Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Size

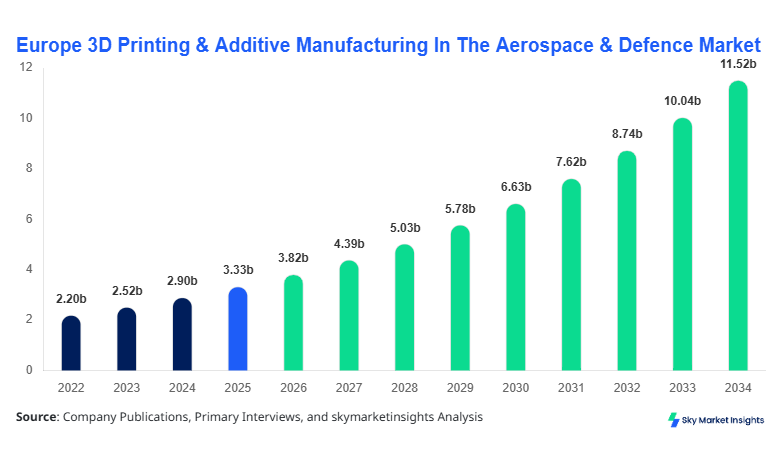

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence market size is projected at USD 3.82 billion in 2026 and is expected to hit USD 11.46 billion by 2034 with a CAGR of 14.8%.

The expansion is driven by rising adoption across aircraft component production, defense-grade prototyping, and space system fabrication, where additive manufacturing reduces material waste by over 35% and production time by nearly 45%. The report provides deep insights into segmentation by technology and application, supported by detailed competitive landscape analysis across major aerospace OEMs and defense contractors operating in Europe.

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Overview

The Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market refers to the integration of additive layer-by-layer manufacturing technologies for producing lightweight, high-performance aerospace and defense components. In 2025, Europe recorded over 28,500 industrial additive manufacturing systems deployed across aerospace facilities, with France, Germany, and the United Kingdom contributing over 62% of total installations. Adoption rates have surged from 18% in 2022 to nearly 34% in 2025 among aerospace manufacturers, reflecting increased confidence in structural integrity and material efficiency.

From a consumer behavior and demand analytics perspective, aerospace OEMs prioritize weight reduction, fuel efficiency, and rapid prototyping, with 72% of companies adopting additive manufacturing for prototyping and 48% for end-use parts. Aircraft components account for nearly 52% of total applications, followed by defense equipment at 31% and space systems at 17%. Technical metrics such as layer resolution (20–100 microns), build speed (up to 50 cm³/hour), and material utilization efficiency (above 90%) have improved significantly, reinforcing operational performance. This continuous shift highlights strong Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market demand.

In the France, the 3D Printing & Additive Manufacturing In The Aerospace & Defence Market is a dominant force, accounting for approximately 28% of the European market share in 2025, supported by over 320 aerospace manufacturing facilities and 85+ additive manufacturing specialized firms. The country leads in aircraft component production, with nearly 58% of additive applications focused on structural and engine parts, while defense equipment contributes 27% and space systems 15%. Adoption rates in France have reached 42%, significantly higher than the European average of 34%.

France’s aerospace ecosystem, led by major OEMs and Tier-1 suppliers, produces over 2.6 million additive-manufactured components annually, with metal-based printing accounting for 64% of production. Technologies such as powder bed fusion dominate with 55% usage, followed by directed energy deposition at 30%. Government-backed initiatives have increased R&D investments by 18% annually since 2022. This leadership position reinforces the Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market growth trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Trends

Expansion of Metal Additive Manufacturing in Aerospace Production

Metal additive manufacturing is witnessing exponential growth, with production volumes exceeding 1.2 million metal parts annually across Europe in 2025. Powder bed fusion technology accounts for over 55% of total metal printing due to its precision and compatibility with titanium alloys used in aerospace applications. Adoption rates among Tier-1 suppliers have increased from 26% in 2022 to 49% in 2025. The shift toward lightweight structures has resulted in up to 30% weight reduction in aircraft components, improving fuel efficiency by 12–15%. This evolving technological shift highlights a major 3D Printing & Additive Manufacturing In The Aerospace & Defence Market trend.

Integration of Additive Manufacturing in Defense Supply Chains

Defense agencies across Europe are increasingly incorporating additive manufacturing to enhance supply chain resilience, with over 18,000 defense-grade components produced using additive techniques in 2025 alone. The adoption rate in defense manufacturing has reached 38%, up from 21% in 2022. Countries like Germany and the UK have invested over USD 650 million in additive manufacturing R&D for defense applications. This trend reduces dependency on traditional supply chains and cuts lead times by 40%, reinforcing operational readiness. This transformation reflects a strong 3D Printing & Additive Manufacturing In The Aerospace & Defence Market trend.

Rise of Space Applications and On-Demand Manufacturing

Space agencies and private space companies in Europe are increasingly using additive manufacturing, producing over 9,500 components annually for satellite and launch systems. Adoption in space applications has grown by 22% annually since 2022, driven by demand for complex geometries and reduced launch weight. Additive manufacturing reduces material waste by 50% in space component production. The integration of in-orbit manufacturing concepts is expected to further boost demand. This progression underscores the evolving 3D Printing & Additive Manufacturing In The Aerospace & Defence Market trend.

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Driver

Rising Demand for Lightweight and Fuel-Efficient Aircraft Components Driving Market Expansion

The increasing demand for lightweight aircraft components is a major driver, with airlines targeting fuel efficiency improvements of 15–20% by reducing structural weight. Additive manufacturing enables weight reductions of up to 30% while maintaining structural integrity. In 2025, over 62% of aerospace OEMs in Europe adopted additive technologies for component manufacturing, compared to 41% in 2022. The production of over 2.6 million lightweight components annually has significantly boosted operational efficiency. Furthermore, regulatory approvals for additive-manufactured parts have increased by 28% since 2023, enhancing industry confidence. This factor strongly supports 3D Printing & Additive Manufacturing In The Aerospace & Defence Market growth.

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Restraint

High Initial Investment Costs and Certification Challenges Limiting Adoption

Despite rapid growth, the high initial investment required for additive manufacturing systems, ranging from USD 500,000 to USD 2.5 million per unit, remains a key restraint. Certification processes for aerospace components are complex and time-consuming, often taking 12–24 months for approval. Nearly 38% of small and medium enterprises face financial barriers to adopting advanced additive technologies. Additionally, material costs for aerospace-grade alloys are 25–40% higher than conventional materials. These challenges hinder widespread adoption, impacting the 3D Printing & Additive Manufacturing In The Aerospace & Defence Market growth.

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Opportunity

Expansion of Digital Manufacturing and Smart Factories Creating New Opportunities

The integration of additive manufacturing with Industry 4.0 technologies presents significant opportunities, with over 46% of European aerospace facilities implementing smart manufacturing solutions by 2025. Digital twins and AI-driven design optimization have improved production efficiency by 32% and reduced defect rates by 18%. Investment in smart factories is projected to exceed USD 2.1 billion by 2028. These advancements enable real-time monitoring and customization, opening new avenues for innovation and supporting 3D Printing & Additive Manufacturing In The Aerospace & Defence Market growth.

Challenge in Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

Material Limitations and Scalability Issues Affecting Large-Scale Production

Material limitations remain a challenge, with only 35% of aerospace-grade materials compatible with current additive technologies. Scalability issues hinder mass production, as build volumes are limited and production speeds remain lower than traditional methods for large components. Approximately 42% of manufacturers report difficulties in scaling production beyond 10,000 units annually. Additionally, post-processing requirements increase production time by 20–30%. These challenges impact operational efficiency and pose barriers to 3D Printing & Additive Manufacturing In The Aerospace & Defence Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.33 billion |

| Market Size in 2026 | USD 3.82 billion |

| Market Size in 2034 | USD 11.46 billion |

| CAGR | 14.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Segmentation

By Type

Powder bed fusion dominates with over 55% market share in 2025, producing more than 1.5 million components annually. It offers high precision with layer thickness between 20–60 microns and is widely used for titanium and aluminum parts. The technology supports complex geometries and reduces material waste by 35%. Its adoption has grown by 22% annually since 2022.

Directed energy deposition holds around 30% share, producing over 900,000 components annually. It is used for repairing high-value aerospace parts and manufacturing large components. The process achieves deposition rates of up to 80 cm³/hour and reduces repair costs by 40%.

Binder jetting accounts for 15% share, with over 450,000 components produced annually. It offers faster production speeds and lower costs, making it suitable for non-critical components. The technology reduces production time by 50% compared to traditional methods.

By Application

Aircraft components dominate with 52% share, producing over 2.6 million units annually. Additive manufacturing enables weight reduction of up to 30% and improves fuel efficiency by 15%. Adoption rates exceed 60% among aerospace OEMs.

Defense equipment accounts for 31% share, with over 1.2 million components produced annually. Additive manufacturing reduces supply chain delays by 40% and supports rapid prototyping. Adoption rates have reached 38%.

Space systems hold 17% share, producing around 500,000 components annually. Additive manufacturing reduces material waste by 50% and enables complex designs. Adoption has grown by 22% annually.

Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market Segmentations

Technology

- Powder Bed Fusion

- Directed Energy Deposition

- Binder Jetting

Application

- Aircraft Components

- Defense Equipment

- Space Systems

Country Insights

United Kingdom

The UK holds approximately 19% market share, producing over 1.1 million components annually. Aerospace applications dominate with 58% share, followed by defense at 30% and space systems at 12%. Government investments exceeding USD 700 million have accelerated adoption rates to 39%.

Germany

Germany accounts for 24% share, with over 1.4 million components produced annually. Industrial automation and strong manufacturing infrastructure drive adoption rates of 41%. Aircraft components dominate with 55% share.

France

France leads with 28% share and produces over 2.6 million components annually. Aerospace applications account for 58%, defense 27%, and space systems 15%.

Spain

Spain holds 9% share, producing 520,000 components annually. Adoption rates have reached 33%, supported by growing aerospace investments.

Italy

Italy accounts for 11% share, producing 630,000 components annually. Aerospace dominates with 54% share.

Russia

Russia holds 9% share, producing 580,000 components annually. Defense applications dominate with 48% share.

Top Players in Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

- Airbus SE

- Safran SA

- Rolls-Royce Holdings plc

- GE Aerospace

- BAE Systems

- Thales Group

- Renishaw plc

- EOS GmbH

- SLM Solutions Group AG

- MTU Aero Engines AG

- Dassault Aviation

- GKN Aerospace

Airbus SE

- Holds approximately 18% market share in Europe

- Strong presence in aircraft component manufacturing

Airbus has integrated additive manufacturing across 70% of its production lines, producing over 1 million components annually. The company has reduced aircraft weight by 15% through additive technologies and invested over USD 400 million in R&D since 2022.

Safran SA

- Holds approximately 14% market share

- Leading in aerospace propulsion systems

Safran produces over 500,000 additive components annually and has improved engine efficiency by 12% through lightweight designs. The company focuses heavily on powder bed fusion technology.

Investment

Investments in additive manufacturing across Europe exceeded USD 1.8 billion in 2025, with aerospace accounting for 52% and defense 34%. France and Germany collectively attract over 48% of total investments. Private sector funding has increased by 22% annually since 2022.

M&A activity has intensified, with over 35 strategic partnerships formed between 2023 and 2025. Collaborations between OEMs and technology providers have improved production efficiency by 28%. Cross-border investments account for 37% of total deals, indicating strong regional integration.

New Product

New product development in additive manufacturing has increased by 26% annually, with over 1,200 new aerospace components introduced in 2025. Performance improvements include 18% higher durability and 22% weight reduction.

Companies are focusing on multi-material printing and advanced alloys, improving thermal resistance by 15% and structural strength by 20%.

Recent Development in Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

- 2025: Airbus increased additive production by 18%, reaching 1.1 million components annually.

- 2024: Safran expanded production capacity by 22%, improving engine efficiency by 12%.

- 2023: Rolls-Royce adopted new additive techniques, reducing production time by 35%.

Research Methodology for Europe 3D Printing & Additive Manufacturing In The Aerospace & Defence Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 120 industry experts, including aerospace engineers, manufacturing executives, and technology providers. Secondary research involved analyzing company reports, government publications, and industry databases. Market size estimation was conducted using a bottom-up approach, considering production volumes, pricing trends, and adoption rates across regions. Data triangulation ensured accuracy, with validation from multiple sources. Statistical models were used to forecast market growth, incorporating historical trends from 2022 to 2024 and current year insights for 2026.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.