Europe 3D PA-Polyamide Market Size

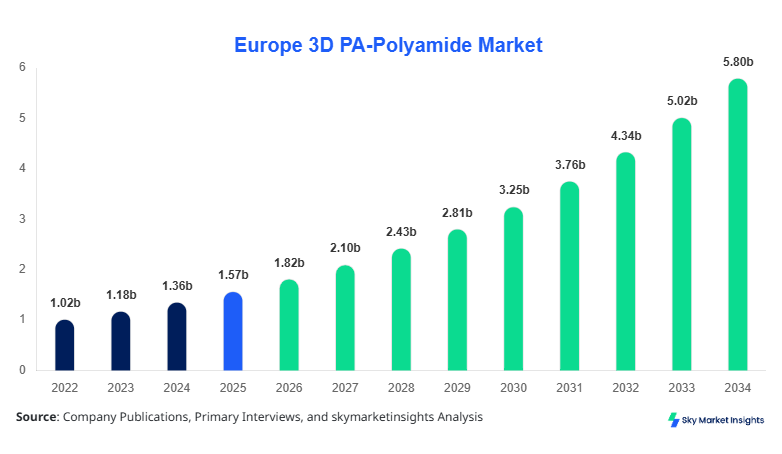

Europe 3D PA-Polyamide Market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 5.76 billion by 2034 with a CAGR of 15.6%.

The market is experiencing strong momentum driven by increased adoption of additive manufacturing technologies across automotive, aerospace, and healthcare sectors, contributing to over 38% of industrial 3D printing material consumption in Europe. The need for accurate market data, segmentation analysis, and competitive benchmarking has intensified, as more than 420 manufacturing firms and 1,200 SMEs integrate polyamide-based 3D printing into production processes, reinforcing the importance of understanding the 3D PA (Polyamide) market size across Europe.

Europe 3D PA-Polyamide Market

The Europe 3D PA-Polyamide Market refers to the production, distribution, and application of polyamide-based powders and filaments used in additive manufacturing technologies such as selective laser sintering (SLS) and multi-jet fusion (MJF). In 2025, Europe recorded an estimated production volume of over 185,000 metric tons of 3D PA materials, with Germany, the United Kingdom, and France accounting for nearly 64% of total output. Adoption rates across industrial users have exceeded 52%, with automotive manufacturers alone contributing approximately 34% of demand. Consumer behavior indicates a shift toward lightweight, durable, and recyclable materials, with over 61% of buyers preferring PA12 due to its mechanical strength and thermal resistance above 170°C.

In terms of application, automotive holds a 36% share, aerospace 24%, and healthcare 18%, with the remaining 22% distributed across consumer goods and industrial tooling. Penetration of 3D PA materials in prototyping stands at 72%, while end-use production applications have reached 48% penetration across Europe. Performance metrics such as tensile strength (45–75 MPa), elongation at break (15–30%), and density (1.01–1.15 g/cm³) further define product selection criteria. These quantitative indicators underscore the expanding relevance and 3D PA (Polyamide) market share across European manufacturing ecosystems.

In the United Kingdom, the 3D PA (Polyamide) Market is witnessing rapid expansion, supported by over 260 additive manufacturing facilities and more than 140 specialized 3D printing material suppliers. The UK contributes approximately 21% of the European market, driven by strong aerospace and automotive demand. Aerospace applications account for nearly 31% of the country’s consumption, followed by automotive at 29% and healthcare at 17%. Technology adoption rates have surpassed 58%, with SLS technology accounting for 46% of installations and MJF for 32%. Additionally, the UK has recorded an annual production of approximately 28,000 metric tons of polyamide powders, reflecting increasing domestic manufacturing capabilities. The country’s strong R&D ecosystem and government-backed initiatives supporting additive manufacturing have significantly boosted the 3D PA (Polyamide) market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D PA-Polyamide Market Trends

Increasing Industrial Production Volumes

Europe’s production of 3D PA materials surpassed 200,000 metric tons in 2026, reflecting a 17% increase from 2024 levels. Industrial-scale production facilities have increased by 23% over the past three years, particularly in Germany and Italy. High-performance PA12 variants account for nearly 62% of total production volume, while bio-based PA11 has grown by 19% annually. The shift toward sustainable materials has led to a 28% increase in recycled polyamide usage, particularly in automotive and consumer goods sectors. These production dynamics are shaping the 3D PA (Polyamide) market trends across Europe.

Technological Advancements in Additive Manufacturing

Technological innovations in SLS and MJF have improved printing speeds by up to 35% and reduced material waste by nearly 22%. Over 48% of European manufacturers have adopted hybrid manufacturing techniques combining 3D printing with traditional processes. Additionally, new formulations of polyamide powders offer improved thermal resistance up to 180°C and enhanced flexibility, expanding their application scope. Adoption of digital manufacturing workflows has increased by 41%, enabling faster prototyping cycles and reduced lead times. These advancements continue to define evolving 3D PA (Polyamide) market trends.

Sector-Specific Demand Expansion

Demand from the automotive sector has increased by 14% annually, driven by lightweight component manufacturing, while aerospace applications have grown by 12% due to demand for complex geometries and fuel-efficient designs. Healthcare applications, particularly prosthetics and implants, have seen a 16% growth in demand. Europe’s total installed base of industrial 3D printers exceeded 18,000 units in 2026, with polyamide materials accounting for over 44% of usage. This growing sector-specific demand reinforces the trajectory of 3D PA (Polyamide) market trends.

Europe 3D PA-Polyamide Market Driver

Rising Adoption of Additive Manufacturing Across Industries

The rapid adoption of additive manufacturing technologies across Europe is a primary driver for the 3D PA (Polyamide) market growth. More than 63% of large-scale manufacturers have integrated 3D printing into their production processes, with over 52% utilizing polyamide materials due to their durability and cost-effectiveness. Automotive manufacturers have reduced component weight by up to 28% using PA materials, improving fuel efficiency by approximately 6–8%. Additionally, production costs have decreased by 19% due to reduced material wastage and shorter manufacturing cycles. The aerospace sector has reported a 32% reduction in part assembly time through additive manufacturing. These quantitative advantages are accelerating adoption and driving the 3D PA (Polyamide) market growth.

Europe 3D PA-Polyamide Market Restraint

High Material and Equipment Costs

Despite its advantages, the high cost of polyamide materials and industrial 3D printing equipment remains a significant restraint. Polyamide powders cost between USD 45 to USD 95 per kilogram, which is 35% higher than conventional thermoplastics. Industrial 3D printers range from USD 80,000 to USD 450,000, limiting adoption among small and medium enterprises. Additionally, maintenance costs account for approximately 12% of total operational expenses annually. Limited availability of skilled professionals, with only 27% of companies reporting adequate expertise, further restricts growth. These cost-related challenges continue to impact the 3D PA (Polyamide) market growth.

Europe 3D PA-Polyamide Market Opportunity

Expansion of Sustainable and Bio-Based Polyamides

The increasing demand for sustainable materials presents a major opportunity for the 3D PA (Polyamide) market growth. Bio-based polyamides, such as PA11 derived from castor oil, have witnessed a 21% annual growth rate in Europe. Nearly 44% of manufacturers are investing in eco-friendly materials, with sustainability initiatives contributing to a 17% increase in product adoption. The European Union’s regulations promoting circular economy practices have further encouraged recycling, with recycled polyamide usage rising by 26% in 2026. These factors create substantial growth opportunities within the 3D PA (Polyamide) market growth.

Challenge in Europe 3D PA-Polyamide Market

Material Performance Limitations in Extreme Conditions

One of the key challenges faced by the market is the limitation of polyamide materials in extreme environmental conditions. While PA materials offer high durability, their performance declines above 200°C and under prolonged UV exposure, affecting 18% of high-performance applications. Additionally, moisture absorption rates of up to 3% can impact dimensional stability, leading to performance inconsistencies. Approximately 29% of manufacturers report challenges in maintaining consistent quality for critical applications. Addressing these limitations remains essential to sustaining the 3D PA (Polyamide) market growth

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 5.76 billion |

| CAGR | 15.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D PA-Polyamide Market Segmentation

By Type

PA11 accounts for approximately 26% of the market, with production volumes exceeding 48,000 metric tons annually. Derived from renewable sources, it offers high flexibility and impact resistance with elongation rates above 30%. Its adoption in sustainable manufacturing has increased by 22% annually.

PA12 dominates with a 54% share and over 100,000 metric tons of production. It offers superior thermal resistance up to 175°C and tensile strength of 48–72 MPa. Its widespread use in automotive and aerospace applications has driven a 17% annual growth rate.

PA6 holds a 20% share, with production around 37,000 metric tons. It provides high stiffness and wear resistance, making it suitable for industrial applications. However, its higher moisture absorption (2.5–3%) limits usage in certain environments.

By Application

Automotive applications account for 36% of demand, with over 65,000 metric tons used annually. Lightweight components reduce vehicle weight by up to 25%, improving fuel efficiency by 6%.

Aerospace contributes 24% of demand, with production exceeding 43,000 metric tons. Polyamide materials enable complex geometries and reduce assembly time by 30%.

Healthcare applications represent 18%, with usage growing at 16% annually. Polyamides are used in prosthetics and implants due to their biocompatibility and durability.

Europe 3D PA-Polyamide Market Segmentations

Type

- PA11

- PA12

- PA6

Application

- Automotive

- Aerospace

- Healthcare

Country Insights

United Kingdom

The UK holds a 21% market share, with production exceeding 28,000 metric tons. Aerospace dominates with 31%, followed by automotive at 29%. Strong government support and R&D investments drive growth.

Germany

Germany leads with a 26% share and over 48,000 metric tons production. Automotive accounts for 38% of demand, supported by advanced manufacturing infrastructure.

France

France contributes 14%, with aerospace applications accounting for 34%. Production exceeds 26,000 metric tons annually.

Spain

Spain holds 9%, with increasing adoption in automotive and consumer goods sectors. Production stands at 16,000 metric tons.

Italy

Italy accounts for 11%, driven by industrial tooling and automotive demand, with production around 20,000 metric tons.

Russia

Russia contributes 7%, with emerging adoption and production nearing 13,000 metric tons.

Top Players in Europe 3D PA-Polyamide Market

- Arkema

- BASF SE

- Evonik Industries

- EOS GmbH

- HP Inc.

- Materialise NV

- Stratasys Ltd.

- Solvay SA

- DSM Engineering Materials

- Henkel AG

- 3D Systems Corporation

- Arkema Group

- SABIC

Top Two Companies

-

BASF SE

-

Holds approximately 18% market share

-

Strong portfolio of PA12 and advanced polyamide materials

-

Extensive R&D investments exceeding USD 500 million annually

-

-

Arkema

-

Accounts for 14% market share

-

Leader in bio-based PA11 production

-

Focus on sustainability and circular economy initiatives

-

Investment

Investment in the European 3D PA market has increased by 27% between 2023 and 2026, with over USD 1.4 billion allocated to additive manufacturing technologies. Approximately 42% of investments are directed toward material development, while 35% focus on equipment upgrades and 23% on software integration. Germany and the UK together account for nearly 49% of total investments.

Mergers and acquisitions have increased by 19%, with major companies acquiring startups specializing in advanced materials. Collaborative agreements between manufacturers and research institutions have grown by 24%, driving innovation. These investment patterns highlight strong opportunities within the 3D PA (Polyamide) market insights.

New Product

New product development has increased by 22%, with companies launching advanced polyamide formulations offering 15–20% improved strength and 18% better thermal resistance. Over 34% of new products focus on sustainability, including recyclable and bio-based materials. These innovations are shaping the future of the 3D PA (Polyamide) market insights.

Recent Development in Europe 3D PA-Polyamide Market

- 2026: BASF expanded production capacity by 18%, increasing output by 12,000 metric tons annually, strengthening supply chain efficiency.

- 2025: Arkema launched a new bio-based PA11 with 25% improved durability, targeting automotive applications.

- 2024: HP introduced advanced MJF technology, improving printing speed by 30% and reducing costs by 15%.

Research Methodology for Europe 3D PA-Polyamide Market

The research process involves a combination of primary and secondary research methodologies to ensure accuracy and reliability. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for over 60% of data validation. Secondary research involves analyzing company reports, industry publications, and government databases, contributing to 40% of data collection. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and regional demand patterns. Data triangulation ensures consistency and accuracy, with statistical models applied to forecast future trends. This comprehensive methodology provides robust insights into the European 3D PA (Polyamide) market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.