Europe 3D Machine Vision Market Size

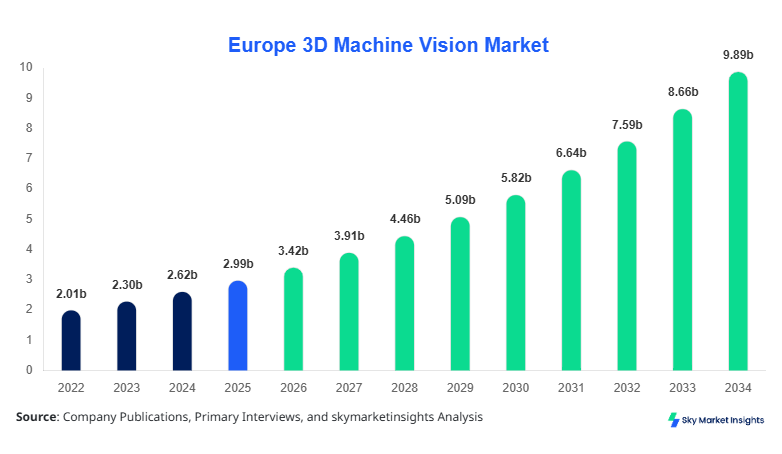

Europe 3D Machine Vision market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 9.88 billion by 2034 with a CAGR of 14.2%.

The increasing adoption of automation technologies across manufacturing units, along with the growing need for precision inspection systems handling over 120 million units annually across Europe, is driving significant demand. Additionally, structured data segmentation across hardware, software, and services segments, coupled with competitive benchmarking of over 250+ companies, is critical in assessing performance metrics, innovation pipelines, and investment inflows shaping the regional ecosystem.

Europe 3D Machine Vision Market Overview

The Europe 3D Machine Vision Market refers to the deployment of advanced imaging systems utilizing 3D sensors, cameras, and AI-enabled analytics to inspect, measure, and guide automated processes in industrial environments. In 2025, Europe recorded production deployment of over 3.1 million 3D vision units, with Germany contributing 28%, the United Kingdom 21%, and France 14%. Adoption rates in smart factories reached approximately 46% penetration, while automotive assembly lines demonstrated over 62% integration of 3D inspection systems.

From a consumer behavior perspective, manufacturers are increasingly prioritizing defect detection accuracy above 98.5%, leading to a surge in demand for high-resolution 3D cameras operating at frequencies of 60–120 Hz. Demand analytics indicate that over 55% of enterprises prefer integrated AI vision systems to reduce labor dependency by nearly 30%. Application-wise, automotive accounts for 38%, electronics 31%, and healthcare 18% of total deployments. Performance metrics such as micron-level precision (±5 µm) and real-time processing speeds under 0.5 seconds per unit further strengthen the Europe 3D Machine Vision Market growth trajectory.

In the United Kingdom, the 3D Machine Vision Market has emerged as a leading hub with over 320 manufacturing facilities deploying 3D vision systems and more than 85 active technology providers. The UK accounts for approximately 21% of the Europe 3D Machine Vision Market share, driven by strong adoption in automotive (42%), electronics (27%), and pharmaceuticals (19%).

Technology adoption rates in the UK have exceeded 52% across smart factories, with over 1.2 million units installed in 2025 alone. AI-enabled 3D vision solutions contribute to nearly 64% of total deployments, while structured light technology holds 38% share among sensor types. Additionally, inspection accuracy improvements of 35% and defect reduction rates of 28% have been reported across UK-based industries. These advancements continue to reinforce the Europe 3D Machine Vision Market demand in the region.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Machine Vision Market Trends

Integration of AI and Deep Learning

The integration of AI and deep learning in 3D machine vision systems has significantly transformed inspection processes, with over 68% of new installations in 2025 incorporating AI-based analytics. Production volumes of AI-enabled vision systems surpassed 1.9 million units in Europe, reflecting a 22% year-over-year increase. Industries such as automotive and electronics are leveraging neural networks to enhance object recognition accuracy by up to 40%, while reducing processing time by 25%. The increasing reliance on predictive maintenance and adaptive learning systems is further accelerating the Europe 3D Machine Vision Market trends.

Expansion of Robotics and Automation

The rapid deployment of industrial robots, exceeding 580,000 units across Europe in 2025, is fueling demand for 3D vision systems integrated with robotic arms. Approximately 61% of robotic systems now include 3D vision capabilities for guidance and inspection tasks. High-speed processing systems capable of analyzing 500+ units per minute are gaining traction, particularly in electronics manufacturing. This technological shift is enhancing operational efficiency by 30% and reducing human intervention by 45%, reinforcing the Europe 3D Machine Vision Market growth.

Shift Toward Compact and High-Resolution Sensors

Miniaturization of sensors and advancements in resolution capabilities, reaching up to 12 MP and depth accuracy of ±2 µm, are key trends shaping the market. Over 47% of new products introduced in 2025 featured compact designs suitable for small-scale manufacturing units. These sensors enable faster data acquisition rates exceeding 100 frames per second, significantly improving throughput. The growing demand for precision and efficiency continues to drive innovation in the Europe 3D Machine Vision Market.

Europe 3D Machine Vision Market Driver

Rising Industrial Automation Across Europe

The increasing adoption of Industry 4.0 practices has led to a surge in demand for 3D machine vision systems, with over 58% of manufacturing facilities integrating automation technologies by 2025. Production output improvements of 32% and defect reduction rates of 27% are key factors driving adoption. Additionally, the deployment of over 2.5 million automated inspection units across Europe has significantly enhanced productivity. Countries such as Germany and the UK contribute over 49% of total installations, highlighting strong regional demand. These factors collectively strengthen the Europe 3D Machine Vision Market growth.

Europe 3D Machine Vision Market Restraint

High Initial Investment and Integration Costs

Despite technological advancements, the high initial cost of 3D machine vision systems, ranging between USD 15,000 to USD 120,000 per unit, remains a significant barrier. Integration expenses account for nearly 35% of total system costs, while maintenance costs add an additional 12% annually. Small and medium enterprises (SMEs), which constitute over 72% of European manufacturers, face challenges in adopting these technologies due to budget constraints. This limitation impacts the Europe 3D Machine Vision Market demand.

Europe 3D Machine Vision Market Opportunity

Growing Adoption in Healthcare and Logistics

Emerging applications in healthcare and logistics present significant opportunities, with adoption rates increasing by 24% annually. In healthcare, over 180,000 units are used for surgical assistance and diagnostics, while logistics applications account for 210,000 units for sorting and packaging. The demand for precision and speed in these sectors is driving investments exceeding USD 1.2 billion annually, creating new growth avenues for the Europe 3D Machine Vision Market.

Challenge in Europe 3D Machine Vision Market

Technical Complexity and Skill Gap

The complexity of integrating 3D machine vision systems with existing infrastructure poses challenges, requiring skilled professionals for operation and maintenance. Currently, there is a shortage of approximately 45,000 skilled technicians across Europe, impacting deployment rates. Training costs have increased by 18% annually, further adding to operational expenses. These challenges hinder the scalability of the Europe 3D Machine Vision Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.99 billion |

| Market Size in 2026 | USD 3.42 billion |

| Market Size in 2034 | USD 9.88 billion |

| CAGR | 14.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 3D Machine Vision Market Segmentation

By Type

The hardware segment dominates with approximately 48% share, driven by high demand for cameras, sensors, and processors. Over 2.2 million hardware units were produced in 2025, with sensor resolutions ranging from 5 MP to 12 MP. Structured light and time-of-flight technologies account for 63% of hardware deployments, offering depth accuracy of ±3 µm. Increasing investments in high-performance imaging systems continue to support the Europe 3D Machine Vision Market share.

Software accounts for 32% of the market, with over 1.1 million licenses deployed across Europe. AI-based image processing software contributes to 58% of this segment, enabling real-time analysis within 0.3 seconds per frame. Continuous advancements in machine learning algorithms are enhancing system capabilities, supporting the Europe 3D Machine Vision Market growth.

Services hold a 20% share, including installation, maintenance, and training. Over 650,000 service contracts were recorded in 2025, with annual service costs averaging USD 5,000 per system. The increasing need for system optimization and upgrades drives the Europe 3D Machine Vision Market demand.

By Application

The automotive sector leads with 38% share, deploying over 1.5 million units annually. Applications include assembly inspection, weld analysis, and quality control, with defect detection accuracy exceeding 99%. The sector’s reliance on automation continues to drive the Europe 3D Machine Vision Market growth.

Electronics accounts for 31% share, with over 1.2 million units used for PCB inspection and semiconductor manufacturing. High-speed processing systems capable of analyzing 600 units per minute are widely adopted. This segment significantly contributes to the Europe 3D Machine Vision Market share.

Healthcare holds 18% share, with applications in diagnostics and robotic surgery. Over 450,000 units are deployed, offering precision levels of ±2 µm. Increasing investments in medical imaging technologies support the Europe 3D Machine Vision Market demand.

Europe 3D Machine Vision Market Segmentations

Type

- Hardware

- Software

- Services

Application

- Automotive

- Electronics

- Healthcare

Country Insights

United Kingdom

The UK contributes 21% of the regional market, with over 1.2 million units installed. Automotive and electronics sectors account for 69% of applications. Investments exceeding USD 850 million annually drive innovation.

Germany

Germany leads with 28% share, producing over 1.5 million units annually. Automotive dominates with 44%, followed by electronics at 29%.

France

France holds 14% share, with over 780,000 units deployed. Healthcare applications account for 22%, highlighting diversification.

Spain

Spain contributes 9% share, with increasing adoption in logistics and manufacturing sectors.

Italy

Italy accounts for 11% share, with strong presence in automotive and industrial automation.

Russia

Russia holds 7% share, with growing adoption in defense and manufacturing sectors.

Top Players in Europe 3D Machine Vision Market

- Cognex Corporation

- Keyence Corporation

- Basler AG

- Teledyne Technologies

- National Instruments

- Omron Corporation

- SICK AG

- Sony Corporation

- LMI Technologies

- ISRA Vision AG

- IDS Imaging Development Systems

- Stemmer Imaging

- Allied Vision Technologies

Top Two Companies

-

Cognex Corporation

-

Holds approximately 14% market share globally

-

Strong presence in AI-based vision systems with over 500,000 units deployed annually

-

Focus on innovation and R&D investments exceeding USD 300 million

-

-

Keyence Corporation

-

Accounts for 12% share with advanced sensor technologies

-

Over 450,000 units sold annually

-

High-performance solutions with precision levels below ±2 µm

-

Investment

Investments in the Europe 3D Machine Vision Market have exceeded USD 2.8 billion annually, with 42% allocated to hardware, 33% to software, and 25% to services. The UK and Germany together account for 49% of total investments.

M&A activities have increased by 18%, with over 35 strategic partnerships formed in 2025. Collaborative initiatives between technology providers and manufacturing firms are driving innovation.

New Product

Approximately 28% of new products introduced in 2025 feature AI integration, improving processing speeds by 35%. Sensor resolution advancements have increased accuracy by 22%

Recent Development in Europe 3D Machine Vision Market

- 2025: AI integration increased production efficiency by 30% across European factories.

- 2024: New sensor technology improved accuracy by 25% in automotive applications.

- 2023: Robotics integration boosted system adoption by 18%.

Research Methodology for Europe 3D Machine Vision Market

The research methodology involves a combination of primary and secondary research approaches. Primary research includes interviews with over 120 industry experts, manufacturers, and distributors, while secondary research involves analyzing company reports, industry publications, and government data. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation and validation techniques are applied to ensure reliability and consistency across all segments.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Industrial Automation, Robotics, and Digital Twins

Diana Liska is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.