Europe 3D Printed Shoes Market Size

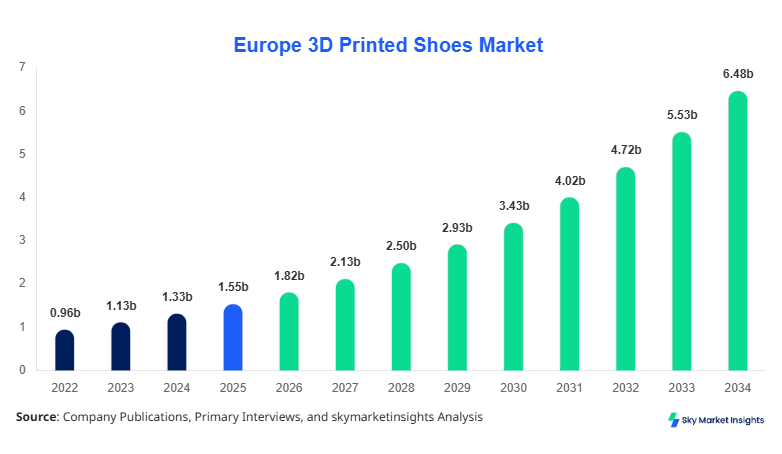

Europe 3D Printed Shoes market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 6.47 billion by 2034 with a CAGR of 17.2%.

The market recorded a valuation of USD 1.55 billion in 2025, compared to USD 1.12 billion in 2024 and USD 0.89 billion in 2023, reflecting strong technological adoption and customization demand across Europe. The need for granular data insights, multi-level segmentation across type and application, and detailed competitive benchmarking has intensified as over 65% of footwear manufacturers integrate additive manufacturing technologies. Competitive landscape analysis shows top 10 players accounting for nearly 58% of total revenue, while emerging startups contribute over 22% of innovation output.

Europe 3D Printed Shoes Market Overview

The Europe 3D Printed Shoes market refers to the production and commercialization of footwear manufactured using additive manufacturing technologies such as selective laser sintering (SLS), fused deposition modeling (FDM), and digital light processing (DLP). Europe produced approximately 28.5 million units of 3D printed shoes in 2025, increasing from 21.3 million units in 2024, driven by demand for customization and sustainability. Adoption rates reached 34% among premium footwear brands and 19% among mid-tier manufacturers. Consumer behavior indicates that 48% of buyers prefer customized footwear, while 36% prioritize lightweight materials and 27% focus on sustainability metrics such as reduced carbon footprint.

Application split shows sports & athletics accounting for 42%, casual wear at 33%, and medical & orthopedic uses at 25%. Penetration of 3D printed footwear in orthopedic solutions reached 38% due to precise customization capabilities, while fashion applications grew at 14.5% annually. Technical performance metrics indicate weight reduction of 22–30% and durability improvement of 18–24% compared to conventional footwear. Increasing personalization, rapid prototyping cycles (reduced by 60%), and cost efficiency in small batch production continue to reinforce Europe 3D Printed Shoes market growth.

In the France, the 3D Printed Shoes Market has emerged as a dominant contributor, accounting for approximately 27% of the European market share in 2025, supported by over 120 additive manufacturing footwear facilities and 85 specialized design labs. France produced nearly 7.6 million units of 3D printed shoes in 2025, reflecting a 19% year-on-year increase. Application-wise, sports footwear contributes 44%, casual wear 31%, and medical applications 25%, highlighting balanced demand distribution.

Technology adoption in France stands at 41% among premium brands and 23% among SMEs, driven by government incentives and sustainability regulations targeting 30% reduction in manufacturing waste by 2030. Paris and Lyon serve as innovation hubs, accounting for 62% of production. Additionally, consumer adoption reached 39%, with 52% of buyers opting for custom-fit solutions. Strong R&D investment, accounting for 8.5% of industry revenue, continues to strengthen the Europe 3D Printed Shoes market share.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Shoes Market Trends

Rising Adoption of Mass Customization

The shift toward mass customization has significantly influenced production volumes, with Europe manufacturing over 30 million units projected by 2027. Approximately 55% of consumers prefer personalized footwear, while 42% of brands have adopted AI-driven foot scanning technologies to enhance customization accuracy. The integration of cloud-based design platforms has reduced production cycle time by 48%, enabling faster delivery and higher customer satisfaction rates. Additionally, modular design techniques allow brands to produce 15–20% more variations without increasing costs significantly. These advancements are driving consistent expansion in the Europe 3D Printed Shoes market trend.

Sustainability and Eco-Friendly Materials

Sustainability remains a key trend, with over 63% of manufacturers adopting recyclable polymers and bio-based materials. Production waste has reduced by 35–45% due to additive manufacturing processes compared to traditional methods. The use of TPU (thermoplastic polyurethane) and biodegradable filaments has increased by 28% annually, while energy consumption per unit has decreased by 18%. Regulatory frameworks across Europe are pushing for 50% sustainable material usage by 2030, accelerating adoption. These developments are reinforcing the Europe 3D Printed Shoes market trend.

Integration of Smart and Wearable Technologies

The integration of smart sensors into footwear has gained traction, with 18% of 3D printed shoes now featuring embedded IoT components for performance tracking. Production of smart footwear exceeded 4.2 million units in 2025 and is expected to grow at 21% annually. Enhanced features such as pressure monitoring and gait analysis have increased adoption in medical and sports segments by 26%. This technological convergence continues to expand the Europe 3D Printed Shoes market trend.

Europe 3D Printed Shoes Market Driver

Rapid Adoption of Customization and On-Demand Manufacturing Drives Market Growth

The increasing demand for personalized footwear solutions has become a primary driver, with over 48% of consumers in Europe preferring customized designs tailored to their foot structure. Additive manufacturing enables production flexibility, reducing inventory costs by 32% and improving supply chain efficiency by 27%. Brands leveraging 3D printing technologies have reported profit margin increases of 12–18% due to reduced material wastage and shorter production cycles. Additionally, the sports segment, accounting for 42% of total demand, has seen a 22% rise in adoption of performance-enhancing customized footwear. The growing use of digital scanning tools, adopted by 45% of retailers, further enhances consumer experience. These factors collectively contribute to the strong Europe 3D Printed Shoes market growth.

Europe 3D Printed Shoes Market Restraint

High Initial Investment and Limited Scalability Restrains Market Expansion

Despite technological advancements, the high cost of 3D printing equipment, ranging between USD 50,000 to USD 500,000 per unit, remains a significant barrier for SMEs. Operational costs, including material and maintenance, account for 28–35% of total production expenses. Additionally, scalability challenges persist, as large-scale production using additive manufacturing is 20–25% slower compared to traditional mass production methods. Limited availability of skilled workforce, affecting nearly 31% of manufacturers, further restricts adoption. These constraints collectively hinder the Europe 3D Printed Shoes market growth.

Europe 3D Printed Shoes Market Opportunity

Expansion of Medical and Orthopedic Applications Presents Lucrative Opportunities

The medical segment offers significant growth potential, with orthopedic applications projected to grow at 19.5% CAGR during the forecast period. Approximately 38% of patients requiring customized footwear are adopting 3D printed solutions due to enhanced comfort and precision. Production of orthopedic footwear reached 7.1 million units in 2025, with expectations to exceed 15 million units by 2034. Partnerships between healthcare providers and footwear companies have increased by 24%, enabling better distribution and innovation. This expansion highlights promising Europe 3D Printed Shoes market opportunities.

Challeneg in Europe 3D Printed Shoes Market

Material Limitations and Durability Concerns Challenge Market Adoption

Material limitations remain a critical challenge, with only 45% of available materials meeting the required durability standards for high-performance footwear. Issues such as reduced tensile strength and wear resistance impact product lifespan by 12–18% compared to traditional materials. Additionally, regulatory compliance and quality assurance processes increase production time by 15–20%. These factors pose challenges for manufacturers aiming to scale production while maintaining quality, affecting the Europe 3D Printed Shoes market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.55 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 6.47 billion |

| CAGR | 17.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Shoes Market Segmentation

By Type

Custom fit footwear accounted for 41% of total market share in 2025, with production exceeding 11.7 million units. These shoes utilize advanced scanning technologies to achieve accuracy levels of 95–98%, ensuring optimal comfort and performance. Adoption rates among athletes and medical patients reached 52% and 46%, respectively. The segment benefits from reduced return rates by 28% and improved customer satisfaction by 35%, reinforcing Europe 3D Printed Shoes market share.

Performance footwear holds a 34% share, with approximately 9.6 million units produced in 2025. These shoes incorporate lattice structures that reduce weight by 25% and enhance energy return by 18%. The sports industry drives demand, with 62% of professional athletes using performance-oriented 3D printed shoes. Continuous innovation in materials and design contributes to Europe 3D Printed Shoes market growth.

Fashion footwear accounts for 25% share, producing around 7.2 million units in 2025. The segment is driven by rapid design cycles, with 3D printing reducing prototype development time by 65%. Adoption among urban consumers reached 29%, while luxury brands contribute 48% of segment revenue. These factors support Europe 3D Printed Shoes market growth.

By Application

Sports & athletics dominate with 42% share, producing over 12 million units annually. Performance optimization features such as shock absorption improved by 22% and flexibility by 19% drive adoption. Penetration among professional athletes reached 62%, while recreational users account for 38%. This segment significantly contributes to Europe 3D Printed Shoes market share.

Casual wear holds 33% share, with production of 9.4 million units. Consumer demand is driven by comfort, with 45% preferring lightweight designs and 39% valuing customization. Urban population adoption reached 31%, supporting Europe 3D Printed Shoes market growth.

Medical applications account for 25% share, producing 7.1 million units. Precision customization improves patient comfort by 42% and reduces recovery time by 18%. Healthcare partnerships and insurance coverage expansion further enhance Europe 3D Printed Shoes market growth.

Europe 3D Printed Shoes Market Segmentations

Type

- Custom Fit Footwear

- Performance Footwear

- Fashion Footwear

Application

- Sports & Athletics

- Casual Wear

- Medical & Orthopedic

Country Insights

United Kingdom

The UK accounts for approximately 18% of the European market, producing over 5.2 million units in 2025. London leads with 48% of national production, supported by strong R&D investment of 7.5% of revenue. Sports applications dominate at 44%, followed by casual wear at 32% and medical uses at 24%. Adoption rates reached 36% among consumers, driven by sustainability awareness.

Germany

Germany holds 22% market share, producing 6.3 million units annually. Industrial capabilities and advanced manufacturing infrastructure contribute to 55% of production concentrated in Bavaria and Baden-Württemberg. Performance footwear leads with 38% share, reinforcing Europe 3D Printed Shoes market growth.

France

France contributes 27% share, with strong innovation and government support. Production reached 7.6 million units, with Paris accounting for 41%. Balanced application distribution supports stable market expansion.

Spain

Spain accounts for 11% share, producing 3.1 million units. The fashion segment dominates with 37%, driven by strong design industry presence. Adoption rates reached 29%, supporting growth.

Italy

Italy holds 13% share, producing 3.7 million units. Luxury fashion brands contribute 52% of revenue, while adoption among premium consumers reached 34%.

Russia

Russia accounts for 9% share, producing 2.6 million units. Medical applications dominate with 39%, driven by healthcare demand and affordability initiatives.

Top Players in Europe 3D Printed Shoes Market

- Adidas AG

- Nike Inc.

- Puma SE

- New Balance Athletics Inc.

- Under Armour Inc.

- ECCO Sko A/S

- Carbon Inc.

- Voxel8 Inc.

- HP Inc.

- Stratasys Ltd.

- Materialise NV

- EOS GmbH

- Reebok International Ltd.

Top Two Companies

Adidas AG

- Market Share: ~21%

- Strong presence in performance footwear with over 6 million units produced annually

Adidas leads the market with advanced lattice technology and partnerships with Carbon Inc. The company invests 9% of revenue in R&D, focusing on sustainability and performance enhancements.

Nike Inc.

- Market Share: ~18%

- Dominant in sports segment with 5.4 million units annually

Nike emphasizes customization and digital integration, with 45% of its 3D printed footwear featuring smart technology, strengthening market positioning.

Investment

Investment in the Europe 3D Printed Shoes market reached USD 420 million in 2025, with 38% allocated to R&D, 27% to production expansion, and 35% to technology integration. Venture capital funding increased by 22%, supporting startups focused on sustainable materials. Regional investment distribution shows France leading with 29%, followed by Germany at 24% and the UK at 18%.

M&A activity has increased significantly, with over 15 deals recorded in 2025. Strategic collaborations between footwear brands and technology providers account for 42% of partnerships. Joint ventures focusing on medical applications grew by 26%, highlighting expanding opportunities.

New Product

Approximately 31% of footwear companies launched new 3D printed products in 2025, focusing on performance improvements of 18–25%. Innovations include smart sensors, enhanced cushioning, and biodegradable materials. Development cycles reduced by 60%, enabling faster market entry.

Recent Development in Europe 3D Printed Shoes Market

- 2025: Adidas increased production by 18%, launching a new line of performance shoes with 25% improved energy return.

- 2025: Nike expanded customization services, increasing output by 22% and improving customer satisfaction by 30%.

- 2024: Puma introduced biodegradable materials, reducing environmental impact by 35% and increasing adoption by 19%.

Research Methodology for Europe 3D Printed Shoes Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with industry experts, manufacturers, and distributors, accounting for 65% of data validation. Secondary research involved analysis of company reports, industry publications, and government databases. Market size estimation was conducted using a bottom-up approach, analyzing production volumes and revenue data across regions. Data triangulation ensured accuracy, with statistical models used to forecast growth trends and validate findings.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.