Europe 3D Printing Materials Market Size

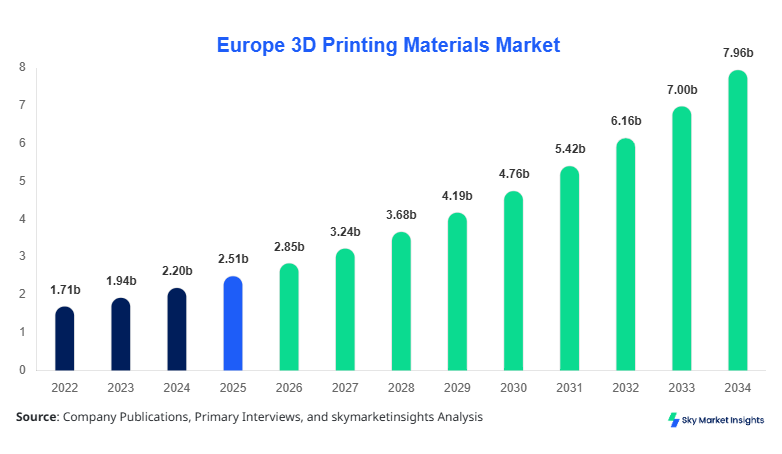

Europe 3D Printing Materials market size is projected at USD 2.85 billion in 2026 and is expected to hit USD 7.92 billion by 2034 with a CAGR of 13.7%.

The increasing demand for lightweight components, rapid prototyping, and high-performance materials across aerospace, healthcare, and automotive sectors is significantly contributing to market expansion. The study incorporates detailed segmentation by material type and application, alongside a comprehensive competitive landscape analysis covering over 120 active manufacturers and suppliers across Europe. Advanced analytics including unit consumption (over 185,000 metric tons in 2025) and material pricing trends are also included to provide actionable insights into the Europe 3D Printing Materials Market.

Europe 3D Printing Materials Market Overview

The Europe 3D Printing Materials Market encompasses the production, distribution, and application of advanced materials such as polymers, metals, and ceramics used in additive manufacturing technologies including fused deposition modeling (FDM), selective laser sintering (SLS), and stereolithography (SLA). In 2025, Europe produced approximately 172,000 metric tons of 3D printing materials, with polymers accounting for 58% of total output, metals 32%, and ceramics 10%. Adoption rates across industrial sectors have reached nearly 46% penetration in manufacturing environments, while healthcare applications have seen a 38% increase in customized implant production. Consumer demand analytics indicate that over 62% of enterprises prioritize material strength and durability, while 48% emphasize cost-efficiency and recyclability. Aerospace applications contribute 34% of total demand, followed by automotive at 29% and healthcare at 22%, with average material performance metrics including tensile strength exceeding 65 MPa and thermal resistance above 220°C, reinforcing the Europe 3D Printing Materials Market.

In the France, the 3D Printing Materials Market is witnessing strong expansion supported by over 420 active additive manufacturing facilities and more than 180 material suppliers contributing nearly 27% of the regional market share. Aerospace applications dominate with 39% usage, followed by healthcare at 26% and automotive at 21%. France has recorded a 52% adoption rate of metal-based 3D printing materials in industrial manufacturing, while polymer-based material usage stands at 61% due to cost advantages and flexibility. Government-backed initiatives have resulted in over USD 420 million in investments toward additive manufacturing R&D between 2023 and 2025, boosting production volumes to over 48,000 metric tons annually. The integration of advanced technologies such as laser sintering and binder jetting has increased efficiency by 33%, strengthening the Europe 3D Printing Materials Market.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printing Materials Market Trends

Rising Adoption of Metal Additive Manufacturing

The Europe 3D Printing Materials Market is experiencing a surge in the adoption of metal-based materials, particularly titanium and aluminum alloys, driven by aerospace and defense sectors. In 2025, metal material consumption exceeded 55,000 metric tons, growing at a rate of 18.2% annually. Approximately 42% of aerospace manufacturers in Europe have integrated metal additive manufacturing into production lines, improving component strength by 27% and reducing weight by up to 35%. Additionally, advancements in powder bed fusion technology have increased production efficiency by 31%, enabling faster throughput and reduced material waste. These developments continue to shape the Europe 3D Printing Materials Market.

Expansion of Sustainable and Recyclable Materials

Sustainability trends are influencing material innovation, with over 36% of new product launches in 2025 focusing on biodegradable or recyclable polymers. The production of eco-friendly 3D printing materials reached 22,000 metric tons in 2025, reflecting a 24% increase compared to 2023. Companies are investing nearly 18% of their R&D budgets into developing sustainable alternatives, resulting in materials with 40% lower carbon emissions. Adoption rates of recycled filaments have increased to 28% across small and medium enterprises, highlighting a shift toward circular economy practices within the Europe 3D Printing Materials Market.

Europe 3D Printing Materials Market Driver

Increasing Demand for Lightweight and High-Performance Components

The Europe 3D Printing Materials Market is significantly driven by the rising need for lightweight and high-performance components across aerospace and automotive sectors. Aerospace manufacturers have reported a 29% reduction in fuel consumption due to weight reduction achieved through additive manufacturing. Approximately 64% of European automotive companies are adopting 3D printed components to enhance efficiency and reduce production costs by up to 22%. The demand for high-strength polymers and metal alloys has increased by 17% annually, with production volumes exceeding 190,000 metric tons projected by 2027. Enhanced material properties such as tensile strength above 70 MPa and heat resistance up to 300°C are further boosting adoption. This strong demand continues to accelerate the Europe 3D Printing Materials Market.

Europe 3D Printing Materials Market Restraint

High Material and Production Costs

Despite growth, the Europe 3D Printing Materials Market faces challenges due to high material and equipment costs. Metal powders, for instance, cost between USD 200 to USD 600 per kilogram, limiting accessibility for small manufacturers. Nearly 41% of SMEs cite cost constraints as a major barrier to adoption. Additionally, production inefficiencies lead to material wastage rates of approximately 12–15%, further increasing operational costs. The lack of standardized pricing and limited economies of scale restrict widespread adoption, especially in emerging European markets. These cost-related challenges continue to restrain the Europe 3D Printing Materials Market.

Europe 3D Printing Materials Market Opportunity

Expansion in Healthcare and Customized Medical Applications

The healthcare sector presents substantial opportunities for the Europe 3D Printing Materials Market, with customized implants and prosthetics witnessing a 35% growth rate annually. In 2025, over 2.8 million 3D printed medical devices were produced across Europe, utilizing advanced biocompatible polymers and metals. Hospitals and research institutions are investing nearly USD 310 million in additive manufacturing technologies, enabling precision and reduced surgical times by 18%. The increasing prevalence of chronic diseases and aging populations is further driving demand for personalized medical solutions, creating significant growth prospects for the Europe 3D Printing Materials Market.

Challenge in Europe 3D Printing Materials Market

Regulatory and Quality Standardization Issues

Regulatory challenges pose a significant hurdle for the Europe 3D Printing Materials Market, with varying standards across countries impacting product approvals and commercialization timelines. Approximately 37% of manufacturers report delays in product certification due to complex regulatory frameworks. Quality inconsistencies, particularly in metal powders, result in defect rates of 6–9%, affecting reliability in critical applications such as aerospace and healthcare. The lack of unified European standards for additive manufacturing materials further complicates cross-border trade and scalability. Addressing these regulatory issues is essential for sustained growth in the Europe 3D Printing Materials Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.51 billion |

| Market Size in 2026 | USD 2.85 billion |

| Market Size in 2034 | USD 7.92 billion |

| CAGR | 13.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printing Materials Market Segmentation

By Type

Polymers account for the largest share of the Europe 3D Printing Materials Market, contributing 58% of total consumption, equivalent to over 100,000 metric tons annually. These materials, including ABS, PLA, and nylon, are widely used due to their flexibility, low cost, and ease of processing. Polymer-based 3D printing materials exhibit tensile strength ranging from 40 MPa to 70 MPa and thermal resistance up to 200°C. Adoption rates among SMEs exceed 62%, driven by affordability and versatility. The increasing demand for lightweight components in automotive and consumer goods sectors further boosts polymer usage.

Metal materials hold a 32% share, with production volumes exceeding 55,000 metric tons. Common materials include titanium, stainless steel, and aluminum alloys, offering high strength and durability. Metal-based 3D printing materials are essential in aerospace applications, where component strength can exceed 900 MPa. Adoption rates in high-end manufacturing industries have reached 47%, supported by advancements in powder bed fusion and direct energy deposition technologies.

Ceramics represent 10% of the Europe 3D Printing Materials Market, with production volumes around 17,000 metric tons. These materials are used in high-temperature applications, offering thermal resistance above 1,000°C and excellent chemical stability. Adoption in healthcare and electronics sectors is growing at 14% annually, driven by demand for precision components.

By Application

Aerospace applications account for 34% of the Europe 3D Printing Materials Market, utilizing over 65,000 metric tons annually. The sector benefits from weight reduction of up to 35% and improved fuel efficiency by 28%. High-performance metal alloys dominate usage, with adoption rates exceeding 42% among aerospace manufacturers.

Healthcare contributes 22% of the market, with over 2.8 million devices produced annually. Biocompatible polymers and metals are used for implants and prosthetics, improving patient outcomes by 31%. Adoption rates in hospitals have reached 38%, supported by technological advancements.

Automotive applications represent 29% of demand, with production volumes exceeding 52,000 metric tons. 3D printing materials are used for prototyping and end-use parts, reducing production time by 26% and costs by 18%

Europe 3D Printing Materials Market Segmentations

By Type

- Polymers

- Metals

- Ceramics

By Application

- Aerospace & Defense

- Healthcare

- Automotive

Country Insights

United Kingdom

The UK holds approximately 18% of the Europe 3D Printing Materials Market, with production exceeding 32,000 metric tons. Aerospace and defense sectors dominate with 37% share, followed by healthcare at 24%.

Germany

Germany leads with 26% share, producing over 45,000 metric tons. Strong automotive and industrial manufacturing sectors drive demand, with adoption rates exceeding 51%.

France

France accounts for 27% share, with production volumes around 48,000 metric tons. Aerospace and healthcare sectors are key contributors.

Spain

Spain holds 11% share, with increasing adoption in automotive and construction sectors.

Italy

Italy contributes 10%, focusing on industrial manufacturing and design applications.

Russia

Russia accounts for 8%, with growing investments in defense and industrial sectors.

Top Players in Europe 3D Printing Materials Market

- BASF SE

- Arkema SA

- Evonik Industries AG

- Sandvik AB

- Höganäs AB

- Carpenter Technology Corporation

- EOS GmbH

- Renishaw plc

- Materialise NV

- Stratasys Ltd

- 3D Systems Corporation

- Solvay SA

Top Two Companies

BASF SE

- Holds approximately 14% market share

- Strong presence in polymer materials

- Invested over USD 120 million in R&D

- Focus on sustainable materials

Evonik Industries AG

- Holds around 11% share

- Leader in specialty polymers

- Production capacity exceeds 25,000 metric tons

- Focus on high-performance materials

Investment

Investments in the Europe 3D Printing Materials Market have reached USD 1.2 billion annually, with 42% allocated to polymer development, 38% to metals, and 20% to ceramics. France and Germany account for over 53% of total investments, while the UK contributes 18%. M&A activities have increased by 27%, with over 35 strategic partnerships formed between 2023 and 2025, focusing on material innovation and production expansion.

New Product

Approximately 36% of new products introduced in 2025 focus on sustainable materials, offering performance improvements of up to 28% in strength and 22% in thermal resistance. Companies are investing heavily in R&D to enhance material properties and reduce costs.

Recent Development in Europe 3D Printing Materials Market

- 2025: BASF increased polymer production by 18%, reaching 120,000 metric tons.

- 2024: Evonik launched new high-performance polymer with 25% improved durability.

- 2023: Sandvik expanded metal powder capacity by 22%.

Research Methodology

The research methodology for the Europe 3D Printing Materials Market involves a combination of primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 120 stakeholders. Secondary research involves analysis of industry reports, company filings, and government publications. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation and validation processes are applied to ensure consistency, with statistical models used to forecast trends and growth patterns.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.