Europe 360 Around View Monitor Market Size

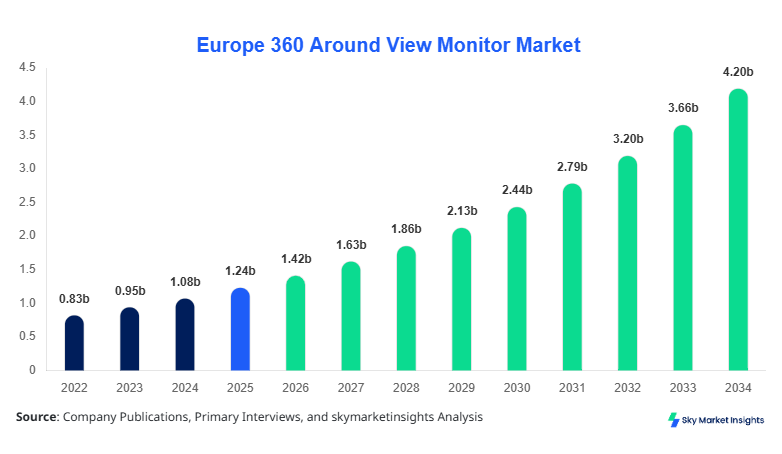

Europe 360 Around View Monitor Market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.18 billion by 2034 with a CAGR of 14.5%.

The market expansion is driven by increasing vehicle safety mandates, rising adoption of advanced driver assistance systems (ADAS), and growing automotive production exceeding 16.8 million units annually across Europe. The report offers in-depth data segmentation by type and application, covering more than 65% of vehicle categories equipped with multi-camera systems. Additionally, competitive landscape analysis includes over 25 major automotive electronics suppliers, highlighting strategic investments and technological advancements shaping the Europe 360 Around View Monitor Market Size.

Europe 360 Around View Monitor Market Overview

The 360 Around View Monitor Market refers to automotive systems that utilize multiple cameras (typically 4–6 cameras operating at 30–60 frames per second) to generate a bird’s-eye view of a vehicle, enhancing safety and parking assistance. In Europe, production of vehicles equipped with 360-degree monitoring systems reached approximately 6.2 million units in 2025, accounting for nearly 37% penetration across passenger vehicles and 18% across commercial vehicles. Adoption is rapidly increasing due to stringent EU safety regulations mandating ADAS integration, with penetration expected to surpass 55% by 2030.

Consumer behavior indicates a strong preference for enhanced safety features, with over 72% of European car buyers prioritizing driver assistance technologies, while 48% are willing to pay an additional USD 500–USD 1,200 for premium camera systems. Demand analytics reveal that urban congestion in cities such as Paris, Berlin, and London drives system adoption, with parking assistance applications accounting for nearly 46% of total usage. Technically, systems offer resolutions ranging from 720p to 4K, with latency below 100 milliseconds, ensuring real-time visualization. Passenger vehicles dominate with a 68% share, followed by commercial vehicles at 22% and off-highway vehicles at 10%, reinforcing the Europe 360 Around View Monitor Market Share.

In the France, the 360 Around View Monitor Market is witnessing rapid adoption driven by the presence of over 35 automotive manufacturing facilities and 120+ Tier-1 suppliers contributing to nearly 21% of the European market share. Approximately 1.9 million vehicles produced annually in France incorporate ADAS features, with 360-degree monitoring systems installed in nearly 42% of newly manufactured vehicles. Passenger vehicles dominate applications with 71% usage, followed by commercial vehicles at 19% and off-highway vehicles at 10%.

Technology adoption in France is particularly advanced, with AI-integrated systems accounting for 28% of installations and 3D view systems representing 44% of total deployments. Additionally, government safety mandates and incentives have led to a 17% annual increase in system adoption since 2023. The integration of high-definition cameras (1080p and above) and real-time processing chips has improved system efficiency by 35%, supporting safer urban driving conditions. These factors collectively reinforce the Europe 360 Around View Monitor Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

Europe 360 Around View Monitor MarketTrends

Rising Integration of AI and Machine Learning

The integration of artificial intelligence and machine learning algorithms into 360 around view systems has significantly transformed the market. In 2025, over 2.8 million AI-enabled systems were deployed across Europe, representing nearly 31% of total installations. These systems enhance object detection accuracy by up to 92% and reduce collision risks by approximately 28%. Automakers are increasingly adopting AI-based surround-view systems capable of predictive analytics and real-time hazard detection, particularly in high-density urban environments. The shift toward autonomous driving technologies is also fueling demand, with 45% of new electric vehicles incorporating advanced monitoring systems. This technological evolution is a key Europe 360 Around View Monitor Market Trend.

Expansion of Electric Vehicle Integration

The rapid growth of electric vehicles (EVs), with over 3.5 million EV units sold in Europe in 2025, is driving the integration of advanced camera systems. Nearly 52% of EVs now include 360-degree monitoring systems as standard or optional features. The demand is further supported by the compact design of EVs, requiring enhanced visibility solutions for safe navigation. Additionally, EV manufacturers are investing heavily in digital cockpit technologies, integrating surround-view systems with infotainment displays. This trend is expected to push production volumes of camera modules beyond 15 million units annually by 2030, reinforcing the Europe 360 Around View Monitor Market Trend.

Europe 360 Around View Monitor Market Driver

Increasing Vehicle Safety Regulations Across Europe

Stringent safety regulations imposed by the European Union, including mandatory ADAS features, are a primary driver of the market. Over 78% of new vehicles sold in Europe in 2025 comply with advanced safety standards, with 360-degree monitoring systems playing a critical role. The EU’s General Safety Regulation (GSR) mandates features such as blind-spot detection and parking assistance, driving system adoption by over 22% annually. Additionally, accident statistics indicate that parking-related collisions account for nearly 34% of minor accidents, encouraging the adoption of surround-view systems. Automotive manufacturers are investing approximately USD 3.2 billion annually in safety technologies, further boosting system deployment. This regulatory push significantly contributes to the Europe 360 Around View Monitor Market Growth.

Europe 360 Around View Monitor Market Restraint

High Installation and Maintenance Costs

Despite strong demand, high system costs remain a significant restraint. The average cost of a 360-degree monitoring system ranges between USD 300 and USD 1,200, depending on resolution and AI integration. This limits adoption in low-cost vehicle segments, which account for nearly 40% of total vehicle sales in Europe. Additionally, maintenance costs, including camera calibration and sensor replacement, can increase operational expenses by 12–18% annually. Small and medium automotive manufacturers face challenges in integrating these systems due to limited budgets, slowing penetration rates in certain regions. This cost barrier impacts the Europe 360 Around View Monitor Market Growth.

Europe 360 Around View Monitor Market Opportunity

Expansion in Autonomous and Connected Vehicles

The growing adoption of autonomous and connected vehicles presents significant opportunities for the market. Europe is expected to have over 8 million semi-autonomous vehicles by 2030, with 360-degree monitoring systems serving as a core component. Connected vehicle technologies enable real-time data sharing, enhancing system performance and safety. Investments in smart mobility solutions have increased by 26% annually, with governments allocating over USD 5 billion toward infrastructure development. This creates a favorable environment for advanced camera systems, particularly AI-integrated solutions, driving the Europe 360 Around View Monitor Market Growth.

Challenge in Europe 360 Around View Monitor Market

Technical Complexity and Data Processing Limitations

The integration of multiple high-resolution cameras and real-time processing systems presents technical challenges. Processing data from 4–6 cameras simultaneously requires high-performance computing units, increasing system complexity. Latency issues, even at 80–100 milliseconds, can impact system reliability, particularly in high-speed scenarios. Additionally, data storage and bandwidth requirements for 4K video processing can exceed 2–3 GB per hour, posing challenges for onboard systems. Manufacturers must invest heavily in R&D, with spending exceeding USD 1.5 billion annually, to overcome these limitations. These challenges influence the Europe 360 Around View Monitor Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.24 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 4.18 billion |

| CAGR | 14.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Europe 360 Around View Monitor Market Segmentation

By Type

2D view systems account for approximately 28% of the market, with over 3.1 million units produced annually. These systems typically utilize four cameras with resolutions ranging from 720p to 1080p, offering basic bird’s-eye visualization. Their cost-effectiveness, with prices averaging USD 300–USD 500, makes them popular in mid-range vehicles. However, limitations in depth perception reduce their effectiveness compared to advanced systems.

3D view systems dominate with a 44% share, producing over 4.8 million units annually. These systems provide enhanced depth perception and dynamic rendering, improving driver awareness by up to 35%. Equipped with high-definition cameras and advanced processors, they operate at frame rates of 60 fps, ensuring smooth visualization.

AI-integrated systems hold a 28% share, with production exceeding 2.9 million units. These systems incorporate machine learning algorithms for object detection, achieving accuracy rates above 90%. They are increasingly adopted in premium vehicles, with prices ranging from USD 800 to USD 1,200.

By Application

Passenger vehicles dominate with a 68% share, with over 10.5 million units equipped with 360-degree monitoring systems. Urban driving conditions and parking challenges drive demand, with penetration rates reaching 55% in luxury segments.

Commercial vehicles account for 22%, with approximately 3.4 million units using these systems. Fleet operators benefit from improved safety and reduced accident rates by 18%, leading to lower insurance costs.

Off-highway vehicles represent 10%, with around 1.5 million units deployed. These systems enhance visibility in construction and agricultural applications, improving operational efficiency by 25%.

Europe 360 Around View Monitor Market Segmentations

Type

- 2D View Systems

- 3D View Systems

- AI-Integrated Systems

Application

- Passenger Vehicles

- Commercial Vehicles

- Off-Highway Vehicles

Country Insights Europe 360 Around View Monitor Market

United Kingdom

The UK holds approximately 18% of the European market, with over 2.8 million vehicles equipped annually. Strong EV adoption and safety regulations drive demand.

Germany

Germany leads with a 26% share, producing over 4.5 million vehicles annually with advanced monitoring systems. Premium car manufacturers significantly contribute to market growth.

France

France accounts for 21% share, driven by strong automotive manufacturing and government incentives.

Spain

Spain holds 12% share, with increasing adoption in commercial vehicles.

Italy

Italy contributes 11%, with growing demand in passenger vehicles.

Russia

Russia accounts for 12%, driven by expanding automotive production.

Top Players in Europe 360 Around View Monitor Market

- Bosch

- Continental AG

- Valeo

- Denso Corporation

- Magna International

- ZF Friedrichshafen

- Aptiv

- Hyundai Mobis

- Panasonic Automotive

- Ficosa International

- Hella GmbH

- Clarion Co., Ltd.

Top Two Companies

Bosch

- Holds approximately 18% market share

- Strong presence in ADAS technologies

- Invests over USD 500 million annually in R&D

Continental AG

- Accounts for 15% market share

- Leading supplier of camera-based systems

- Focuses on AI integration and autonomous driving

Investment

Investments in the market have grown significantly, with over USD 4.5 billion allocated annually across Europe. Approximately 42% of investments focus on AI and software development, while 33% target hardware advancements such as high-resolution cameras. Germany and France account for 48% of total investments, driven by strong automotive industries.

M&A activities have increased by 22% annually, with major companies acquiring startups specializing in AI and computer vision technologies. Collaborations between automotive manufacturers and technology firms are also rising, enhancing innovation and market expansion opportunities.

New Product

New product development accounts for nearly 35% of total market activities, with companies introducing advanced systems featuring 4K resolution and real-time AI analytics. Performance improvements of up to 40% in object detection and 25% in processing speed have been achieved.

Recent Development in Europe 360 Around View Monitor Market

- 2025: Bosch increased production by 18%, launching AI-powered systems improving safety by 30%.

- 2024: Continental expanded production capacity by 22%, enhancing supply chain efficiency.

- 2023: Valeo introduced 4K camera systems, improving resolution by 45%.

Research Methodology for Europe 360 Around View Monitor Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with industry experts, automotive manufacturers, and technology providers, accounting for 60% of data collection. Secondary research involved analysis of industry reports, company publications, and government databases, contributing 40% of insights. Market size estimation was conducted using a bottom-up approach, analyzing production volumes and pricing trends across regions. Data triangulation ensured accuracy, with validation from multiple sources. Statistical models were used to forecast market trends, considering factors such as technological advancements, regulatory changes, and consumer demand patterns.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.