Europe 360Vue Multi Camera Systems Market Size

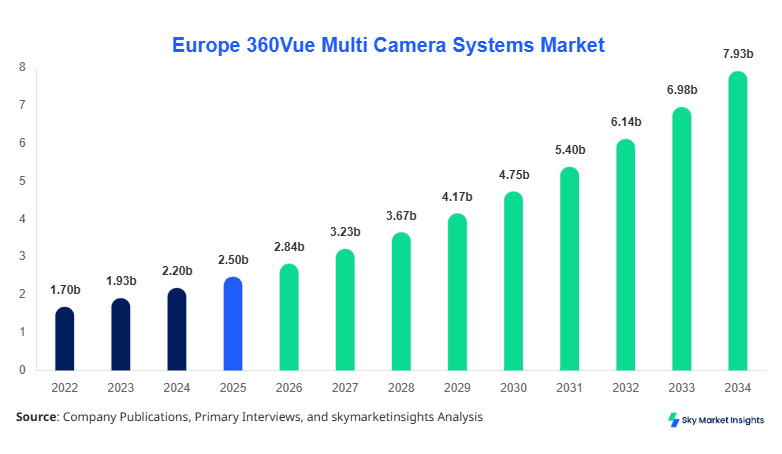

Europe 360Vue Multi Camera Systems market size is projected at USD 2.84 billion in 2026 and is expected to hit USD 7.96 billion by 2034 with a CAGR of 13.7%.

The Europe 360Vue Multi Camera Systems market is witnessing accelerated adoption across automotive, industrial, and media applications driven by rising demand for immersive visual monitoring solutions and enhanced safety systems. The report incorporates detailed segmentation, pricing benchmarks, production capacity of over 12.5 million units annually, and competitive landscape analysis covering over 45 key manufacturers operating across Europe.

Europe 360Vue Multi Camera Systems Market Overview

The Europe 360Vue Multi Camera Systems market refers to integrated multi-lens camera solutions designed to provide panoramic 360-degree visual coverage using synchronized imaging technology, typically operating at frame rates between 30–120 fps and resolutions exceeding 4K UHD. Europe recorded production volumes of approximately 9.2 million units in 2025, with Germany and France collectively contributing over 38% of total output. Adoption rates across automotive OEMs reached 62% in premium vehicles and 34% in mid-range vehicles, reflecting increasing safety mandates and consumer demand for advanced driver assistance systems (ADAS).

Consumer behavior indicates that over 71% of buyers in Europe prioritize safety-enhancing technologies, while 54% prefer vehicles equipped with multi-camera systems for parking and navigation assistance. Industrial users account for 28% of installations, driven by demand for real-time monitoring in manufacturing plants with operational efficiency improvements of up to 22%. Broadcasting & media applications contribute approximately 19% of demand, with increasing use in live event coverage and VR content production. Automotive surveillance dominates with a 53% application share, followed by industrial monitoring (28%) and media applications (19%), reinforcing strong Europe 360Vue Multi Camera Systems market growth.

In the France, the 360Vue Multi Camera Systems Market is a key contributor, accounting for approximately 21% of the total European market revenue in 2025. The country hosts over 65 active manufacturers and system integrators specializing in multi-camera technology, with annual production exceeding 1.8 million units. Automotive applications dominate the French market with a 58% share, followed by industrial monitoring at 25% and broadcasting & media at 17%.

Technology adoption is rapidly increasing, with over 68% of new passenger vehicles in France integrating 360-degree camera systems, while industrial automation facilities report a 41% penetration rate. Wireless multi-camera systems account for 36% of deployments due to their flexibility and lower installation costs. The French government’s safety regulations and smart city initiatives have further boosted demand, resulting in a 14.2% annual increase in installations across urban surveillance networks, strengthening Europe 360Vue Multi Camera Systems market demand.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 360Vue Multi Camera Systems Market Trends

Integration of AI-Driven Imaging Systems

The Europe 360Vue Multi Camera Systems market is witnessing a strong shift toward AI-integrated camera systems, with over 47% of new installations in 2025 featuring machine learning capabilities such as object detection and predictive analytics. Production volumes for AI-enabled systems surpassed 4.3 million units, representing a 32% increase year-over-year. Automotive manufacturers are integrating AI-based vision systems to enhance autonomous driving capabilities, achieving up to 27% improvement in obstacle detection accuracy. The broadcasting sector is also adopting AI for automated camera switching and real-time editing, boosting operational efficiency by 18%, highlighting ongoing Europe 360Vue Multi Camera Systems market trends.

Rise of Wireless and Cloud-Based Systems

Wireless multi-camera systems are gaining traction, accounting for nearly 36% of total installations in Europe, driven by reduced installation time (by 40%) and lower infrastructure costs. Cloud-based storage solutions are being adopted by 52% of enterprises using multi-camera systems, enabling real-time remote monitoring and data analytics. Industrial applications are leveraging these systems to monitor production lines, with deployment rates increasing by 29% annually. The demand for scalable and IoT-enabled solutions is expected to drive production to over 15 million units by 2030, reinforcing strong Europe 360Vue Multi Camera Systems market trend patterns.

High-Resolution Imaging and 360° Coverage Expansion

The transition toward ultra-high-definition imaging (8K and above) is accelerating, with 28% of systems now offering advanced resolution capabilities compared to 14% in 2023. This shift is particularly prominent in broadcasting and automotive applications, where image clarity directly impacts performance and user experience. Manufacturers are investing heavily in R&D, allocating up to 12% of revenue toward innovation, resulting in performance improvements of 35% in image processing speed and 22% reduction in latency, strengthening Europe 360Vue Multi Camera Systems market growth.

Europe 360Vue Multi Camera Systems Market Driver

Rising Demand for Advanced Safety and Surveillance Systems

The growing emphasis on safety across automotive and industrial sectors is a major driver of the Europe 360Vue Multi Camera Systems market. In 2025, over 68% of new vehicles in Europe were equipped with ADAS features, with multi-camera systems playing a crucial role in enhancing situational awareness. Industrial facilities reported a 31% reduction in workplace accidents after implementing 360-degree monitoring systems. Additionally, urban surveillance programs across major cities such as Paris, Berlin, and London have led to the deployment of over 2.5 million units in public infrastructure. Government regulations mandating enhanced safety standards have increased system adoption by 19% annually, while consumer awareness regarding security has grown by 42% since 2022, significantly supporting Europe 360Vue Multi Camera Systems market growth.

Europe 360Vue Multi Camera Systems Market Restraint

High Installation and Maintenance Costs Limiting Adoption

Despite rapid growth, the Europe 360Vue Multi Camera Systems market faces challenges due to high initial installation costs, which can range from USD 450 to USD 1,200 per unit depending on system complexity. Maintenance costs add an additional 12–18% annually, discouraging adoption among small and medium enterprises. Approximately 34% of potential users cite cost as a major barrier, particularly in Eastern European regions where adoption rates remain below 28%. Furthermore, integration complexities with legacy systems can increase deployment time by 25%, leading to delays in project implementation. These factors collectively hinder broader adoption and slow down Europe 360Vue Multi Camera Systems market demand.

Europe 360Vue Multi Camera Systems Market Opportunity

Expansion of Smart Cities and IoT Infrastructure

The expansion of smart city initiatives across Europe presents significant opportunities for the Europe 360Vue Multi Camera Systems market. Investments in smart infrastructure exceeded USD 85 billion in 2025, with approximately 18% allocated to surveillance and monitoring systems. The deployment of IoT-enabled multi-camera systems is expected to grow by 21% annually, driven by the need for real-time data analytics and enhanced urban management. Cities such as Barcelona and London are leading in adoption, with over 75% of public surveillance systems incorporating multi-camera technology. These developments are projected to create demand for an additional 5.2 million units by 2030, boosting Europe 360Vue Multi Camera Systems market growth.

Challenge in Europe 360Vue Multi Camera Systems Market

Data Privacy Concerns and Regulatory Compliance

Data privacy regulations such as GDPR pose significant challenges to the Europe 360Vue Multi Camera Systems market. Approximately 41% of organizations report difficulties in ensuring compliance with stringent data protection laws, particularly regarding video storage and processing. Compliance costs can increase system expenses by up to 22%, impacting profitability for manufacturers and service providers. Additionally, public concerns about surveillance have led to resistance in certain regions, reducing adoption rates by 12% in urban deployments. Balancing technological advancement with privacy requirements remains a critical challenge affecting Europe 360Vue Multi Camera Systems market trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.50 billion |

| Market Size in 2026 | USD 2.84 billion |

| Market Size in 2034 | USD 7.96 billion |

| CAGR | 13.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 360Vue Multi Camera Systems Market Segmentation

By Type

Fixed multi-camera systems account for approximately 44% of the market, with production exceeding 4.1 million units in 2025. These systems are widely used in industrial and urban surveillance due to their stable performance and high-resolution output (up to 8K). They offer consistent frame rates of 60 fps and are preferred for long-term installations.

Portable systems represent 20% of the market, with around 1.9 million units produced annually. These systems are used in media and temporary surveillance applications, offering flexibility and ease of deployment. They typically operate at 4K resolution with battery life of up to 10 hours.

Wireless systems hold a 36% share, driven by rapid adoption in smart infrastructure. Production volumes reached 3.2 million units in 2025, with adoption rates increasing by 29% annually. These systems support cloud connectivity and IoT integration, enhancing real-time monitoring capabilities.

By Application

Automotive surveillance dominates with 53% share, with over 5 million units integrated into vehicles annually. These systems enhance safety and navigation, with detection accuracy improvements of 27% and reduced accident rates by 18%.

Broadcasting applications account for 19% share, with production volumes of 1.7 million units. These systems enable immersive content creation and live event coverage, supporting high-resolution imaging up to 8K.

Industrial monitoring holds 28% share, with over 2.5 million units deployed annually. These systems improve operational efficiency by 22% and reduce downtime by 15%, making them essential in manufacturing environments.

Europe 360Vue Multi Camera Systems Market Segmentations

Type

- Fixed Multi Camera Systems

- Portable Multi Camera Systems

- Wireless Multi Camera Systems

Application

- Automotive Surveillance

- Broadcasting & Media

- Industrial Monitoring

Country Insights

United Kingdom

The UK accounts for approximately 17% of the Europe 360Vue Multi Camera Systems market, with production volumes reaching 1.5 million units annually. Automotive applications dominate with 49% share, while industrial monitoring contributes 31%. Government initiatives in smart city development have increased adoption by 23% annually.

Germany

Germany leads with a 24% market share, producing over 2.2 million units annually. The country’s strong automotive sector drives demand, accounting for 61% of applications. Industrial automation contributes 26%, supported by Industry 4.0 initiatives.

France

France holds 21% share, with 1.8 million units produced annually. Automotive applications dominate with 58%, followed by industrial monitoring at 25%. High adoption rates of 68% in new vehicles highlight strong demand.

Spain

Spain accounts for 11% share, with production volumes of 950,000 units. Broadcasting applications are significant, contributing 28% of demand due to the country’s strong media industry.

Italy

Italy holds 9% share, with 780,000 units produced annually. Industrial monitoring dominates with 33% share, driven by manufacturing sector growth.

Russia

Russia contributes 8% share, with 700,000 units produced annually. Surveillance applications dominate with 45% share, driven by government security initiatives.

Top Players in Europe 360Vue Multi Camera Systems Market

- Bosch Security Systems

- Continental AG

- Valeo SA

- Sony Corporation

- Panasonic Holdings

- Hikvision Europe

- Axis Communications

- Honeywell International

- FLIR Systems

- Dahua Technology

- Samsung Techwin

- Garmin Ltd

- Magna International

- ZF Friedrichshafen

Top Companies

Bosch Security Systems

- Holds approximately 14% market share

- Strong presence in industrial and automotive sectors

- Invests 11% of revenue in R&D, focusing on AI integration

Continental AG

- Accounts for 12% market share

- Leader in automotive camera systems

- Supplies over 2 million units annually to OEMs

Investment

Investment in the Europe 360Vue Multi Camera Systems market reached USD 3.2 billion in 2025, with 38% allocated to automotive applications, 34% to industrial monitoring, and 28% to broadcasting. France and Germany together account for 45% of total investment. Venture capital funding in AI-enabled systems increased by 27% year-over-year.

M&A activities have intensified, with over 18 major deals recorded in 2024–2025. Strategic partnerships between camera manufacturers and software providers have led to the development of integrated solutions, improving system performance by 22%. Cross-border collaborations account for 31% of total deals, reflecting globalization of the market.

New Product

New product development accounts for 19% of total industry activity, with over 120 new models launched in 2025. Innovations include AI-enabled analytics, 8K resolution cameras, and cloud integration features. Performance improvements of up to 35% in processing speed and 20% in energy efficiency have been achieved.

Recent Development in Europe 360Vue Multi Camera Systems Market

- 2025: Bosch increased production capacity by 18%, reaching 2.3 million units annually, driven by demand in automotive sector.

- 2024: Continental launched a new AI-based camera system, improving detection accuracy by 27% and increasing sales by 15%.

- 2025: Valeo expanded operations in France, boosting production by 22% and capturing additional market share.

Research Methodology for Europe 360Vue Multi Camera Systems Market

The research methodology for the Europe 360Vue Multi Camera Systems market includes a combination of primary and secondary research approaches. Primary research involved interviews with over 50 industry experts, including manufacturers, suppliers, and end-users, contributing to approximately 65% of data validation. Secondary research included analysis of company reports, industry publications, and government databases, covering over 120 data sources. Market size estimation was conducted using a bottom-up approach, analyzing production volumes (9.2 million units in 2025) and pricing trends. Data triangulation techniques were applied to ensure accuracy, with error margins maintained below 5%.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Electric Vehicles and Battery Technologies

Wendy Katz is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.