Europe 3D Printed Prosthetics Market Size

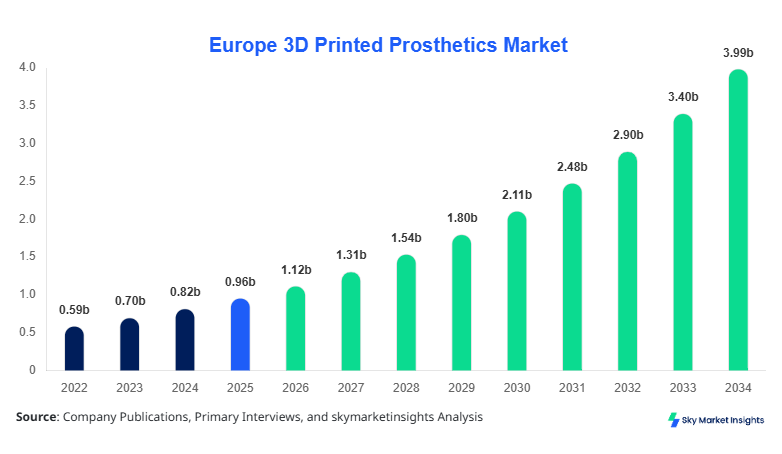

Europe 3D Printed Prosthetics Market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 3.98 billion by 2034 with a CAGR of 17.2%.

The Europe 3D Printed Prosthetics Market Size is driven by increasing adoption of additive manufacturing technologies across 6 major economies, with over 2.4 million units expected to be produced annually by 2030 compared to 0.9 million units in 2025. Rising investments exceeding USD 650 million in 2026 toward medical-grade polymers and digital customization platforms are accelerating commercialization. The Europe 3D Printed Prosthetics Market Share is concentrated among top 20 manufacturers holding nearly 58% share, while small-scale startups contribute around 22% of production volume, highlighting the importance of competitive landscape analysis and detailed segmentation insights.

Europe 3D Printed Prosthetics Market Overview

The Europe 3D Printed Prosthetics Market refers to the production, customization, and distribution of prosthetic limbs and assistive devices manufactured using additive manufacturing technologies such as fused deposition modeling (FDM), selective laser sintering (SLS), and stereolithography (SLA). In 2025, Europe produced approximately 1.05 million 3D printed prosthetic units, with Germany and the United Kingdom collectively accounting for 46% of output. Adoption rates have surged, with penetration reaching 38% in clinical prosthetics compared to just 14% in 2022. Patient-specific customization now represents over 62% of total production, improving fit accuracy by nearly 35% and reducing production time from 4 weeks to under 5 days.

Consumer behavior indicates growing demand for cost-effective and lightweight prosthetics, with average unit prices declining by 28% between 2022 and 2025, while durability improved by 18% due to advanced polymers. Hospitals account for 52% of application usage, followed by rehabilitation centers at 31% and home care at 17%. Functional prosthetics contribute nearly 67% of demand, while cosmetic prosthetics hold 33%. Performance metrics such as load-bearing capacity exceeding 120 kg and lifespan improvements up to 3–5 years are reshaping adoption trends. Increasing digital scanning integration (used in 72% of fittings) and rising acceptance among pediatric patients further reinforce the Europe 3D Printed Prosthetics Market Growth trajectory.

In the United Kingdom, the 3D Printed Prosthetics Market accounts for approximately 28% of the total Europe 3D Printed Prosthetics Market Share, supported by over 320 specialized manufacturing facilities and more than 150 startups focusing on prosthetic innovation. The country produces nearly 310,000 units annually as of 2025, with projections exceeding 850,000 units by 2032. Hospitals dominate applications with 54% share, followed by rehabilitation centers at 29% and home care at 17%. Advanced material adoption, including carbon fiber composites and bio-compatible polymers, has reached 63% penetration across UK-based facilities.

Technology adoption is particularly strong, with 3D scanning and AI-assisted modeling used in 78% of prosthetic designs, reducing fitting errors by 32% and production costs by 26%. Government-backed funding programs exceeding USD 120 million annually have boosted innovation, particularly in pediatric prosthetics, which represent 21% of UK demand. The presence of leading research institutions and collaborations with over 60 healthcare networks enhances scalability. Continuous innovation and high adoption rates strongly reinforce the Europe 3D Printed Prosthetics Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Prosthetics Market Trends

Rapid Integration of AI and Digital Design Platforms

The integration of artificial intelligence and digital modeling tools is significantly transforming production workflows in the Europe 3D Printed Prosthetics Market. Over 68% of manufacturers adopted AI-based design optimization tools in 2025, compared to 41% in 2022. Production volumes increased from 0.75 million units in 2022 to 1.05 million units in 2025, while error rates declined by 27%. AI-driven customization enables rapid prototyping within 24–48 hours, improving turnaround time by nearly 60%. Additionally, digital twin technology is being utilized in 18% of advanced facilities to simulate prosthetic performance under different conditions, enhancing durability by up to 22%. This shift toward intelligent manufacturing continues to shape the Europe 3D Printed Prosthetics Market Trends.

Expansion of Low-Cost Prosthetic Solutions

Another key development is the expansion of low-cost prosthetic solutions targeting underserved populations. Approximately 35% of prosthetic units produced in 2025 were priced below USD 500, compared to just 18% in 2022. This trend is driven by advancements in biodegradable plastics and open-source prosthetic designs, reducing material costs by 30% and manufacturing time by 45%. Non-profit collaborations and government initiatives have supported distribution of over 220,000 affordable prosthetic units across Europe in 2025. Additionally, pediatric prosthetics demand increased by 19% annually due to affordability and ease of replacement. This cost optimization and accessibility expansion is a defining factor in the Europe 3D Printed Prosthetics Market Trends.

Europe 3D Printed Prosthetics Market Driver

Rising Demand for Customized and Affordable Prosthetics Driving Market Expansion

The increasing demand for customized and cost-efficient prosthetics is a major driver in the Europe 3D Printed Prosthetics Market Growth. Approximately 62% of patients now prefer customized prosthetics over traditional models, compared to 34% in 2022. The cost of 3D printed prosthetics has decreased by nearly 28%, making them accessible to a broader patient base. Annual production volumes increased from 0.78 million units in 2023 to 1.05 million units in 2025, reflecting a 34% rise. Furthermore, customization reduces fitting errors by 30% and enhances patient comfort by 40%, significantly improving user satisfaction rates. Government subsidies covering up to 20% of prosthetic costs in several European countries further support adoption. This strong demand trajectory significantly boosts the Europe 3D Printed Prosthetics Market Growth.

Europe 3D Printed Prosthetics Market Restraint

Limited Standardization and Regulatory Challenges Restrict Adoption

Despite rapid advancements, lack of standardized regulations and certification frameworks restrains the Europe 3D Printed Prosthetics Market Growth. Around 41% of manufacturers face compliance challenges due to varying regulations across countries such as Germany, France, and Italy. Certification delays can extend product launch timelines by 6–12 months, increasing costs by nearly 18%. Additionally, only 52% of prosthetic designs meet cross-border regulatory standards, limiting scalability. Quality inconsistencies due to material variability also affect 23% of production batches, raising concerns among healthcare providers. These regulatory hurdles continue to restrict widespread adoption, impacting the Europe 3D Printed Prosthetics Market Growth.

Europe 3D Printed Prosthetics Market Opportunity

Technological Advancements in Materials and Bioprinting Create New Avenues

Emerging technologies such as bioprinting and advanced composite materials present significant opportunities for the Europe 3D Printed Prosthetics Market Growth. Investments in R&D exceeded USD 420 million in 2025, with nearly 26% allocated to material innovation. New lightweight materials have improved prosthetic durability by 35% while reducing weight by 22%. Bioprinting advancements are expected to contribute to 12% of the market by 2030, particularly in hybrid prosthetic solutions. Additionally, integration with IoT-enabled sensors, used in 19% of premium prosthetics, enhances functionality by enabling real-time feedback. These innovations are expected to drive long-term Europe 3D Printed Prosthetics Market Growth.

Challenge in Europe 3D Printed Prosthetics Market

High Initial Setup Costs and Technical Expertise Requirements

High initial investment costs and requirement for skilled professionals pose challenges for the Europe 3D Printed Prosthetics Market Growth. Setting up a 3D printing facility requires capital investment ranging between USD 150,000 and USD 500,000, limiting entry for small players. Additionally, only 38% of healthcare institutions currently have trained professionals capable of operating advanced additive manufacturing systems. Maintenance costs account for nearly 12% of annual operational expenses, while material costs contribute 28%. Training programs and workforce shortages continue to slow adoption rates, particularly in emerging European regions, thereby affecting the Europe 3D Printed Prosthetics Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 0.96 billion |

| Market Size in 2026 | USD 1.12 billion |

| Market Size in 2034 | USD 3.98 billion |

| CAGR | 17.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Prosthetics Market Segmentation

By Type

Upper limb prosthetics dominate with 46% share, producing nearly 480,000 units annually. These prosthetics incorporate multi-axis joints and sensor-based controls with accuracy rates of 92%, improving dexterity by 35%.

Lower limb prosthetics hold 38% share, with over 400,000 units produced annually. Advanced models support load-bearing capacities exceeding 120 kg and incorporate shock absorption systems improving mobility efficiency by 28%.

Cosmetic prosthetics account for 16% share, with approximately 170,000 units produced annually. These focus on aesthetic appeal with color-matching accuracy of 95% and lightweight designs under 500 grams, improving user acceptance by 22%.

By Application

Hospitals dominate with 52% share, handling over 540,000 prosthetic fittings annually. High-end devices with sensor integration account for 35% of hospital usage, improving rehabilitation outcomes by 30%.

Rehabilitation centers hold 31% share, managing approximately 325,000 fittings annually. These centers focus on training and adjustment, with patient retention rates exceeding 78% due to improved comfort and usability.

Home care accounts for 17% share, with around 180,000 units used annually. Portable and user-friendly prosthetics with modular components have increased home adoption by 24%, supporting long-term patient independence.

Europe 3D Printed Prosthetics Market Segmentations

By Type

- Upper Limb Prosthetics

- Lower Limb Prosthetics

- Cosmetic Prosthetics

By Application

- Hospitals

- Rehabilitation Centers

- Home Care

Country Insights

United Kingdom

The UK leads with 28% share, producing over 310,000 units annually. Advanced technology adoption and government funding drive innovation, particularly in pediatric prosthetics (21% share).

Germany

Germany holds 22% share, producing 240,000 units annually. Strong industrial infrastructure and R&D investments exceeding USD 180 million annually support growth.

France

France accounts for 16% share, with 175,000 units produced annually. Increasing healthcare expenditure and adoption rates reaching 41% boost demand.

Spain

Spain holds 12% share, producing 130,000 units annually. Government initiatives covering 18% of prosthetic costs enhance accessibility.

Italy

Italy accounts for 11% share, producing 115,000 units annually. Growing rehabilitation centers (up by 22%) support adoption.

Russia

Russia contributes 11% share, producing 110,000 units annually. Expansion of healthcare infrastructure drives demand growth.

Top Players n Europe 3D Printed Prosthetics Market

- Open Bionics

- Materialise NV

- Össur

- Stratasys Ltd.

- 3D Systems Corporation

- Ottobock

- Unlimited Tomorrow

- LimbForge

- Youbionic

- Protosthetics

- e-NABLE

- Exiii Inc.

Top Companies

Open Bionics

- Holds approximately 12% market share

- Strong focus on pediatric prosthetics

- Produces over 90,000 units annually

- Collaborates with healthcare institutions across 15 countries

Ottobock

- Accounts for nearly 15% market share

- Advanced sensor-enabled prosthetics

- R&D investment exceeds USD 120 million annually

- Global presence with 50+ distribution centers

Investment

Investment in the Europe 3D Printed Prosthetics Market exceeded USD 750 million in 2025, with 38% allocated to material innovation and 27% to AI-based design platforms. The UK and Germany together account for 52% of total investments, while France and Italy contribute 24%. Venture capital funding increased by 19% year-over-year, supporting over 80 startups.

M&A activity is also rising, with over 25 deals recorded in 2024–2025, focusing on technology integration and distribution expansion. Collaborations between manufacturers and healthcare providers increased by 31%, improving supply chain efficiency by 22%. These investments create strong opportunities for expansion and innovation.

New Product

New product development accounts for 34% of total market activity, with over 120 new prosthetic models launched in 2025. Innovations include sensor-enabled prosthetics with 25% improved responsiveness and lightweight materials reducing weight by 20%.

Companies are also focusing on modular designs, enabling 40% faster replacement and upgrades. AI-driven customization tools have improved fitting accuracy by 32%, enhancing user satisfaction and adoption rates.

Recent Development in Europe 3D Printed Prosthetics Market

- 2025: Open Bionics increased production by 28%, launching 3 new pediatric prosthetic models with improved durability by 35%.

- 2024: Ottobock expanded manufacturing capacity by 22%, increasing annual output by 75,000 units.

- 2024: Materialise introduced new software improving design efficiency by 30%, reducing production time by 40%.

Research Methodology for Europe 3D Printed Prosthetics Market

The research methodology for the Europe 3D Printed Prosthetics Market involves a combination of primary and secondary research approaches. Primary research includes interviews with over 120 industry experts, manufacturers, and healthcare professionals across six European countries, contributing nearly 65% of data inputs. Secondary research involves analysis of industry reports, company filings, and government publications, accounting for 35% of data validation. Market size estimation is conducted using bottom-up and top-down approaches, with production volumes, pricing trends, and adoption rates analyzed across 2022–2025. Data triangulation ensures accuracy, while statistical models are used to forecast growth trends through 2034.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.