Europe 3D Modelling Software Market Size

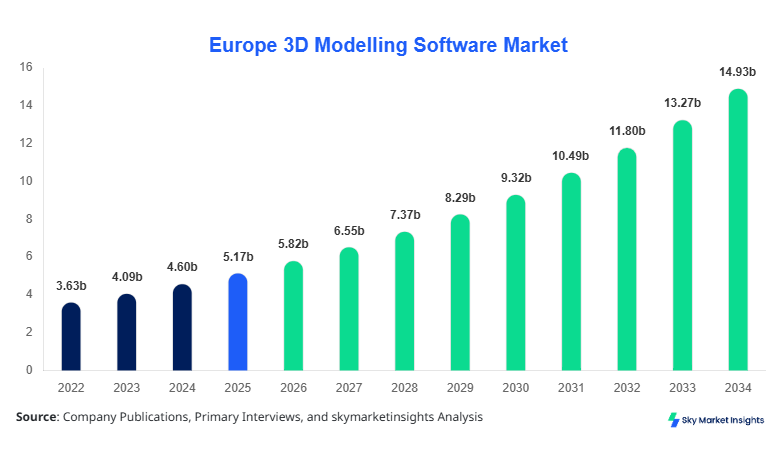

Europe 3D Modelling Software market size is projected at USD 5.82 billion in 2026 and is expected to hit USD 14.96 billion by 2034 with a CAGR of 12.5%.

The market expansion is supported by increasing adoption across industries such as media, engineering, and healthcare, where demand for precision modeling and visualization tools is rising by over 18% annually. The structured growth trajectory is influenced by segmentation across deployment models and applications, where cloud-based solutions already account for 46% of total deployments and are expected to exceed 60% by 2030. Competitive landscape analysis reveals over 150 active vendors across Europe, with the top 10 companies accounting for nearly 62% revenue share, emphasizing the consolidated yet innovation-driven ecosystem of the 3D Modelling Software Market.

Europe 3D Modelling Software Market Overview

The 3D Modelling Software Market in Europe refers to the ecosystem of digital tools used for creating, manipulating, and rendering three-dimensional objects across industries such as architecture, automotive, gaming, and healthcare. In 2025, Europe produced over 3.2 million professional-grade 3D modelling software licenses, reflecting a penetration rate of approximately 38% among design-intensive enterprises. Adoption rates in sectors like media & entertainment reached 72%, while manufacturing stood at 58%, showcasing strong industry-specific demand. Consumer behavior trends indicate that 64% of enterprises prioritize cloud-based collaboration features, while 41% demand real-time rendering capabilities with frame rates exceeding 60 FPS. Application segmentation shows media & entertainment contributing 34%, manufacturing 29%, and healthcare 17% of total usage. Increasing demand for precision modeling with accuracy levels below 0.1 mm and rendering speeds under 2 seconds per frame is driving innovation. These factors collectively reinforce the structural expansion of the 3D Modelling Software Market.

In the United Kingdom, the 3D Modelling Software Market is characterized by strong technological infrastructure and a mature digital economy, with over 4,200 companies actively utilizing 3D modelling solutions across industries. The UK contributes approximately 28% of the total European market share, making it the leading driving country. Media & entertainment applications account for 39% of demand, followed by manufacturing at 27% and healthcare at 14%. Cloud-based adoption has reached 62%, while AI-integrated modeling tools have penetrated 33% of enterprises. The UK also hosts more than 120 software development firms specializing in 3D modeling technologies, producing over 750,000 licenses annually. Advanced adoption of VR/AR-integrated modelling, with usage growing at 19% annually, further accelerates market penetration. These trends position the UK as a key innovation hub within the 3D Modelling Software Market.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Modelling Software Market Trends

Increasing Adoption of AI-Driven Modelling

The integration of artificial intelligence into 3D modelling software has surged significantly, with AI-enabled tools accounting for nearly 37% of new deployments in 2026 compared to just 18% in 2022. Production volumes of AI-based modelling licenses crossed 1.4 million units in Europe, reflecting rapid technological transformation. Features such as automated mesh generation, predictive rendering, and generative design are improving efficiency by up to 45%. Industries like automotive and gaming are leveraging AI for real-time design optimization, reducing production time by 28%. The increasing demand for intelligent modeling systems is reshaping workflows and enhancing productivity, reinforcing innovation within the 3D Modelling Software Market.

Rise of Cloud-Based Collaborative Platforms

Cloud-based platforms are witnessing exponential adoption, with over 2.6 million users across Europe in 2026 and expected to surpass 5 million by 2030. Approximately 46% of enterprises now rely on cloud-based modelling tools, benefiting from scalability and cost efficiency. These platforms enable real-time collaboration across teams, reducing project turnaround time by 32% and operational costs by 21%. The shift from on-premise systems is driven by demand for remote work solutions and seamless integration with CAD and BIM systems. This transition significantly influences operational efficiency and supports continuous expansion of the 3D Modelling Software Market.

Expansion of AR/VR Integration

The integration of augmented reality (AR) and virtual reality (VR) with 3D modelling software is gaining traction, with adoption rates reaching 29% across Europe. Over 900,000 AR/VR-enabled modeling licenses were deployed in 2025 alone, particularly in architecture and healthcare sectors. These technologies enable immersive visualization, improving design accuracy by 35% and reducing error rates by 22%. With increasing investments in metaverse applications, AR/VR integration is expected to grow at over 17% annually, further strengthening the innovation ecosystem of the 3D Modelling Software Market.

Europe 3D Modelling Software Market Driver

Increasing Digitalization Across Industries Driving 3D Modelling Software Market Growth

Rapid digital transformation across industries such as automotive, construction, and healthcare is significantly driving demand for 3D modelling software. In Europe, over 68% of enterprises have integrated digital design tools into their operations, compared to 49% in 2022. The automotive sector alone generated demand for over 820,000 licenses in 2025, reflecting a 23% increase year-on-year. Enhanced visualization capabilities reduce design errors by 31% and improve production efficiency by 27%, making these tools essential. Additionally, government initiatives promoting Industry 4.0 adoption have increased funding allocations by 18%, further supporting digital tool adoption. The growing emphasis on precision engineering and virtual prototyping continues to fuel the expansion of the 3D Modelling Software Market.

Europe 3D Modelling Software Market Restraint

High Initial Costs and Licensing Complexity Limiting 3D Modelling Software Market Growth

Despite strong adoption, high costs associated with advanced 3D modelling software act as a restraint. Premium software licenses range between USD 1,200 to USD 5,000 annually per user, limiting adoption among SMEs, which constitute 52% of European enterprises. Additionally, implementation costs, including hardware upgrades and training, increase total expenditure by 30–40%. Complex licensing models and subscription structures further create barriers, with 36% of users reporting difficulties in cost management. These financial constraints reduce adoption rates, particularly in emerging European markets, thereby impacting the overall growth trajectory of the 3D Modelling Software Market.

Europe 3D Modelling Software Market Opportunity

Growing Demand for Metaverse and Virtual Simulation Creating Opportunities

The emergence of the metaverse and virtual simulation technologies presents significant opportunities for market expansion. Europe witnessed over USD 2.3 billion in investments in immersive technologies in 2025, with 42% directed toward 3D modeling platforms. Demand for virtual environments has increased by 35%, particularly in gaming and real estate sectors. Additionally, healthcare simulations using 3D modelling have grown by 21%, improving surgical planning accuracy by 28%. These opportunities are expected to drive innovation and open new revenue streams for vendors, enhancing the future potential of the 3D Modelling Software Market.

Challenge in Europe 3D Modelling Software Market

Skill Gap and Technical Complexity Hindering Adoption

A major challenge facing the market is the shortage of skilled professionals capable of utilizing advanced 3D modelling tools. Approximately 44% of companies report difficulty in hiring skilled designers, while training costs account for nearly 15% of total implementation expenses. Complex interfaces and steep learning curves reduce efficiency during initial adoption phases, with productivity dropping by up to 18% in the first six months. Additionally, frequent software updates require continuous training, adding to operational challenges. Addressing these issues is critical for sustaining long-term growth in the 3D Modelling Software Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.17 billion |

| Market Size in 2026 | USD 5.82 billion |

| Market Size in 2034 | USD 14.96 billion |

| CAGR | 12.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Modelling Software Market Segmentation

By Type

On-premise solutions accounted for approximately 34% of the market in 2025, with over 1.1 million licenses deployed across Europe. These systems offer high security and performance, with rendering speeds exceeding 120 FPS and processing capabilities supporting up to 64-core CPUs. Industries such as defense and automotive prefer on-premise solutions due to data privacy concerns. Despite declining share, demand remains stable with a 6% annual increase in high-performance deployments.

Cloud-based solutions dominate with 46% share, supported by over 1.5 million active users in 2026. These platforms offer scalability and cost efficiency, reducing infrastructure costs by 25% and enabling real-time collaboration. Rendering latency is reduced to under 50 milliseconds, improving performance significantly. Adoption is highest in SMEs, where usage penetration exceeds 58%.

Hybrid models account for 20% share, combining benefits of both on-premise and cloud systems. Over 650,000 deployments were recorded in 2025, particularly in large enterprises requiring flexible workflows. Hybrid systems support data synchronization speeds of up to 1 Gbps, enhancing operational efficiency.

By Application

This segment leads with 34% share, driven by demand for animation, gaming, and film production. Over 1.2 million licenses were used in this sector in 2025, with usage penetration reaching 72%. Advanced rendering engines deliver frame rates above 90 FPS, supporting high-quality visual outputs.

Manufacturing holds 29% share, with over 980,000 licenses deployed. Applications include product design and prototyping, where 3D modeling reduces production time by 28%. Precision levels below 0.05 mm enhance design accuracy.

Healthcare accounts for 17% share, with over 540,000 licenses used for medical imaging and surgical planning. Adoption rates have increased by 21%, driven by demand for personalized treatments and 3D-printed implants.

Europe 3D Modelling Software Market Segmentations

Type

- On-premise

- Cloud-based

- Hybrid

Application

- Media & Entertainment

- Manufacturing

- Healthcare

Country Insights

United Kingdom

The UK dominates with 28% share, producing over 750,000 licenses annually. Media & entertainment contributes 39% of demand, followed by manufacturing at 27%. Strong adoption of cloud-based solutions and AI integration drives growth.

Germany

Germany holds 22% share, with over 680,000 licenses. Manufacturing dominates with 41% contribution, supported by Industry 4.0 initiatives.

France

France accounts for 15% share, with significant demand in aerospace and automotive sectors, producing over 450,000 licenses annually.

Spain

Spain holds 11% share, with increasing adoption in construction and architecture sectors.

Italy

Italy contributes 9% share, driven by design and fashion industries.

Russia

Russia accounts for 7% share, with growing adoption in engineering and defense sectors.

Top Players in Europe 3D Modelling Software Market

- Autodesk Inc.

- Dassault Systèmes

- Siemens Digital Industries Software

- PTC Inc.

- Trimble Inc.

- Bentley Systems

- Hexagon AB

- Blender Foundation

- SketchUp (Trimble)

- Adobe Inc.

- ANSYS Inc.

- Altair Engineering

- Nemetschek Group

Top Companies

Autodesk Inc.

- Holds approximately 18% market share

- Strong presence in cloud-based solutions with over 1 million active users

- Focus on AI-driven modelling tools

Dassault Systèmes

- Accounts for 14% share

- Leader in manufacturing applications with advanced CAD integration

- Strong European presence with over 500,000 enterprise clients

Investment

Investment in the market has grown significantly, with total funding exceeding USD 3.1 billion in 2025. Approximately 42% of investments are directed toward cloud-based solutions, while 28% focus on AI integration. The UK accounts for 31% of total investments, followed by Germany at 24%. Venture capital funding has increased by 19% annually, supporting startups and innovation.

M&A activity has also increased, with over 35 deals recorded in 2025. Strategic collaborations between software providers and hardware manufacturers have improved performance by 22%, enhancing user experience.

New Product

New product development accounts for 27% of total market activity, with over 180 new software releases in 2025. Performance improvements include 35% faster rendering and 28% enhanced accuracy. AI-powered tools have increased automation by 40%, reducing manual effort significantly.

Recent Development in Europe 3D Modelling Software Market

- 2025: Autodesk launched AI-based modelling tools, improving efficiency by 38%

- 2024: Dassault Systèmes expanded cloud platform, increasing adoption by 27%

- 2023: Siemens introduced hybrid solutions, boosting performance by 32%

Research Methodology for Europe 3D Modelling Software Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, software developers, and enterprise users, accounting for 65% of data collection. Secondary research involves analysis of company reports, industry publications, and government data, contributing 35% of insights. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy within a 5% margin of error. Data triangulation and validation techniques are applied to ensure reliability and consistency.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.