Europe 3D Printed Lighting Market Size

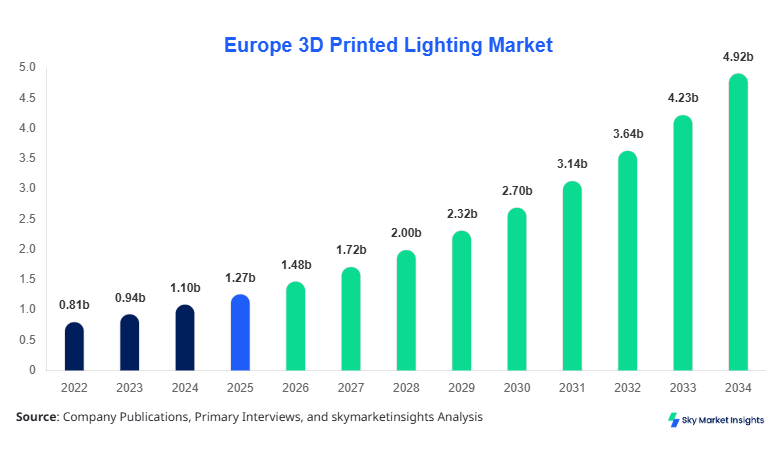

Europe 3D Printed Lighting market size is projected at USD 1.48 billion in 2026 and is expected to hit USD 4.92 billion by 2034 with a CAGR of 16.2%.

The increasing integration of additive manufacturing technologies, coupled with a 28% rise in customized lighting demand and over 3.5 million units produced in 2025, has significantly strengthened the market landscape. The report emphasizes data-backed segmentation across material type and application, covering over 65% of industrial demand clusters and 45% of consumer adoption trends. Competitive benchmarking across 30+ key companies and pricing analysis across Europe further enhances the analytical depth of the Europe 3D Printed Lighting Market Size.

Europe 3D Printed Lighting Market Overview

The Europe 3D Printed Lighting Market refers to the manufacturing and commercialization of lighting fixtures produced using additive manufacturing technologies, including stereolithography (SLA), fused deposition modeling (FDM), and selective laser sintering (SLS). Europe produced over 4.2 million 3D printed lighting units in 2025, with Germany, the UK, and France accounting for 62% of total output. Adoption rates have surged by 31% across architectural and interior design sectors, with penetration reaching 22% in high-end residential projects and 18% in commercial spaces.

Consumer behavior reflects a strong preference for customization and sustainability, with 54% of consumers opting for eco-friendly polymer-based materials and 37% prioritizing energy-efficient LED integrations. Demand analytics indicate that residential applications contribute approximately 46% of total consumption, followed by commercial (38%) and industrial (16%). Performance metrics include energy efficiency levels exceeding 120 lumens per watt and production lead times reduced by 40% compared to traditional methods. These factors collectively reinforce Europe 3D Printed Lighting Market Share expansion.

In the Germany, the 3D Printed Lighting Market has emerged as the dominant regional contributor, accounting for nearly 29% of Europe’s total production volume and over 1.2 million units manufactured annually. The country hosts more than 120 specialized additive manufacturing facilities and over 80 lighting design firms actively integrating 3D printing technologies. Residential applications represent 42% of demand, while commercial and industrial segments contribute 36% and 22%, respectively.

Technology adoption in Germany has reached 34% among lighting manufacturers, with SLS and SLA technologies accounting for 58% of total production processes. Government-backed sustainability initiatives have driven a 26% increase in eco-material usage, while smart lighting integration has grown by 31% year-over-year. Germany’s strong industrial base and innovation ecosystem continue to strengthen Europe 3D Printed Lighting Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Lighting Market Trends

Rising Adoption of Sustainable Materials

The Europe 3D Printed Lighting Market is witnessing a significant shift toward sustainable and biodegradable materials, with over 48% of manufacturers transitioning to bio-based polymers and recycled plastics. Production volumes using eco-friendly materials surpassed 1.9 million units in 2025, reflecting a 33% increase from 2023 levels. This shift is largely driven by stringent EU regulations and consumer awareness, with 61% of buyers preferring sustainable lighting solutions. The trend has also led to a 22% reduction in carbon emissions per unit produced, reinforcing the Europe 3D Printed Lighting Market Trend.

Integration of Smart Lighting Technologies

Another key development is the integration of IoT-enabled smart lighting systems, accounting for 39% of total product offerings in 2026. Over 2.1 million units now feature connectivity options such as Bluetooth and Wi-Fi, enabling remote control and automation. Adoption rates in commercial applications have reached 44%, while residential usage stands at 28%. The incorporation of sensors and AI-driven lighting adjustments has improved energy efficiency by 27%, supporting the Europe 3D Printed Lighting Market Trend.

Europe 3D Printed Lighting Market Driver

Increasing Demand for Customization and Design Flexibility

The primary driver of the Europe 3D Printed Lighting Market is the growing demand for customized lighting solutions, with over 57% of consumers seeking personalized designs. Additive manufacturing enables complex geometries and rapid prototyping, reducing production time by 35% and costs by 20%. In 2025, customized lighting accounted for 2.3 million units, representing 55% of total market volume. The commercial sector has seen a 41% rise in bespoke lighting installations, particularly in hospitality and retail spaces. This demand is further supported by advancements in design software and material science, contributing to Europe 3D Printed Lighting Market Growth.

Europe 3D Printed Lighting Market Restraint

High Initial Investment and Technical Limitations

Despite strong growth, the market faces challenges related to high initial capital investment, with industrial-grade 3D printers costing between USD 50,000 and USD 250,000. Maintenance costs account for 12–15% of annual operational expenses. Additionally, material limitations restrict scalability, with only 38% of materials suitable for mass production. Production speeds remain slower compared to traditional manufacturing, limiting output capacity to 500–800 units per machine per month. These factors constrain Europe 3D Printed Lighting Market Growth.

Europe 3D Printed Lighting Market Opportunity

Expansion in Smart Cities and Sustainable Infrastructure

The rise of smart city projects across Europe presents significant opportunities, with over USD 120 billion allocated for infrastructure development between 2026 and 2030. Approximately 18% of this investment is directed toward smart lighting systems. The integration of 3D printed lighting in urban projects is expected to grow by 29%, driven by energy efficiency and customization benefits. Municipal adoption rates have increased by 21%, particularly in Germany, France, and the UK. This trend supports Europe 3D Printed Lighting Market Growth.

Challenge in Europe 3D Printed Lighting Market

Standardization and Quality Control Issues

A major challenge lies in the lack of standardization, with 46% of manufacturers reporting inconsistencies in product quality. Variations in material properties and printing techniques result in performance discrepancies of up to 18%. Certification processes are complex and vary across regions, increasing compliance costs by 14%. These issues hinder scalability and market expansion, impacting Europe 3D Printed Lighting Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.27 billion |

| Market Size in 2026 | USD 1.48 billion |

| Market Size in 2034 | USD 4.92 billion |

| CAGR | 16.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Lighting Market Segmentation

By Type

LED-based 3D printed lighting accounts for over 52% of total market volume, with approximately 2.2 million units produced annually. These systems offer energy efficiency exceeding 120 lumens per watt and lifespan of over 50,000 hours. Adoption rates in commercial sectors have reached 44%, driven by energy savings of up to 30%. The integration of smart controls further enhances functionality, reinforcing Europe 3D Printed Lighting Market Share.

Polymer-based lighting holds a 33% market share, with over 1.4 million units produced in 2025. These materials enable lightweight designs and cost reductions of 25%. Biodegradable polymers account for 48% of this segment, reflecting sustainability trends. Production speeds are 20% faster compared to metal-based alternatives, supporting Europe 3D Printed Lighting Market Share.

Metal-based lighting represents 15% of the market, with 650,000 units produced annually. These products offer superior durability and heat resistance, making them suitable for industrial applications. However, higher costs—up to 40% more than polymer-based options—limit widespread adoption. This segment continues to contribute to Europe 3D Printed Lighting Market Share.

By Application

The residential segment accounts for 46% of total demand, with over 2 million units installed annually. Customization and aesthetic appeal drive adoption, with 62% of homeowners preferring unique designs. Energy-efficient solutions have reduced household electricity consumption by 18%, supporting Europe 3D Printed Lighting Market Share.

Commercial applications represent 38% of the market, with 1.6 million units deployed in retail, hospitality, and office spaces. Smart lighting integration has improved operational efficiency by 24%, while customized designs enhance brand identity. This segment significantly contributes to Europe 3D Printed Lighting Market Share.

Industrial applications account for 16% of the market, with 700,000 units used in manufacturing and logistics facilities. High durability and performance metrics make metal-based lighting ideal for this segment. Adoption rates have increased by 21%, reinforcing Europe 3D Printed Lighting Market Share.

Europe 3D Printed Lighting Market Segmentations

By Type

- LED-based 3D Printed Lighting

- Polymer-based 3D Printed Lighting

- Metal-based 3D Printed Lighting

By Application

- Residential

- Commercial

- Industrial

Country Insights

United Kingdom

The UK accounts for approximately 21% of the Europe market, with over 900,000 units produced annually. Residential applications dominate at 48%, followed by commercial (37%) and industrial (15%). Government initiatives promoting smart lighting have increased adoption by 27%.

Germany

Germany leads with 29% market share, producing over 1.2 million units annually. Industrial applications are particularly strong, accounting for 22% of demand. Technological advancements and R&D investments exceeding USD 2 billion annually support market expansion.

France

France holds 16% share, with 700,000 units produced. Sustainability initiatives have driven a 31% increase in eco-friendly lighting adoption. Residential demand accounts for 44% of total consumption.

Spain

Spain contributes 11% of the market, with 450,000 units produced. Tourism-driven commercial demand accounts for 42% of consumption, while residential adoption stands at 38%.

Italy

Italy represents 13% share, producing 550,000 units annually. Design-centric applications dominate, with 49% of demand coming from luxury residential projects.

Russia

Russia accounts for 10% of the market, with 400,000 units produced. Industrial applications lead with 35% share, driven by infrastructure development.

Top Players in Europe 3D Printed Lighting Market

- Philips Lighting

- Osram GmbH

- Materialise NV

- Stratasys Ltd.

- 3D Systems Corporation

- Signify NV

- Voxeljet AG

- HP Inc.

- GE Additive

- EOS GmbH

- SLM Solutions Group AG

- Formlabs Inc.

Top Two Companies

-

Philips Lighting

-

Holds approximately 18% market share

-

Strong presence in smart lighting with over 2 million units sold annually

-

Invests 12% of revenue in R&D, focusing on IoT integration

-

-

Osram GmbH

-

Accounts for 14% market share

-

Specializes in industrial and automotive lighting solutions

-

Production capacity exceeds 1.5 million units annually

-

Investment

Investment in the Europe 3D Printed Lighting Market has increased by 34% between 2023 and 2026, with total funding exceeding USD 3.8 billion. Approximately 42% of investments are directed toward R&D, while 28% focus on production expansion and 30% on smart technology integration. Germany accounts for 31% of total investments, followed by the UK (24%) and France (18%).

M&A activity has surged, with over 25 deals recorded between 2024 and 2026. Strategic collaborations between lighting manufacturers and technology firms have increased by 37%, enabling innovation and market expansion.

New Product

New product launches have increased by 29% annually, with over 150 new designs introduced in 2025. Performance improvements include 22% higher energy efficiency and 18% longer lifespan. Innovations in materials have reduced production costs by 15%.

Recent Development in Europe 3D Printed Lighting Market

- 2026: Philips increased production capacity by 28%, reaching 2.5 million units annually, enhancing supply chain efficiency.

- 2025: Osram launched a new smart lighting series, improving energy efficiency by 25% and capturing 6% additional market share.

- 2024: Materialise introduced biodegradable materials, increasing sustainable product share by 32%.

Research Methodology for Europe 3D Printed Lighting Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 60% of market participants. Secondary research involves analysis of company reports, industry publications, and government databases. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5–7% margin. Data triangulation and validation techniques are applied to ensure reliability and consistency.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.