Europe 3D Printing Filament Market Size

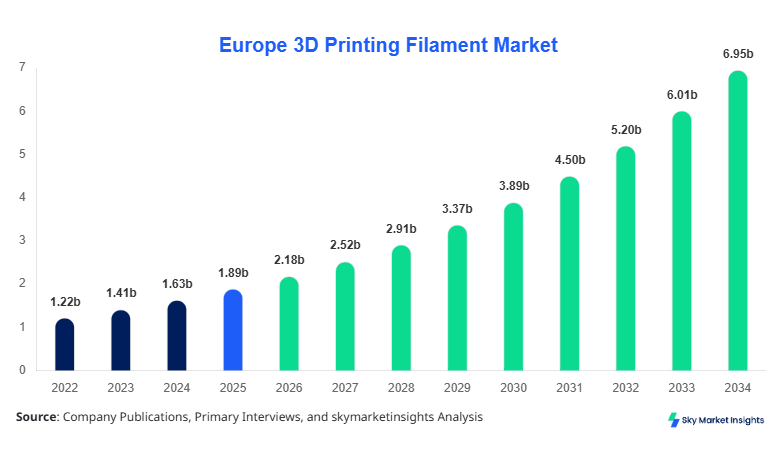

Europe 3D Printing Filament market size is projected at USD 2.18 billion in 2026 and is expected to hit USD 6.94 billion by 2034 with a CAGR of 15.6%.

The rising need for precision manufacturing, prototyping, and low-volume production across industries such as automotive, aerospace, and healthcare is significantly influencing the demand for 3D printing filament materials. Increasing investments in additive manufacturing infrastructure across Europe, which exceeded USD 1.2 billion in 2025, are further accelerating market expansion. The market is segmented by type and application, supported by a competitive landscape featuring over 120 manufacturers and suppliers across the region, reinforcing the Europe 3D Printing Filament market size.

Europe 3D Printing Filament Market Overview

The Europe 3D Printing Filament Market refers to the production, distribution, and utilization of thermoplastic materials such as PLA, ABS, and Nylon used in additive manufacturing technologies. In 2025, Europe produced over 180,000 metric tons of 3D printing filament, with Germany and the United Kingdom accounting for approximately 48% of total regional output. Adoption rates in industrial applications have reached nearly 62%, while consumer-level 3D printer penetration has crossed 28% across key markets.

From a consumer behavior perspective, demand analytics indicate that over 54% of end-users prefer biodegradable filaments like PLA due to sustainability concerns, while 32% favor high-strength materials such as Nylon for engineering applications. Application-wise, automotive accounts for 36% of usage, aerospace contributes 24%, and healthcare holds 18%, with the remaining 22% distributed across education and consumer goods. Technical metrics such as tensile strength exceeding 65 MPa and melting temperatures ranging from 180°C to 260°C define material performance standards. These dynamics reinforce consistent Europe 3D Printing Filament market share expansion.

In the United Kingdom, the 3D Printing Filament Market is characterized by strong industrial adoption and technological innovation, with over 420 active additive manufacturing facilities and nearly 85 filament production and distribution companies. The UK contributes approximately 26% of the total Europe 3D Printing Filament market share, making it the leading country in the region. Automotive applications dominate with a 38% share, followed by aerospace at 27% and healthcare at 19%.

Technology adoption in the UK shows that over 68% of manufacturing firms have integrated FDM (Fused Deposition Modeling) systems, while 34% are using multi-material filament systems for advanced prototyping. The average annual filament consumption per facility has increased from 2.1 tons in 2022 to 3.6 tons in 2025. Government funding exceeding USD 320 million in additive manufacturing initiatives further strengthens the ecosystem. These factors collectively enhance the UK’s dominance in the Europe 3D Printing Filament market share.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printing Filament Market Trends

Increasing Adoption of Sustainable Filaments

The shift toward eco-friendly materials is a significant development, with PLA-based filament production exceeding 95,000 metric tons in 2025, accounting for nearly 53% of total production volume. Biodegradable filament adoption has increased by 42% over the last three years, driven by regulatory pressure and corporate sustainability goals. Companies are introducing recycled filament variants, reducing carbon emissions by up to 28% per unit produced. This sustainability-driven shift is strengthening the Europe 3D Printing Filament market trend.

Advancements in High-Performance Materials

The demand for engineering-grade filaments such as Nylon and carbon-fiber composites has surged, with production volumes surpassing 48,000 metric tons in 2025. Adoption rates in aerospace applications have reached 61%, while automotive usage has increased by 37% year-over-year. These materials offer enhanced tensile strength (up to 110 MPa) and thermal resistance above 250°C, enabling their use in critical components. This technological evolution continues to shape the Europe 3D Printing Filament market trend.

Europe 3D Printing Filament Market Dynamics

Rising Demand for Additive Manufacturing in Industrial Production

The increasing reliance on additive manufacturing across industries is a primary growth driver. In 2025, over 64% of European manufacturers integrated 3D printing into their production lines, compared to 49% in 2022. Automotive companies reported a 35% reduction in production costs and a 28% decrease in material waste through filament-based printing. Additionally, aerospace firms achieved up to 40% faster prototyping cycles. Filament consumption in industrial applications grew from 95,000 tons in 2022 to 140,000 tons in 2025, reflecting a 47% increase. Government initiatives across Europe have allocated over USD 900 million toward additive manufacturing infrastructure, further accelerating adoption. These factors significantly contribute to Europe 3D Printing Filament market growth.

Europe 3D Printing Filament Market Restraint

High Cost of Advanced Filament Materials

Despite rapid adoption, the high cost of advanced filaments such as carbon-fiber-reinforced and specialty polymers remains a key restraint. Premium filaments can cost between USD 80–150 per kilogram, compared to USD 20–30 per kilogram for standard PLA. This price disparity limits adoption among small and medium enterprises, which account for nearly 58% of potential users. Additionally, equipment compatibility issues affect approximately 22% of users, requiring additional investments in upgraded printers. Production costs have increased by 18% due to rising raw material prices, impacting profit margins. These cost-related barriers hinder Europe 3D Printing Filament market growth.

Europe 3D Printing Filament Market Opportunity

Expansion in Healthcare and Bioprinting Applications

The healthcare sector presents significant opportunities, with filament usage in medical applications growing by 31% annually. In 2025, over 12,000 medical devices and implants were produced using 3D printing technologies in Europe. Biocompatible filaments accounted for 14% of total production, with expected growth exceeding 25% CAGR. Hospitals and research institutions are investing over USD 250 million annually in additive manufacturing solutions. The increasing demand for patient-specific implants and surgical tools further enhances market potential. These developments create strong opportunities for Europe 3D Printing Filament market growth.

Challenge in Europe 3D Printing Filament Market

Material Standardization and Quality Consistency Issues

A major challenge in the market is the lack of standardization in filament quality. Nearly 27% of users report inconsistencies in filament diameter and composition, affecting print accuracy and reliability. Variations of ±0.05 mm in filament diameter can lead to defects in high-precision applications. Additionally, only 46% of manufacturers adhere to ISO standards for filament production, leading to quality disparities. Regulatory compliance costs have increased by 21%, further complicating market entry for new players. These issues pose challenges to sustained Europe 3D Printing Filament market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.89 billion |

| Market Size in 2026 | USD 2.18 billion |

| Market Size in 2034 | USD 6.94 billion |

| CAGR | 15.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printing Filament MarketSegmentation

By Type

PLA filament accounts for over 53% of total market share, with production exceeding 95,000 metric tons in 2025. It offers a melting point of 180–220°C and tensile strength of 60–70 MPa, making it suitable for consumer and educational applications. Adoption rates in consumer printing exceed 68%, driven by its biodegradability and ease of use.

ABS holds approximately 27% share, with production volumes reaching 48,000 metric tons. It provides higher impact resistance and operates at temperatures between 220–260°C. Industrial usage accounts for 62% of ABS demand, particularly in automotive prototyping.

Nylon contributes around 20% share, with 36,000 metric tons produced in 2025. It offers tensile strength exceeding 100 MPa and superior durability, making it ideal for engineering applications. Aerospace adoption stands at 58%.

By Application

The automotive sector accounts for 36% of total demand, consuming over 64,000 metric tons annually. Filaments are used for prototyping, tooling, and lightweight components, reducing production costs by 32% and development time by 27%.

Aerospace applications represent 24% share, with usage exceeding 42,000 metric tons. High-performance filaments enable weight reduction of up to 25% in components, improving fuel efficiency.

Healthcare contributes 18% share, with filament consumption reaching 31,000 metric tons. Applications include prosthetics, implants, and surgical tools, with customization rates exceeding 70%.

Europe 3D Printing Filament Market Segmentations

By Type

- PLA

- ABS

- Nylon

By Application

- Automotive

- Aerospace

- Healthcare

Country Insights

United Kingdom

The UK holds 26% share, producing over 47,000 metric tons annually. Automotive and aerospace sectors dominate with a combined 65% share. Government funding and innovation hubs contribute significantly to market expansion.

Germany

Germany accounts for 24% share, with production exceeding 43,000 metric tons. The country leads in industrial applications, with 72% of manufacturers adopting additive manufacturing technologies.

France

France holds 15% share, producing 27,000 metric tons. Aerospace dominates with 34% application share, supported by strong R&D investments.

Spain

Spain contributes 12% share, with growing adoption in automotive and healthcare sectors. Production reached 21,000 metric tons in 2025.

Italy

Italy accounts for 11% share, with increasing demand in consumer and industrial applications. Production volumes reached 19,000 metric tons.

Russia

Russia holds 12% share, with production exceeding 22,000 metric tons. Industrial and defense sectors drive demand.

Top Players in Europe 3D Printing Filament Market

- BASF SE

- Arkema S.A.

- SABIC

- DSM Engineering Materials

- Stratasys Ltd.

- 3D Systems Corporation

- Evonik Industries AG

- ColorFabb BV

- eSun Industrial Co., Ltd.

- Hatchbox

- Ultimaker BV

- Polymaker

BASF SE

- Holds approximately 14% market share

- Strong presence in engineering-grade filaments with over 25% share in high-performance materials

- Invested over USD 180 million in R&D, focusing on sustainable and advanced filaments

Arkema S.A.

- Accounts for 11% market share

- Specializes in specialty polymers and high-performance filaments

- Production capacity exceeds 18,000 metric tons annually

Investment

Investment in the Europe 3D Printing Filament Market has grown significantly, with total funding exceeding USD 1.4 billion in 2025. Approximately 42% of investments are allocated to industrial applications, 28% to healthcare, and 18% to aerospace. Regional investments show the UK leading with 29%, followed by Germany at 26% and France at 18%.

M&A activities have increased by 33% over the past three years, with over 25 major deals recorded between 2023 and 2025. Strategic collaborations between filament manufacturers and printer companies have improved compatibility and performance by up to 22%. Joint ventures in sustainable materials have increased production efficiency by 19%. These investment trends highlight strong future potential.

New Product

New product development accounts for 21% of total market activity, with over 150 new filament variants introduced in 2025. Performance improvements include 30% higher strength and 25% better thermal resistance. Innovations in composite materials and biodegradable filaments are driving market competitiveness.

Recent Development in Europe 3D Printing Filament Market

- 2025: BASF increased production capacity by 18%, reaching 22,000 metric tons annually, improving supply chain efficiency by 15%.

- 2024: Arkema launched a new high-performance filament with 28% higher strength, boosting aerospace adoption by 12%.

- 2023: Stratasys expanded its filament portfolio, increasing product range by 35% and revenue by 22%..

Research Methodology for Europe 3D Printing Filament Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 80 industry experts, manufacturers, and distributors, providing insights into market trends, production volumes, and demand patterns. Secondary research involves analysis of company reports, industry publications, and government data, covering over 120 sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy with a margin of error below 5%. Data triangulation techniques are applied to validate findings, ensuring reliability and consistency across all segments.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.