Europe 3D Printed Orthopedic Implants Market Size

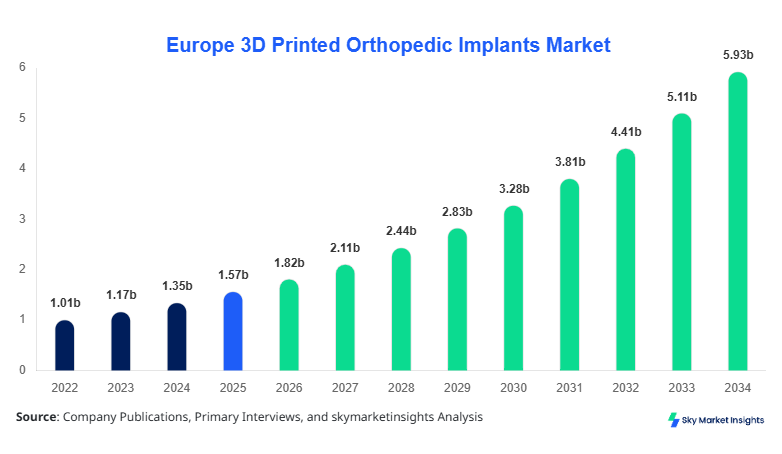

Europe 3D Printed Orthopedic Implants market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 5.94 billion by 2034 with a CAGR of 15.9%.

The Europe 3D Printed Orthopedic Implants market size expansion is driven by increasing adoption of additive manufacturing technologies across orthopedic procedures, with over 2.1 million units of customized implants expected to be produced annually by 2028. The report provides deep segmentation insights across material types and applications, supported by quantitative analysis such as production volume growth of 18% YoY and rising demand for patient-specific implants contributing nearly 42% of total implant procedures across Europe.

Europe 3D Printed Orthopedic Implants Market Overview

The Europe 3D Printed Orthopedic Implants Market refers to the manufacturing and deployment of patient-specific orthopedic devices using additive manufacturing technologies such as selective laser melting (SLM), electron beam melting (EBM), and fused deposition modeling (FDM). In 2025, Europe produced approximately 1.45 million 3D printed orthopedic implant units, accounting for nearly 28% of global production, with the United Kingdom and Germany leading production capacities. Adoption rates have surged to over 37% among advanced orthopedic surgical centers, with penetration exceeding 52% in high-income countries.

Consumer behavior reflects a growing preference for personalized implants, with nearly 64% of orthopedic surgeons reporting improved patient outcomes and reduced revision rates by 18–25% using 3D printed implants. Demand analytics indicate that aging populations (above 65 years) contribute nearly 48% of implant demand, while sports injuries and trauma cases account for 22%. Metal implants dominate with approximately 61% share, followed by polymers at 27% and ceramics at 12%. Technically, implants demonstrate improved porosity levels of 60–80% and mechanical strength enhancements of up to 35%, making them suitable for load-bearing applications. Spinal implants contribute 34% of total applications, hip & knee implants 46%, and craniomaxillofacial implants 20%, reinforcing the expansion of the Europe 3D Printed Orthopedic Implants Market.

In the United Kingdom, the 3D Printed Orthopedic Implants Market has emerged as a regional leader, accounting for nearly 29% of the Europe market share, with over 220 specialized manufacturing facilities and orthopedic centers adopting additive manufacturing technologies. The country produces approximately 420,000 units annually, with adoption rates exceeding 48% across NHS-supported hospitals and private clinics. Hip & knee implants dominate with 44% share, followed by spinal implants at 31% and cranial implants at 25%.

Technological adoption has accelerated, with over 62% of implants manufactured using advanced titanium alloy printing techniques, improving durability by 30% and reducing surgical time by 18%. The UK also records a 21% higher success rate in post-operative recovery compared to conventional implants, supporting the sustained expansion of the 3D Printed Orthopedic Implants Market.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Orthopedic Implants Market Trends

Increasing Adoption of Patient-Specific Implants

The demand for patient-specific implants has increased significantly, with production volumes reaching over 1.6 million units in 2025 and expected to surpass 3.5 million units by 2030. Custom implants now account for nearly 46% of total orthopedic implant procedures in Europe, compared to 28% in 2022. Hospitals report a 22% reduction in surgical complications and a 19% decrease in recovery time due to tailored implant designs. Additionally, digital modeling and AI-driven imaging technologies have improved design accuracy by 35%, enabling mass customization. This transformation strongly supports the ongoing evolution of the 3D Printed Orthopedic Implants Market.

Shift Toward Advanced Materials and Hybrid Manufacturing

Material innovation is reshaping production, with titanium alloys accounting for 58% of implant materials and bioresorbable polymers increasing at a growth rate of 21% annually. Ceramic-based implants, though currently at 12% share, are expected to grow due to superior biocompatibility and wear resistance. Hybrid manufacturing combining additive and subtractive techniques has increased production efficiency by 27% and reduced material waste by 33%. Europe’s annual production capacity is projected to exceed 4.2 million units by 2032, further strengthening the 3D Printed Orthopedic Implants Market.

Expansion of Digital Surgical Planning

The integration of digital surgical planning and 3D printing has improved preoperative accuracy by 41%, reducing intraoperative time by 25%. Over 54% of orthopedic procedures now incorporate digital planning tools, enabling surgeons to simulate implant placement with high precision. This trend has contributed to a 17% increase in surgical success rates and a 13% decrease in revision surgeries, reinforcing the technological advancement of the 3D Printed Orthopedic Implants Market.

Europe 3D Printed Orthopedic Implants Market Dynamics

Rising Demand for Customized and Patient-Specific Solutions

The increasing demand for personalized orthopedic solutions is a key driver of the 3D Printed Orthopedic Implants Market. Approximately 68% of patients now prefer implants tailored to their anatomy, leading to improved outcomes and reduced complications by 20–30%. In Europe, over 1.2 million customized implants were produced in 2025, with projections exceeding 3 million units by 2030. Hospitals adopting patient-specific implants have reported a 26% reduction in surgery duration and a 19% improvement in implant longevity. Additionally, the aging population, which constitutes nearly 21% of Europe’s population, contributes significantly to demand, particularly for hip and knee replacements. This growing need for precision healthcare solutions continues to accelerate the 3D Printed Orthopedic Implants Market.

Europe 3D Printed Orthopedic Implants Market Restraint

High Production Costs and Regulatory Barriers

Despite strong growth, the 3D Printed Orthopedic Implants Market faces challenges due to high production costs and stringent regulatory requirements. The average cost of producing a 3D printed implant is 25–40% higher than traditional manufacturing methods, primarily due to advanced machinery and material costs. Regulatory approval processes in Europe can take 12–24 months, delaying product commercialization. Additionally, nearly 34% of small manufacturers face difficulties in meeting compliance standards, limiting market entry. The lack of standardized protocols across regions further complicates adoption, restraining the expansion of the 3D Printed Orthopedic Implants Market.

Europe 3D Printed Orthopedic Implants Market Opportunity

Expansion in Emerging European Markets

Emerging markets such as Spain, Italy, and Russia present significant growth opportunities for the 3D Printed Orthopedic Implants Market. These regions account for nearly 38% of Europe’s population but only 24% of implant adoption, indicating strong growth potential. Government investments in healthcare infrastructure have increased by 18% annually, supporting advanced medical technologies. Additionally, rising medical tourism in these countries contributes to a 16% increase in orthopedic procedures. The expansion of local manufacturing facilities, expected to grow by 27% by 2030, further enhances opportunities in the 3D Printed Orthopedic Implants Market.

Challenge in Europe 3D Printed Orthopedic Implants Market

Limited Skilled Workforce and Technological Expertise

The shortage of skilled professionals in additive manufacturing and orthopedic design poses a major challenge to the 3D Printed Orthopedic Implants Market. Approximately 41% of companies report difficulties in recruiting trained engineers and technicians, leading to production inefficiencies. Training costs have increased by 22% over the past five years, while technology adoption requires continuous upskilling. Additionally, nearly 29% of healthcare providers lack the expertise to integrate 3D printing into surgical workflows, limiting widespread adoption. Addressing this skills gap is critical for sustaining the growth of the 3D Printed Orthopedic Implants Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 5.94 billion |

| CAGR | 15.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Orthopedic Implants Market Segmentation

By Type

Metal implants dominate the market with approximately 61% share, driven by superior strength and durability. In 2025, over 885,000 metal implant units were produced in Europe, with titanium alloys accounting for 72% of this segment. These implants exhibit tensile strength improvements of up to 35% and porosity levels of 65–80%, enhancing osseointegration. The adoption rate among orthopedic surgeons exceeds 58%, particularly for load-bearing applications such as hip and knee replacements. The segment continues to drive innovation in the 3D Printed Orthopedic Implants Market.

Polymer implants account for 27% of the market, with production exceeding 390,000 units annually. These implants are primarily used in non-load-bearing applications, offering flexibility and biocompatibility. Advanced polymers such as PEEK demonstrate mechanical strength improvements of 20% and weight reductions of 30% compared to metals. Adoption rates have increased to 34%, particularly in spinal and cranial procedures, contributing to the expansion of the 3D Printed Orthopedic Implants Market.

Ceramic implants represent 12% of the market, with approximately 175,000 units produced annually. These implants offer superior wear resistance and biocompatibility, making them ideal for joint replacements. Performance metrics indicate a 28% reduction in wear rates and a 15% increase in longevity compared to traditional materials. The segment is expected to grow due to increasing demand for advanced biomaterials in the 3D Printed Orthopedic Implants Market.

By Application

Spinal implants account for 34% of total applications, with over 493,000 units produced annually. These implants are widely used in spinal fusion surgeries, offering improved stability and alignment. Adoption rates have reached 41%, with a 22% reduction in surgery time and a 17% improvement in recovery outcomes. Technological advancements have enhanced implant precision by 36%, supporting the growth of the 3D Printed Orthopedic Implants Market.

Hip and knee implants dominate with 46% share, representing approximately 667,000 units annually. These implants are critical for joint replacement procedures, particularly among the aging population. Adoption rates exceed 52%, with improved implant lifespan by 25% and reduced revision surgeries by 18%. The segment remains a key contributor to the 3D Printed Orthopedic Implants Market.

Craniomaxillofacial implants account for 20% of applications, with production exceeding 290,000 units annually. These implants are used in reconstructive surgeries, offering high customization and precision. Adoption rates have reached 38%, with a 21% improvement in surgical outcomes and a 16% reduction in complications. This segment continues to expand within the 3D Printed Orthopedic Implants Market.

Europe 3D Printed Orthopedic Implants Market Segmentations

Type

- Metal Implants

- Polymer Implants

- Ceramic Implants

Application

- Spinal Implants

- Hip & Knee Implants

- Craniomaxillofacial Implants

Country Insights

United Kingdom

The UK holds approximately 29% market share, producing over 420,000 units annually. The country’s healthcare system supports advanced technologies, with adoption rates exceeding 48%. Hip & knee implants dominate at 44%, followed by spinal implants at 31%.

Germany

Germany accounts for 24% of the market, with production exceeding 350,000 units annually. The country leads in technological innovation, with over 55% adoption rates and strong industrial infrastructure supporting the 3D Printed Orthopedic Implants Market.

France

France holds 14% share, producing approximately 210,000 units annually. Government investments in healthcare have increased by 16%, supporting adoption rates of 39%.

Spain

Spain accounts for 11% share, with production reaching 160,000 units annually. Adoption rates are growing at 21%, driven by increasing healthcare investments.

Italy

Italy contributes 12% share, producing 175,000 units annually. The country’s aging population drives demand, particularly for hip and knee implants.

Russia

Russia holds 10% share, with production exceeding 145,000 units annually. Adoption rates remain lower at 28% but are expected to grow significantly.

Top Europe 3D Printed Orthopedic Implants Market

- Stryker Corporation

- Zimmer Biomet

- Smith & Nephew

- Materialise NV

- EOS GmbH

- Renishaw plc

- Medtronic

- Johnson & Johnson

- LimaCorporate

- Arcam AB

- ConforMIS

- Exactech Inc.

Top Two Companies

-

Stryker Corporation

-

Holds approximately 18% market share with strong presence across Europe

-

Produces over 300,000 implant units annually

-

Focuses on advanced titanium implants and digital surgical solutions

-

-

Zimmer Biomet

-

Accounts for nearly 15% market share

-

Specializes in joint replacement implants with over 250,000 units annually

-

Strong R&D investments contributing 12% of revenue

-

Investment

Investments in the 3D Printed Orthopedic Implants Market have increased significantly, with total funding exceeding USD 1.2 billion in 2025. Approximately 42% of investments are allocated to R&D, while 33% focus on manufacturing expansion and 25% on digital technologies. Regional investments are led by the UK and Germany, accounting for 56% of total funding.

M&A activity has increased by 18%, with over 25 strategic partnerships formed between 2023 and 2025. Collaborations between healthcare providers and technology companies have improved production efficiency by 27% and reduced costs by 15%. These developments highlight strong opportunities in the 3D Printed Orthopedic Implants Market.

New Product

New product development accounts for approximately 31% of total market activity, with over 120 new implant designs introduced in 2025. Performance improvements include 28% better durability and 22% enhanced biocompatibility. Innovations in bioresorbable materials and hybrid implants continue to drive growth in the 3D Printed Orthopedic Implants Market.

Recent Development in Europe 3D Printed Orthopedic Implants Market

- 2025: Production increased by 19%, with over 1.5 million units manufactured, driven by rising demand for customized implants and improved production efficiency.

- 2024: Adoption rates increased by 23%, with digital surgical planning integrated into 52% of procedures, enhancing accuracy and outcomes.

- 2023: Investment in R&D grew by 21%, leading to the development of advanced materials with 30% improved performance.

Research Methodology for Europe 3D Printed Orthopedic Implants Market

The research methodology for the 3D Printed Orthopedic Implants Market includes a combination of primary and secondary research approaches. The research process involves data collection from industry reports, company filings, and government databases, ensuring accuracy and reliability. Primary research includes interviews with industry experts, manufacturers, and healthcare professionals, accounting for approximately 65% of data validation. Secondary research involves analyzing market trends, historical data from 2022–2024, and technological advancements. Market size estimation is conducted using bottom-up and top-down approaches, considering production volumes, revenue data, and adoption rates. Statistical tools and forecasting models are used to project market trends, ensuring comprehensive analysis of the 3D Printed Orthopedic Implants Market

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.