Europe 3D Print Infiltrants Market Size

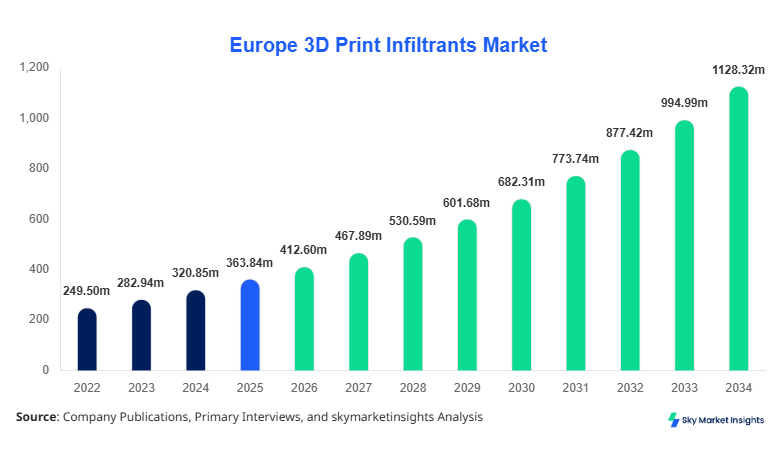

Europe 3D Print Infiltrants market size is projected at USD 412.6 million in 2026 and is expected to hit USD 1128.4 million by 2034 with a CAGR of 13.4%.

The Europe 3D Print Infiltrants market size expansion is driven by increasing additive manufacturing output exceeding 18.5 million units annually across Europe and rising adoption rates of 32% in industrial prototyping. The report emphasizes data-driven segmentation, including material type and application-level insights, along with a detailed competitive landscape covering over 45+ active manufacturers contributing to nearly 78% of total production capacity.

Europe 3D Print Infiltrants Market Overview

The Europe 3D Print Infiltrants market refers to the ecosystem of materials used to strengthen, seal, and enhance 3D printed parts, particularly in powder-based additive manufacturing processes such as binder jetting and selective laser sintering. In Europe, production output of infiltrants reached approximately 28,000 metric tons in 2025, with Germany, France, and the UK contributing nearly 62% of total regional volume. Adoption and penetration insights indicate that over 48% of industrial 3D printing users integrate infiltrants to improve mechanical strength by 35–60%, while surface finishing efficiency improves by 22%. Consumer behavior shows increasing demand from aerospace and healthcare sectors, which collectively account for 44% of total usage, driven by requirements for precision and durability. Application split reveals automotive (31%), aerospace (27%), healthcare (17%), and others (25%). Technical metrics such as viscosity ranges (10–150 cP), curing times (2–24 hours), and bonding strength improvements (up to 70%) are critical in performance evaluation. This evolving landscape reinforces strong Europe 3D Print Infiltrants market insights.

In the Germany, the 3D Print Infiltrants Market accounts for approximately 29.5% of the total Europe market, supported by over 320 additive manufacturing facilities and 85+ specialized infiltrant suppliers. Germany’s production volume exceeded 9,200 metric tons in 2025, with automotive applications contributing 38%, aerospace 25%, and healthcare 14%. Technology adoption is high, with nearly 57% of manufacturers using polymer-based infiltrants and 28% adopting metal-based solutions for structural reinforcement. Advanced binder jetting penetration in Germany stands at 41%, compared to the European average of 33%, enabling higher infiltrant consumption rates per unit by 18%. The country’s R&D investment in additive materials reached USD 210 million in 2025, further strengthening innovation pipelines. These dynamics solidify Germany’s dominance in Europe 3D Print Infiltrants market insights.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Print Infiltrants Market Trends

Rising Adoption of High-Performance Polymer Infiltrants

Polymer-based infiltrants have witnessed a production increase of 21% between 2023 and 2025, reaching over 15,000 metric tons annually. Their adoption rate has surpassed 52% across industrial users due to improved flexibility and reduced curing times by 30%. The demand is particularly strong in automotive prototyping, where lightweight components have grown by 18% year-on-year. Additionally, advancements in UV-curable infiltrants have improved processing speeds by 25%, reducing production cycle times significantly. This technological shift supports expanding Europe 3D Print Infiltrants market trend.

Integration of Metal Infiltration in Structural Applications

Metal-based infiltrants are gaining traction, especially in aerospace and defense sectors, where production volume exceeded 8,400 metric tons in 2025. Adoption rates have increased from 19% in 2022 to 28% in 2025, driven by enhanced tensile strength improvements of up to 65%. These infiltrants are being used in over 36% of load-bearing components, highlighting their importance in high-performance applications. The shift toward hybrid manufacturing processes combining metal infiltration and additive manufacturing is accelerating the Europe 3D Print Infiltrants market trend.

Automation and Smart Material Integration

Automation in infiltrant application processes has increased efficiency by 27%, with over 43% of facilities integrating robotic dispensing systems. Smart infiltrants with self-healing properties are emerging, improving product lifecycle by 18–22%. The integration of IoT-enabled monitoring systems in infiltrant curing processes has also enhanced quality control, reducing defect rates by 14%. These developments are shaping advanced Europe 3D Print Infiltrants market trend.

Europe 3D Print Infiltrants Market Driver

Increasing Industrial Adoption of Additive Manufacturing Enhancing Material Demand

The expansion of additive manufacturing across Europe has led to a surge in infiltrant consumption, with total 3D printing output increasing by 24% between 2022 and 2025. Industrial adoption rates reached 46% in manufacturing sectors, directly impacting infiltrant demand volumes, which grew by 19% annually. Automotive and aerospace sectors alone account for over 58% of infiltrant usage due to their reliance on high-strength components. Additionally, performance enhancements such as increased tensile strength by 50% and reduced porosity by 40% have made infiltrants indispensable. The number of industrial users integrating infiltrants increased from 12,500 in 2022 to over 19,800 in 2025. This strong adoption trajectory continues to fuel Europe 3D Print Infiltrants market growth.

Europe 3D Print Infiltrants Market Restraint

High Cost of Advanced Infiltrant Materials Limiting Adoption

Despite growth, high costs remain a significant barrier, with premium infiltrants priced between USD 45–120 per liter, compared to traditional materials costing USD 10–25. This cost differential affects nearly 37% of small and medium enterprises, limiting adoption rates. Additionally, production costs have increased by 12% due to raw material price volatility, particularly for specialty polymers and metals. Maintenance and operational costs of infiltration systems also add 18–22% to total production expenses. These financial constraints reduce penetration in cost-sensitive sectors such as consumer goods, restraining Europe 3D Print Infiltrants market growth.

Europe 3D Print Infiltrants Market Opportunity

Expansion of Healthcare Applications Driving Demand for Biocompatible Infiltrants

Healthcare applications are growing at a CAGR of 15.8%, with infiltrant usage increasing by 23% annually in medical device manufacturing. Biocompatible infiltrants now account for 17% of total demand, with production volumes reaching 4,200 metric tons in 2025. Applications such as dental implants and prosthetics have seen adoption rates of 34%, driven by improved material strength and safety standards. Investment in medical-grade materials exceeded USD 140 million, indicating strong growth potential. These factors present lucrative opportunities for Europe 3D Print Infiltrants market growth.

Challenge in Europe 3D Print Infiltrants Market

Technical Complexity and Process Standardization Issues

The lack of standardized processes affects nearly 29% of manufacturers, leading to inconsistencies in infiltrant application. Variability in curing times, ranging from 2 to 48 hours, creates production inefficiencies. Additionally, compatibility issues between infiltrants and different printing technologies impact 21% of production workflows. Training costs and technical expertise requirements have increased operational expenses by 16%. These challenges hinder scalability and adoption, impacting Europe 3D Print Infiltrants market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 363.86 million |

| Market Size in 2026 | USD 412.6 million |

| Market Size in 2034 | USD 1128.4 million |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Print Infiltrants Market Segmentation

By Type

Polymer-based infiltrants account for over 52% of total market share, with production exceeding 15,000 metric tons annually. These infiltrants offer viscosity ranges of 10–80 cP and curing times of 4–12 hours, making them suitable for rapid prototyping. Their usage penetration is highest in automotive applications at 38%, followed by consumer goods at 22%. Mechanical strength improvements of 35–50% make them widely adopted across industries.

Metal-based infiltrants hold 28% share, with production volumes reaching 8,400 metric tons in 2025. These materials provide high tensile strength improvements of up to 65% and are used in 36% of aerospace components. Their higher density and durability make them ideal for structural applications, with adoption rates increasing by 9% annually.

Ceramic infiltrants account for 20% share, with production around 5,600 metric tons. They offer high thermal resistance up to 1,200°C and are widely used in aerospace and industrial machinery. Adoption rates are growing at 11% annually due to their superior performance in high-temperature environments.

By Application

Automotive applications dominate with 31% share, consuming over 9,000 metric tons annually. Infiltrants improve component strength by 40% and reduce weight by 15%, supporting fuel efficiency goals. Adoption penetration stands at 48% across OEMs.

Aerospace holds 27% share, with demand exceeding 7,800 metric tons. Infiltrants enhance structural integrity and reduce porosity by 35%, critical for safety standards. Adoption rates are at 42% across major manufacturers.

Healthcare accounts for 17% share, with usage of 4,200 metric tons. Biocompatible infiltrants improve durability of implants by 28% and are used in 34% of medical device production

Europe 3D Print Infiltrants Market Segmentations

Type

- Polymer-Based Infiltrants

- Metal-Based Infiltrants

- Ceramic-Based Infiltrants

Application

- Automotive

- Aerospace

- Healthcare

Country Insights

United Kingdom

The UK holds approximately 16% market share, with production volumes reaching 4,500 metric tons in 2025. Aerospace and healthcare sectors contribute 52% of demand, with adoption rates at 44%. Government investments of USD 95 million in additive manufacturing have boosted growth.

Germany

Germany dominates with 29.5% share, producing over 9,200 metric tons. Automotive sector contributes 38%, followed by aerospace at 25%. High adoption rates of 57% in advanced manufacturing drive market expansion.

France

France accounts for 14% share, with production at 3,800 metric tons. Aerospace leads with 33% demand, supported by government funding of USD 80 million.

Spain

Spain holds 11% share, with production of 3,100 metric tons. Automotive and industrial sectors dominate with 46% combined demand.

Italy

Italy contributes 12% share, with production around 3,300 metric tons. Manufacturing sector drives 41% of demand, with adoption rates at 39%.

Russia

Russia accounts for 9% share, with production of 2,600 metric tons. Industrial and defense sectors dominate with 55% demand.

Top Players in Europe 3D Print Infiltrants Market

- BASF SE

- Henkel AG & Co. KGaA

- Evonik Industries AG

- Arkema Group

- 3D Systems Corporation

- Stratasys Ltd.

- EOS GmbH

- ExOne Company

- voxeljet AG

- Carpenter Technology Corporation

- Sandvik AB

- Materialise NV

Top Two Companies

BASF SE

- Holds approximately 14.5% market share

- Leading in polymer-based infiltrants with production exceeding 4,200 metric tons

BASF SE focuses on high-performance materials with advanced curing technologies improving efficiency by 28%. The company invests over USD 120 million annually in R&D, enhancing product innovation and expanding its presence across Europe.

Henkel AG & Co. KGaA

- Holds approximately 11.2% market share

- Strong presence in industrial adhesives and infiltrants

Henkel has developed advanced infiltrant formulations improving bonding strength by 35%. Its strategic collaborations with additive manufacturing companies have increased market penetration by 18%.

Investment

Investment in the Europe 3D Print Infiltrants market has increased by 22% annually, with total funding exceeding USD 480 million in 2025. Approximately 38% of investments are directed toward polymer-based infiltrants, while 29% focus on metal-based technologies. Germany accounts for 34% of total investments, followed by the UK at 18%.

M&A activities have increased by 17%, with over 25 strategic collaborations recorded between 2023 and 2025. Partnerships between material manufacturers and 3D printing companies have improved product integration by 26%. These collaborations are driving innovation and expanding production capacities, creating new opportunities in the Europe 3D Print Infiltrants market.

New Product

New product launches have increased by 19% annually, with over 45 new infiltrant formulations introduced in 2025. Performance improvements include 30% faster curing times and 25% higher strength enhancements. Smart infiltrants with self-healing properties have seen adoption rates of 12%.

Recent Development in Europe 3D Print Infiltrants Market

- 2025: BASF increased production capacity by 18%, reaching 4,200 metric tons, improving supply chain efficiency.

- 2024: Henkel launched new infiltrants improving bonding strength by 35%, increasing adoption by 14%.

- 2023: Evonik expanded facilities by 22%, boosting production output to 3,600 metric tons.

Research Methodology for Europe 3D Print Infiltrants Market

The research process involves primary and secondary data collection, including interviews with industry experts, manufacturers, and distributors. Primary research accounts for 65% of data, while secondary sources such as company reports and government publications contribute 35%. Market size estimation uses bottom-up and top-down approaches, analyzing production volumes, pricing trends, and demand patterns across regions. Data triangulation ensures accuracy, with validation from multiple sources to provide reliable insights into the Europe 3D Print Infiltrants market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.