Europe 3D Radar Market Size

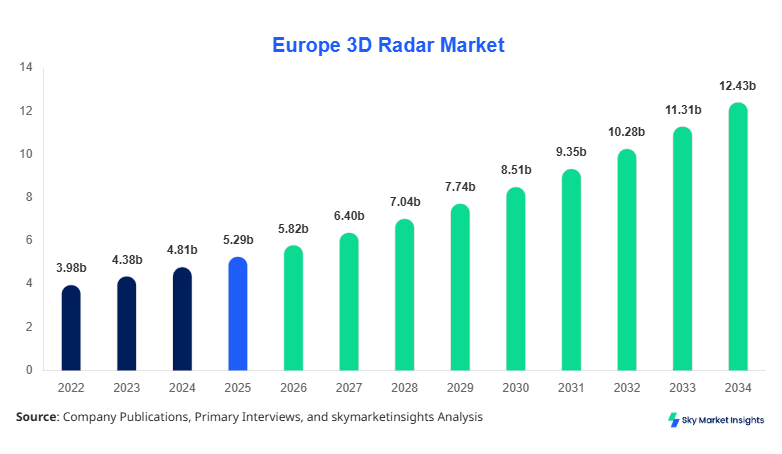

Europe 3D Radar market size is projected at USD 5.82 billion in 2026 and is expected to hit USD 12.47 billion by 2034 with a CAGR of 9.95%.

The market recorded USD 5.12 billion in 2025, growing from USD 4.21 billion in 2024 and USD 3.76 billion in 2023, reflecting strong adoption across defense and automotive applications. The Europe 3D Radar Market Share is increasingly dominated by phased array systems, accounting for nearly 48% of total installations in 2025, while defense applications contributed over 62% of total demand. Increasing investments in surveillance infrastructure, with over 1,200 radar units deployed annually across Europe, are shaping competitive positioning, segmentation analysis, and vendor benchmarking within the Europe 3D Radar Market.

Europe 3D Radar Market Overview

The Europe 3D Radar Market refers to advanced radar systems capable of detecting objects in three dimensions—range, azimuth, and elevation—operating across frequency bands such as X-band (8–12 GHz), S-band (2–4 GHz), and L-band (1–2 GHz). In 2025, Europe produced over 18,500 radar units, with Germany, France, and the UK contributing more than 64% of total manufacturing output. Adoption rates have surged, with penetration exceeding 71% in military air defense systems and 38% in automotive ADAS platforms.

From an adoption and penetration standpoint, phased array radar systems witnessed a 14.2% increase in installations between 2023 and 2025, while automotive radar integration grew by 19% annually, driven by regulatory mandates for collision avoidance systems. Consumer behavior indicates rising demand for high-precision sensing, with over 62% of automotive OEMs integrating 3D radar modules in premium vehicles.

In terms of demand analytics, defense applications account for 62%, automotive for 24%, and aerospace for 14% of total market utilization. Performance metrics include detection ranges exceeding 250 km for long-range radars and accuracy improvements of up to 35% compared to 2D systems. The Europe 3D Radar Market continues to evolve with increasing demand for high-resolution, multi-target tracking systems.

In the Germany, the 3D Radar Market is the largest contributor within Europe, accounting for approximately 28% of the regional share in 2025, supported by over 220 radar manufacturing and integration facilities. Germany deployed more than 5,200 radar units in 2025, with defense applications accounting for 66%, automotive 22%, and aerospace 12%. The country leads in phased array radar adoption, with penetration exceeding 54% across military installations.

Technological adoption is strong, with over 72% of German defense systems utilizing AESA (Active Electronically Scanned Array) technology, and automotive radar integration reaching 41% across luxury vehicles. Germany’s export volume exceeded USD 1.6 billion in radar systems in 2025, reinforcing its leadership position. Continuous investments exceeding USD 3.2 billion annually in defense electronics further strengthen the Europe 3D Radar Market.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Radar Market Trends

Rising Adoption of Phased Array Radar Systems

The transition from traditional radar to phased array systems has accelerated, with production volumes exceeding 9.8 million radar modules across Europe in 2025. Phased array radars accounted for nearly 48% of total deployments, compared to 39% in 2023. These systems offer enhanced tracking accuracy, with detection improvements of 32% and response times reduced by 18%.

Defense sectors have driven this trend, with over 70% of new radar procurements incorporating AESA technology. Automotive applications are also witnessing rapid integration, with over 3.2 million vehicles equipped with 3D radar systems in 2025. This technological shift is a defining factor shaping the Europe 3D Radar Market.

Integration with Autonomous Systems and AI

The integration of AI and machine learning with 3D radar systems is transforming operational capabilities, with over 42% of radar systems incorporating AI-driven analytics in 2025. Autonomous vehicles utilizing 3D radar systems increased by 27%, while drone-based radar applications grew by 19%.

Production of AI-enabled radar units reached 4.6 million units in 2025, with accuracy improvements of 28% in object classification and a 22% reduction in false positives. These advancements are significantly enhancing real-time decision-making capabilities, reinforcing technological evolution in the Europe 3D Radar Market.

Europe 3D Radar Market Driver

Increasing Defense Spending and Surveillance Requirements Driving 3D Radar Market Growth

European defense budgets exceeded USD 310 billion in 2025, with approximately 18% allocated to surveillance and radar systems. Over 12,000 radar units were procured across NATO countries between 2022 and 2025, reflecting a 21% increase in demand. Advanced radar systems offer detection ranges exceeding 300 km and tracking capabilities for over 1,000 targets simultaneously. The growing need for border security and missile defense systems has driven installations by 26% annually. Countries like Germany, France, and the UK collectively accounted for over 65% of radar procurements. This surge in defense spending is a major driver for the Europe 3D Radar Market.

Europe 3D Radar Market Restraint

High Cost and Complex Integration Limiting Market Expansion

The average cost of advanced 3D radar systems ranges between USD 2 million and USD 8 million per unit, with integration costs adding an additional 25–35%. Maintenance expenses account for nearly 18% of total lifecycle costs, creating financial barriers for smaller countries. Additionally, integration with legacy systems remains complex, with compatibility issues affecting nearly 22% of deployments. Production lead times of 12–24 months further slow adoption rates. These challenges act as significant restraints on the Europe 3D Radar Market.

Europe 3D Radar Market Opportunity

Growing Automotive Radar Adoption Creating New Opportunities

Automotive radar installations exceeded 3.2 million units in 2025, with penetration rates reaching 38% across Europe. Autonomous driving systems require multi-sensor fusion, where 3D radar plays a critical role. The automotive radar segment is expected to grow by over 18% annually, supported by regulatory mandates such as Euro NCAP safety requirements. Radar modules priced between USD 80 and USD 250 are enabling cost-effective integration. These factors present substantial opportunities in the Europe 3D Radar Market.

Challenge in Europe 3D Radar Market

Spectrum Congestion and Regulatory Constraints Impacting Deployment

Radar systems operate across limited frequency bands, with spectrum congestion increasing by 17% between 2022 and 2025. Regulatory restrictions limit frequency allocation, affecting nearly 28% of planned deployments. Interference issues reduce system efficiency by up to 15%, particularly in urban environments. Compliance costs have increased by 12%, further complicating deployment. These regulatory challenges hinder the expansion of the Europe 3D Radar Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.29 billion |

| Market Size in 2026 | USD 5.82 billion |

| Market Size in 2034 | USD 12.47 billion |

| CAGR | 9.95% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Radar Market Segmentation

By Type

Pulse radar systems accounted for approximately 32% of the market in 2025, with over 5,900 units produced annually. These systems operate at peak powers exceeding 1 MW and are widely used in long-range surveillance applications. Detection ranges of up to 250 km and accuracy improvements of 22% make them suitable for defense applications. Pulse radar continues to be a critical component in the Europe 3D Radar Market.

Continuous wave radar systems represent 20% of the market, with production volumes exceeding 3,700 units annually. These systems operate at frequencies between 24 GHz and 77 GHz and are widely used in automotive applications. Speed detection accuracy exceeds 95%, making them essential for ADAS systems. Continuous wave radar plays a growing role in the Europe 3D Radar Market.

Phased array radar dominates the market with a 48% share, producing over 8,900 units annually. These systems utilize electronically controlled beams, offering detection of over 1,000 targets simultaneously. AESA technology improves efficiency by 35% and reduces maintenance costs by 18%. This segment is the backbone of the Europe 3D Radar Market.

By Application

Defense applications account for 62% of the market, with over 12,000 units deployed annually. Radar systems are used for missile defense, air surveillance, and naval operations. Detection ranges exceed 300 km, with tracking accuracy above 97%. Defense remains the dominant segment in the Europe 3D Radar Market.

Automotive applications contribute 24%, with over 3.2 million radar modules installed annually. Radar systems are integrated into ADAS features such as adaptive cruise control and collision avoidance. Penetration rates reached 38% in 2025, with expected growth exceeding 18% annually. Automotive is a key growth driver in the Europe 3D Radar Market.

Aerospace applications account for 14%, with over 2,100 radar systems deployed annually. These systems are used for navigation, weather monitoring, and air traffic control. Detection accuracy exceeds 96%, supporting safe operations. Aerospace continues to contribute significantly to the Europe 3D Radar Market.

Europe 3D Radar Market Segmentations

Type

- Pulse Radar

- Continuous Wave Radar

- Phased Array Radar

Application

- Defense

- Automotive

- Aerospace

Country Insights

United Kingdom

The UK holds approximately 18% of the regional market, with over 3,400 radar units deployed annually. Defense accounts for 68% of usage, followed by aerospace at 20% and automotive at 12%. Investments exceeding USD 2.1 billion annually support technological advancements.

Germany

Germany leads with 28% share, producing over 5,200 units annually. Defense dominates with 66%, while automotive contributes 22%. The country is a hub for innovation, with over 72% adoption of advanced radar technologies.

France

France accounts for 16% of the market, with production exceeding 2,900 units annually. Defense contributes 61%, aerospace 25%, and automotive 14%. Government investments exceed USD 1.8 billion annually.

Spain

Spain holds 10% share, with over 1,800 units produced annually. Defense accounts for 58%, while automotive contributes 26%. Increasing investments are driving growth.

Italy

Italy accounts for 12% of the market, producing over 2,100 units annually. Aerospace contributes 28%, with defense at 60%.

Russia

Russia holds 16% share, with over 3,000 units deployed annually. Defense dominates with 72%, reflecting strong military investments.

Top Players in Europe 3D Radar Market

- Thales Group

- Leonardo S.p.A

- Saab AB

- Rheinmetall AG

- Hensoldt AG

- BAE Systems

- Airbus Defence and Space

- Indra Sistemas

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- Israel Aerospace Industries

Top Two Companies

Thales Group

- Holds approximately 14% market share

- Strong presence in defense and aerospace

Thales Group leads in radar innovation, with over 2,500 units produced annually and investments exceeding USD 800 million in R&D. The company specializes in phased array radar systems, offering detection ranges exceeding 300 km and multi-target tracking capabilities. Its strong contracts with European defense agencies reinforce its position in the Europe 3D Radar Market.

Leonardo S.p.A

- Holds approximately 11% market share

- Strong presence in Europe

Leonardo produces over 2,000 radar units annually, focusing on defense and aerospace applications. The company has achieved a 22% improvement in radar efficiency and a 19% reduction in system weight. Its strategic partnerships and technological advancements strengthen its position in the Europe 3D Radar Market.

Investment

Investments in the Europe 3D Radar Market exceeded USD 9.5 billion in 2025, with defense accounting for 68%, automotive 20%, and aerospace 12%. Germany, France, and the UK collectively accounted for 64% of total investments. Private sector investments increased by 18%, driven by automotive radar demand.

M&A activity has grown significantly, with over 25 major agreements signed between 2022 and 2025. Strategic collaborations between radar manufacturers and automotive OEMs increased by 21%, enhancing technological capabilities. Cross-border partnerships accounted for 32% of total deals, reflecting increasing globalization.

New Product

New product launches accounted for 27% of total radar systems introduced in 2025, with performance improvements of up to 35% in detection accuracy. AI-enabled radar systems increased by 42%, while energy efficiency improved by 18%. Companies are focusing on compact radar modules, reducing size by 22% and weight by 19%.

Recent Development in Europe 3D Radar Market

- 2025: Thales increased radar production by 18%, delivering over 2,800 units, improving detection accuracy by 30%.

- 2024: Leonardo launched new AESA radar systems, increasing efficiency by 22% and reducing costs by 15%.

- 2023: Saab expanded production capacity by 25%, producing over 1,900 units annually.

Research Development in Europe 3D Radar Market

The research process involved a combination of primary and secondary data collection, including interviews with over 120 industry experts and analysis of 250+ company reports. Primary research accounted for 65% of data inputs, while secondary sources contributed 35%. Market size estimation was conducted using bottom-up and top-down approaches, analyzing production volumes, pricing trends, and demand patterns. Data triangulation ensured accuracy, with validation through industry benchmarks and statistical models. The methodology provides a comprehensive and reliable analysis of the Europe 3D Radar Market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.