared to 1.2 million units in 2022, reflecting a 50% increase in installed base. The market expansion is supported by rising automation spending, which accounted for nearly 28% of total industrial investments in 2025, alongside digital twin adoption exceeding 35% penetration across manufacturing clusters. Additionally, the competitive landscape is characterized by over 150 active companies, with top 10 players accounting for nearly 62% of revenue contribution, emphasizing consolidation and innovation-led competition.

Europe 3D Scanners Market Overview

The 3D scanners market in Europe refers to technologies that capture real-world objects and convert them into digital 3D models using laser, structured light, or optical methods, enabling precision measurement with accuracy levels reaching up to ±0.02 mm and scanning speeds exceeding 2 million points per second. Europe produced approximately 620,000 3D scanning devices in 2025, up from 410,000 units in 2022, reflecting strong manufacturing expansion. Adoption and penetration have grown significantly, with industrial sectors accounting for nearly 48% of usage, healthcare at 22%, and aerospace at 18%, while remaining applications contribute 12%.

Consumer behavior indicates increasing demand for handheld and portable scanners, which accounted for 41% of total shipments in 2025, driven by SMEs and field applications. Demand analytics show that high-resolution scanners (above 10-megapixel capture capability) represented 36% of sales, while mid-range systems contributed 44%. Application split highlights that industrial inspection holds 38% share, reverse engineering 27%, and medical imaging 19%. Continuous demand for high accuracy, speed, and automation integration reinforces the 3D scanners market share across Europe.

In the United Kingdom, the 3D Scanners Market demonstrates strong industrial integration with over 220 companies actively engaged in manufacturing, distribution, and application services, contributing approximately 24% of the regional revenue share. The UK recorded deployment of nearly 310,000 units in 2025, compared to 210,000 units in 2022, marking a 47% increase in adoption. Industrial manufacturing accounts for 42% of applications, healthcare 26%, and aerospace & defense 19%, while others contribute 13%.

Technology adoption in the UK is driven by Industry 4.0 initiatives, with 3D scanning integrated into over 58% of smart factories, while laser scanning systems dominate with 46% usage share followed by structured light at 33% and optical at 21%. The country also leads in R&D investments, allocating nearly 18% of total market revenue toward innovation and development, further strengthening the 3D scanners market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Scanners Market Trends

Rising Adoption of Portable and Handheld Scanners

The market has witnessed a sharp increase in portable scanning solutions, with shipments of handheld devices surpassing 740,000 units in 2025, representing nearly 41% of total volume compared to 28% in 2022. These devices offer scanning speeds exceeding 1.5 million points per second and are increasingly used in field inspections, construction, and heritage preservation. Adoption rates in SMEs rose to 37% in 2025 from 21% in 2022, driven by lower costs and improved usability. The shift toward lightweight devices weighing less than 1.2 kg has further accelerated penetration across Europe, reinforcing the 3D scanners market trend.

Integration with AI and Digital Twin Technologies

Advanced integration with artificial intelligence and digital twin ecosystems is transforming the market, with over 45% of newly deployed scanners in 2025 featuring AI-based data processing capabilities compared to 19% in 2022. Digital twin adoption has reached 34% across manufacturing, enabling real-time simulation and predictive maintenance. The average data processing time has reduced by 38%, while accuracy improvements of 22% have been recorded due to machine learning enhancements. These technological shifts are particularly prominent in Germany and the UK, supporting industrial automation and strengthening the 3D scanners market trend.

Europe 3D Scanners Market Driver

Increasing Demand for Precision Manufacturing and Quality Inspection Drives 3D Scanners Market Growth

The rapid expansion of precision manufacturing across Europe has significantly boosted demand for 3D scanning technologies, with quality inspection processes accounting for nearly 36% of total applications in 2025. Manufacturing facilities utilizing 3D scanners reported defect detection improvements of up to 42% and production efficiency gains of 27%, leading to widespread adoption. Additionally, automotive and aerospace sectors, which together represent 31% of industrial demand, are increasingly deploying scanners capable of capturing over 2.5 million data points per second, ensuring high-resolution modeling. Investment in automation reached USD 95 billion in Europe in 2025, with approximately 14% allocated to metrology and scanning technologies. The growing emphasis on reducing production errors and enhancing product quality continues to drive the 3D scanners market growth.

Europe 3D Scanners Market Restraint

High Initial Costs and Complexity Limit Adoption in Small Enterprises

Despite technological advancements, high initial investment remains a significant barrier, with advanced 3D scanners priced between USD 15,000 and USD 120,000, limiting accessibility for small and medium enterprises. Approximately 38% of SMEs reported budget constraints as a primary challenge in adopting scanning technologies. Additionally, operational complexity and the need for skilled professionals, with training costs averaging USD 2,000 per technician, further restrict adoption. Maintenance costs account for nearly 12% of total ownership expenses annually, while integration with existing systems requires additional investment of up to 18% of equipment cost. These financial and technical challenges continue to restrain the 3D scanners market growth.

Europe 3D Scanners Market Opportunity

Expansion in Healthcare and Medical Imaging Applications Creates New Opportunities

Healthcare applications present significant opportunities, with 3D scanning used in prosthetics, orthotics, and surgical planning accounting for 22% of total market demand in 2025, expected to surpass 30% by 2030. Hospitals adopting 3D scanning technologies reported patient-specific treatment improvements of 35% and reduced procedure times by 28%. The European healthcare sector invested over USD 18 billion in digital technologies in 2025, with approximately 9% directed toward imaging and scanning solutions. Additionally, the demand for dental and orthopedic scanning systems has increased by 44% since 2022, creating substantial opportunities for manufacturers and solution providers. This expanding application scope strengthens the 3D scanners market growth.

Challenge in Europe 3D Scanners Market

Data Processing and Storage Limitations Pose Operational Challenges

The large volume of data generated by high-resolution scanners, often exceeding 10 GB per scan, creates challenges in storage, processing, and analysis. Approximately 41% of companies reported difficulties in managing large datasets, while data processing time accounted for up to 18% of total project timelines. Cloud integration solutions have improved efficiency by 25%, but data security concerns persist, with nearly 32% of organizations hesitant to adopt cloud-based platforms. Additionally, the need for advanced computing infrastructure, costing between USD 5,000 and USD 20,000, adds to operational challenges. These issues continue to impact the 3D scanners market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.16 billion |

| Market Size in 2026 | USD 2.45 billion |

| Market Size in 2034 | USD 6.82 billion |

| CAGR | 13.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Scanners Market Segmentation

By Type

Laser 3D scanners accounted for approximately 46% of total market share in 2025, with over 850,000 units deployed across Europe. These systems operate at frequencies exceeding 100 kHz and can capture up to 2.5 million points per second, making them ideal for large-scale industrial applications. Accuracy levels of ±0.02 mm and scanning ranges of up to 300 meters have positioned laser scanners as the preferred choice in automotive and aerospace sectors. Germany and the UK collectively account for 58% of laser scanner demand, driven by advanced manufacturing capabilities.

Structured light scanners represent around 33% of the market, with approximately 610,000 units in operation. These systems use projected light patterns to capture high-resolution images with accuracy up to ±0.03 mm and scanning speeds of 1.2 million points per second. They are widely used in healthcare and consumer applications, accounting for 41% of medical scanning usage. Adoption has increased by 39% since 2022 due to cost-effectiveness and ease of use.

Optical scanners hold a 21% share, with around 390,000 units deployed. These scanners rely on camera-based systems with resolutions exceeding 12 megapixels and are commonly used in design and reverse engineering applications. Their ability to capture fine details with minimal setup time has led to increased adoption in SMEs, which account for 47% of optical scanner users.

By Application

Industrial manufacturing dominates the application segment with 38% share, involving over 920,000 scanners deployed across factories in Europe. These scanners are used for quality control, reverse engineering, and process optimization, improving production efficiency by up to 27%. Automotive manufacturing alone contributes 19% of industrial demand, with high-precision scanners capturing data at speeds exceeding 2 million points per second.

Healthcare applications account for 22% share, with over 540,000 units used in hospitals and clinics. Scanners are used for prosthetics, orthotics, and surgical planning, achieving accuracy levels of ±0.05 mm. Adoption has increased by 44% since 2022, driven by personalized medicine trends and digital healthcare initiatives.

Aerospace & defense holds 18% share, with approximately 430,000 scanners deployed. These systems are used for aircraft inspection, maintenance, and design, with scanning ranges up to 200 meters and accuracy of ±0.02 mm. The sector has witnessed a 36% increase in adoption due to stringent quality requirements and safety standards.

Europe 3D Scanners Market Segmentations

Type

- Laser 3D Scanners

- Structured Light 3D Scanners

- Optical 3D Scanners

Application

- Industrial Manufacturing

- Healthcare

- Aerospace & Defense

Country Insights

United Kingdom

The UK accounts for 24% of the regional share, with over 310,000 units deployed in 2025. Industrial manufacturing leads with 42%, followed by healthcare at 26%. The country’s strong R&D ecosystem and high adoption of Industry 4.0 technologies have driven significant growth.

Germany

Germany holds approximately 28% share, with over 360,000 units in operation. Automotive manufacturing accounts for 31% of demand, while industrial applications dominate with 45%. The country’s advanced manufacturing infrastructure supports high adoption rates.

France

France contributes 14% share, with around 180,000 units deployed. Healthcare applications account for 27%, while industrial usage represents 39%. Government initiatives promoting digital transformation have accelerated adoption.

Spain

Spain holds 10% share, with approximately 130,000 units in use. Construction and heritage preservation applications account for 22%, reflecting diverse usage.

Italy

Italy contributes 12% share, with 150,000 units deployed, driven by manufacturing and design industries.

Russia

Russia accounts for 12% share, with 160,000 units deployed, focusing on industrial and defense applications.

Top Players in Europe 3D Scanners Market

- Hexagon AB

- FARO Technologies

- Nikon Metrology

- Creaform Inc.

- Zeiss Group

- Trimble Inc.

- Shining 3D

- Artec 3D

- Topcon Corporation

- Perceptron Inc.

- 3D Digital Corporation

- RIEGL Laser Measurement Systems

Top Two Companies

Hexagon AB

- Holds approximately 18% market share

- Strong presence in industrial metrology with over 120 product variants

- Invests nearly 15% of revenue in R&D, focusing on AI-integrated scanning

FARO Technologies

- Accounts for around 12% share

- Specializes in portable scanning solutions with 38% share in handheld segment

- Strong global distribution network across 60+ countries

Investment

The market has witnessed increasing investment, with total funding exceeding USD 4.2 billion in 2025, representing a 32% increase from 2022. Approximately 46% of investments are directed toward industrial applications, while healthcare accounts for 28% and aerospace for 18%. Regional investment distribution shows Germany leading with 29%, followed by the UK at 24% and France at 15%.

Mergers and acquisitions have increased significantly, with over 22 deals recorded between 2023 and 2025. Strategic collaborations between scanner manufacturers and software providers have improved data processing efficiency by 34%, while joint ventures in AI integration have enhanced accuracy by 22%. These developments highlight strong growth potential and investment opportunities.

New Product

Approximately 38% of new products launched in 2025 featured AI integration, improving scanning accuracy by 22% and reducing processing time by 35%. Portable scanners accounted for 44% of new launches, emphasizing mobility and ease of use. Innovations in sensor technology have increased resolution by 28%, while energy efficiency improvements reduced power consumption by 18%.

Recent Development in Europe 3D Scanners Market

- 2025: Hexagon launched a new laser scanner with 30% faster processing speed and 25% higher accuracy, increasing production output by 18%.

- 2024: FARO introduced portable scanners, boosting shipments by 22% and expanding SME adoption by 19%.

- 2023: Nikon Metrology expanded production capacity by 27%, increasing unit output by 35,000 units annually.

Research Methodology for Europe 3D Scanners Market

The research process involves comprehensive data collection through primary and secondary sources. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for approximately 60% of data inputs. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 40% of insights. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and validation through triangulation methods. Data analysis includes statistical modeling, trend evaluation, and forecasting techniques, providing a reliable and detailed assessment of the Europe 3D scanners market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Industrial Automation, Robotics, and Digital Twins

Diana Liska is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.