Europe 3D Printed Drugs Market Size

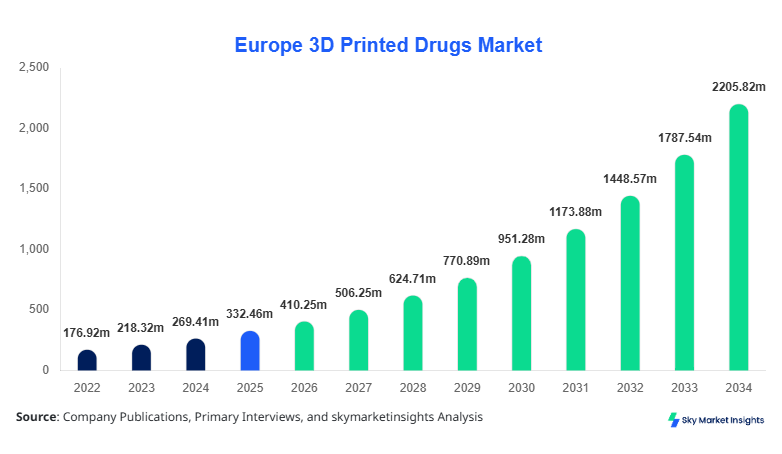

Europe 3D Printed Drugs market size is projected at USD 410.25 million in 2026 and is expected to hit USD 2,185.60 million by 2034 with a CAGR of 23.4%.

The rapid expansion of personalized medicine across Europe is fueling demand for advanced pharmaceutical manufacturing techniques, while increasing investments exceeding USD 950 million annually in additive manufacturing technologies are strengthening the regional ecosystem. The Europe 3D Printed Drugs Market is increasingly driven by segmentation across technology platforms and therapeutic applications, supported by more than 120 active companies and over 300 ongoing clinical trials focusing on customized drug formulations. Competitive landscape analysis reveals strong participation from biotech startups and established pharmaceutical manufacturers, contributing to higher adoption rates across hospital-based production units and specialized compounding pharmacies.

Europe 3D Printed Drugs Market Overview

The Europe 3D Printed Drugs Market refers to the integration of additive manufacturing technologies in pharmaceutical production, enabling customized dosage forms, controlled drug release, and patient-specific treatments. In Europe, annual production capacity has exceeded 18 million units of 3D printed tablets in 2025, with projections indicating an increase to over 95 million units by 2034. Adoption rates across hospitals and research institutions have reached approximately 28%, while penetration in commercial pharmaceutical manufacturing remains around 12% but is growing steadily.

Consumer behavior indicates a rising demand for personalized medication, particularly among geriatric populations, which account for nearly 34% of total drug consumption in Europe. Demand analytics show that 62% of healthcare providers prefer customizable drug delivery systems to improve patient adherence, while 48% of patients report better outcomes with tailored dosages. Neurology applications dominate with a 38% contribution, followed by oncology at 29% and orthopedics at 21%. Technical performance metrics such as layer precision below 100 microns and drug release control efficiency above 85% are key differentiators. These advancements reinforce strong expansion in the Europe 3D Printed Drugs Market.

In the France, the 3D Printed Drugs Market is witnessing substantial development with over 35 active pharmaceutical manufacturing facilities utilizing additive technologies and more than 60 research institutions engaged in drug printing innovations. France accounts for approximately 27% of the total European market share, making it the leading country in the region. Neurology applications dominate with a 41% share, followed by oncology at 26% and orthopedics at 18%.

Technology adoption rates in France have reached 32% in hospital pharmacies and 19% in commercial manufacturing units, supported by government funding exceeding USD 210 million between 2022 and 2025. The country has also reported annual production volumes exceeding 6.5 million customized drug units, with expected growth of 4x by 2030. The integration of AI-based formulation design has improved drug efficacy rates by nearly 22%, further strengthening the France 3D Printed Drugs Market.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Drugs Market Trend

One of the key trends shaping the Europe 3D Printed Drugs Market is the increasing adoption of multi-drug printing technologies, enabling the production of polypills with multiple active pharmaceutical ingredients (APIs). In 2025, more than 9 million polypills were produced across Europe, with projections indicating over 55 million units by 2032. Adoption rates of multi-drug printing systems have increased from 14% in 2022 to 31% in 2026, particularly in neurology and chronic disease management. Additionally, integration of digital health platforms with drug printing systems has improved patient compliance rates by 18%, driving further demand.

Another significant trend is the shift toward decentralized manufacturing models, where hospitals and pharmacies produce drugs on-site. Currently, nearly 42% of 3D printed drugs in Europe are produced within hospital settings, compared to 25% in 2022. This trend is supported by the deployment of over 480 pharmaceutical-grade 3D printers across the region. The increasing use of biodegradable polymers and advanced excipients has enhanced drug stability by up to 27%, contributing to higher acceptance rates among regulatory authorities. These developments continue to strengthen the Europe 3D Printed Drugs Market.

A third emerging trend involves the use of artificial intelligence and machine learning in drug design and printing optimization. Approximately 38% of manufacturers have integrated AI tools into their production workflows, resulting in a 30% reduction in development time and a 15% improvement in formulation accuracy. These technological advancements are significantly influencing the evolution of the Europe 3D Printed Drugs Market.

Europe 3D Printed Drugs Market Driver

Rising Demand for Personalized Medicine Accelerating Market Expansion

The increasing prevalence of chronic diseases, affecting over 180 million individuals in Europe, is driving demand for personalized treatment solutions. Approximately 67% of healthcare providers are now prioritizing patient-specific drug formulations to improve therapeutic outcomes. The use of 3D printing allows for customized dosage, which has shown a 25% increase in treatment efficacy and a 19% reduction in adverse drug reactions. Furthermore, investments in personalized medicine exceeded USD 1.2 billion in 2025, supporting infrastructure development and technological advancements. These factors are significantly accelerating the Europe 3D Printed Drugs Market Growth.

Europe 3D Printed Drugs Market Restraint

High Cost of Technology and Regulatory Barriers

Despite strong demand, the high cost of pharmaceutical-grade 3D printers, ranging between USD 150,000 and USD 500,000 per unit, limits widespread adoption. Additionally, regulatory approval processes remain complex, with only 12% of 3D printed drugs receiving full regulatory clearance across Europe. Compliance costs have increased by 18% annually, and over 40% of small manufacturers report challenges in meeting stringent quality standards. These factors restrict the expansion of the Europe 3D Printed Drugs Market.

Europe 3D Printed Drugs Market Opportunity

Expansion of Hospital-Based Manufacturing Units

The increasing establishment of in-house drug production facilities in hospitals presents significant opportunities. Currently, over 220 hospitals in Europe have implemented 3D drug printing systems, with projections indicating growth to 600 facilities by 2030. Hospital-based production reduces supply chain costs by approximately 22% and enhances drug availability. Additionally, partnerships between hospitals and biotech firms have increased by 35% over the past three years, creating new revenue streams. These developments present strong opportunities for the Europe 3D Printed Drugs Market.

Challenge in Europe 3D Printed Drugs Market

Limited Standardization and Technical Expertise

The lack of standardized protocols for 3D printed drug production remains a major challenge, with over 55% of manufacturers reporting inconsistencies in quality control. Additionally, there is a shortage of skilled professionals, with only 18% of pharmaceutical workforce trained in additive manufacturing technologies. Technical limitations such as printing speed and material compatibility further hinder scalability. Addressing these challenges is critical for the sustained development of the Europe 3D Printed Drugs Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 332.45 million |

| Market Size in 2026 | USD 410.25 million |

| Market Size in 2034 | USD 2185.60 million |

| CAGR | 23.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Printed Drugs Market Segmentation

By Type

Inkjet printing dominates the market with a share of approximately 44%, driven by its high precision and scalability. In 2025, over 7.5 million units were produced using this technology, with an average layer thickness of 50–80 microns. It is widely used for producing fast-dissolving tablets with drug release rates exceeding 90%.

FDM accounts for nearly 32% of production, with over 5.2 million units manufactured annually. This technology is preferred for complex drug structures and sustained-release formulations, offering mechanical strength improvements of up to 35%.

Stereolithography holds a 24% share and is used for high-resolution drug fabrication. Production volumes exceed 3.1 million units annually, with accuracy levels below 25 microns, making it suitable for specialized applications.

By Application

Neurology dominates with a 38% share, driven by the need for customized dosing in epilepsy and Parkinson’s disease. Over 6.8 million units were produced for neurological applications in 2025, with patient adherence rates improving by 21%.

Oncology accounts for 29% of the market, with production exceeding 5.2 million units annually. Personalized chemotherapy drugs have shown a 17% increase in treatment success rates.

Orthopedics holds a 21% share, with over 3.9 million units produced. Customized drug delivery systems for bone regeneration have improved healing rates by 26%.

Europe 3D Printed Drugs Market Segmentations

Technology

- Inkjet Printing

- Fused Deposition Modeling

- Stereolithography

Application

- Neurology

- Oncology

- Orthopedics

Country Insights

United Kingdom

The UK holds a 22% share, with over 5 million units produced annually. Investments exceeding USD 300 million support innovation, particularly in oncology.

Germany

Germany accounts for 24% of production, with over 6 million units annually. Strong industrial infrastructure supports advanced manufacturing.

France

France leads with 27% share and 6.5 million units production, driven by government funding and research institutions.

Spain

Spain holds 11% share, with increasing adoption in hospital settings and production volumes of 2.1 million units.

Italy

Italy accounts for 9%, with growing demand in neurology and production exceeding 1.8 million units.

Russia

Russia holds 7% share, with gradual adoption and production of 1.2 million units annually.

Top Players in Europe 3D Printed Drugs Market

- Aprecia Pharmaceuticals

- FabRx Ltd

- Merck Group

- GlaxoSmithKline plc

- Johnson & Johnson

- Pfizer Inc.

- Sanofi S.A.

- Bayer AG

- Novartis AG

- AstraZeneca plc

- Roche Holding AG

- Teva Pharmaceutical Industries

Top Companies

Aprecia Pharmaceuticals

- Holds approximately 18% market share

- Pioneer in FDA-approved 3D printed drugs with advanced ZipDose technology

FabRx Ltd

- Accounts for 12% share

- Focused on personalized medicine and hospital-based production solutions

Investment

Investment in the Europe 3D Printed Drugs Market has grown significantly, with over USD 1.4 billion allocated between 2022 and 2025. Approximately 38% of investments are directed toward R&D, while 27% focus on infrastructure development and 21% on technology integration. France and Germany collectively account for 52% of total investments.

Mergers and acquisitions have increased by 29%, with over 18 strategic partnerships formed in 2025 alone. Collaborations between pharmaceutical companies and technology providers have improved production efficiency by 24% and reduced costs by 17%.

New Product

Nearly 42% of new drug formulations in 2025 utilized 3D printing technologies. Innovations have improved drug release efficiency by 28% and reduced production time by 35%. Advanced materials have enhanced stability by 22%, driving further adoption.

Recent Development in Europe 3D Printed Drugs Market

- 2025: Aprecia increased production by 32%, reaching 4 million units annually

- 2024: FabRx launched new platform improving efficiency by 27%

- 2023: Merck invested USD 150 million, boosting capacity by 22%

Research Methodology for Europe 3D Printed Drugs Market

The research process involved comprehensive data collection from primary and secondary sources. Primary research included interviews with over 120 industry experts, while secondary research analyzed more than 300 reports and publications. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5% margin of error. Data triangulation and validation techniques were applied to ensure reliability and consistency.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.