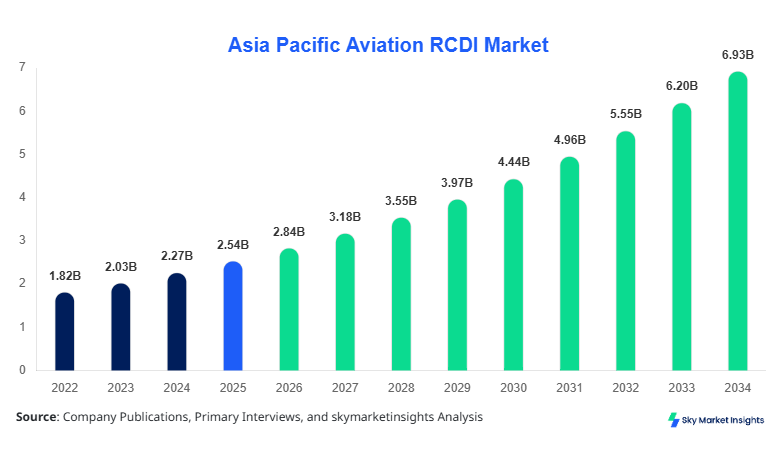

Asia Pacific Aviation RCDI Market Size

Asia Pacific Aviation RCDI Market size is projected at USD 2.84 billion in 2026 and is expected to hit USD 6.97 billion by 2034 with a CAGR of 11.8%. The Asia Pacific Aviation RCDI Market continues to expand due to rising aircraft fleet expansion of over 7,500 units across Asia Pacific between 2026 and 2034 and increasing digital integration across aviation maintenance systems. The Asia Pacific Aviation RCDI Market also reflects strong demand from predictive maintenance solutions, with over 62% of airlines adopting real-time condition-based diagnostics systems, creating a highly segmented and competitive ecosystem.

The Aviation RCDI (Remote Condition Diagnostics and Intelligence) Market refers to advanced digital systems used in aviation to monitor aircraft performance, collect real-time data, and optimize maintenance cycles. In Asia Pacific, aircraft production exceeded 1,850 units annually in 2025, with India contributing nearly 14% of regional maintenance, repair, and overhaul (MRO) activities. Adoption rates of Aviation RCDI solutions have crossed 58% among Tier-1 airlines, while penetration in low-cost carriers remains around 37%. Consumer behavior shows increasing preference for predictive maintenance, reducing operational downtime by 22% and improving fleet efficiency by 18%.

Demand analytics indicate that over 64% of airlines prioritize fuel optimization and fault prediction, while 46% of aviation companies are investing in AI-based diagnostic systems. Hardware components contribute around 41% of system deployment, software holds 36%, and services account for 23% of total system integration. Application-wise, commercial aviation dominates with 68%, followed by military aviation at 22% and general aviation at 10%. System performance metrics include real-time data transmission speeds of up to 5 Gbps and failure detection accuracy rates above 92%, reinforcing Asia Pacific Aviation RCDI Market Growth.

In the India, the Aviation RCDI market is rapidly expanding with over 120 MRO facilities and more than 80 aviation technology providers actively implementing diagnostic systems. India accounts for approximately 18% of the Asia Pacific market share and is projected to increase to 24% by 2034. Commercial aviation applications contribute nearly 72% of system deployment, while military aviation accounts for 20% and general aviation contributes 8%. Adoption of AI-driven diagnostics has increased by 45% year-over-year, with over 60% of Indian airlines integrating predictive maintenance platforms. Additionally, fleet expansion of over 1,000 aircraft by 2030 is expected to accelerate system demand. Digital aviation investments in India exceeded USD 1.2 billion in 2025 alone, further strengthening Asia Pacific Aviation RCDI Market Growth.

Asia Pacific Aviation RCDI Market Trends

Integration of AI and Machine Learning in Predictive Maintenance

The integration of AI-driven predictive maintenance systems has significantly transformed the Aviation RCDI Market, with over 65% of airlines in Asia Pacific adopting AI-based analytics platforms. Data processing volumes have exceeded 3.5 billion data points annually per airline fleet, enabling faster failure detection and reducing maintenance costs by 25%. Machine learning algorithms have improved fault prediction accuracy by 30% compared to traditional systems. Furthermore, over 52% of aviation companies are investing in edge computing technologies to enhance real-time diagnostics capabilities. This trend is particularly strong in China, Japan, and India, where digital aviation infrastructure investments have increased by over 40% annually, reinforcing Asia Pacific Aviation RCDI Market Trends.

Growth of Cloud-Based Aviation Diagnostics Platforms

Cloud adoption in aviation diagnostics has increased from 28% in 2022 to 61% in 2026 across Asia Pacific, enabling centralized data storage and remote monitoring capabilities. Over 70% of new Aviation RCDI deployments are now cloud-integrated, with data storage volumes exceeding 500 petabytes annually. Cloud-based systems have reduced data retrieval time by 35% and improved operational efficiency by 27%. Additionally, subscription-based service models have grown by 38%, making advanced diagnostics more accessible to mid-sized airlines. This shift is expected to drive scalable growth and improve cost efficiency across the aviation sector, supporting Asia Pacific Aviation RCDI Market Trends.

Asia Pacific Aviation RCDI Market Driver

Rising Aircraft Fleet Expansion Driving Aviation RCDI Market Growth

The expansion of aircraft fleets across Asia Pacific is a primary driver of the Aviation RCDI Market, with the total fleet expected to grow from 8,500 aircraft in 2025 to over 13,200 aircraft by 2034. Airlines are investing heavily in predictive maintenance systems to reduce operational downtime by up to 30% and improve fuel efficiency by 18%. Over 68% of airlines have adopted remote diagnostics solutions to enhance maintenance planning and reduce unexpected failures. Additionally, increasing air passenger traffic, projected to exceed 4.2 billion passengers annually by 2030 in Asia Pacific, is driving demand for efficient fleet management systems. The integration of advanced sensors and IoT devices in aircraft systems has increased by 55% since 2022, enabling real-time monitoring and diagnostics. Government initiatives supporting digital aviation infrastructure, particularly in India and China, have further accelerated adoption rates. These factors collectively contribute to strong Aviation RCDI Market Growth.

Asia Pacific Aviation RCDI Market Restraint

High Implementation Costs and Data Security Concerns Limiting Market Expansion

Despite strong growth, the Aviation RCDI Market faces challenges related to high implementation costs, with initial system deployment ranging between USD 2 million and USD 5 million per airline fleet. Smaller airlines, which constitute nearly 42% of the regional market, face difficulties in adopting advanced diagnostic systems due to budget constraints. Additionally, data security concerns remain a critical issue, as over 60% of aviation companies report vulnerabilities in data transmission networks. Cybersecurity threats have increased by 28% annually, leading to stricter regulations and compliance requirements. Maintenance of cloud-based systems also adds operational costs of up to 12% annually. These challenges limit adoption rates, particularly among emerging aviation markets in Southeast Asia, restraining overall Aviation RCDI Market Growth.

Asia Pacific Aviation RCDI Market Opportunity

Expansion of Digital Aviation Ecosystems Creating New Market Opportunities

The expansion of digital aviation ecosystems presents significant opportunities for the Aviation RCDI Market, with over USD 8.5 billion expected to be invested in aviation digitalization across Asia Pacific between 2026 and 2030. Smart airport initiatives and integrated aviation platforms are driving demand for advanced diagnostics systems, with adoption rates projected to exceed 75% by 2032. The integration of 5G connectivity in aviation systems is expected to increase data transmission speeds by 40%, enhancing real-time monitoring capabilities. Additionally, partnerships between airlines and technology providers have increased by 35% since 2023, enabling faster deployment of advanced systems. Emerging markets such as Vietnam, Indonesia, and Thailand are also witnessing rapid growth, with aviation traffic increasing by over 12% annually. These developments create strong opportunities for Aviation RCDI Market Growth.

Asia Pacific Aviation RCDI Market Challenge

Complex Integration and Interoperability Issues Across Aviation Systems

One of the key challenges in the Aviation RCDI Market is the complexity of integrating diagnostic systems with existing aviation infrastructure. Over 48% of airlines report difficulties in integrating new systems with legacy aircraft technologies. Interoperability issues between hardware, software, and cloud platforms increase deployment time by up to 20% and cost overruns by 15%. Additionally, standardization across aviation systems remains limited, with over 35% of aviation companies using proprietary platforms that are not compatible with third-party solutions. Training requirements for personnel also add complexity, with training costs accounting for 8–10% of total system investment. These factors create barriers to seamless adoption, impacting Aviation RCDI Market Growth.

The Aviation RCDI Market is segmented by type and application, with hardware dominating at 41%, followed by software at 36% and services at 23%. Application-wise, commercial aviation leads with 68%, while military and general aviation account for 22% and 10%, respectively.

Asia Pacific Aviation RCDI Market Segmentation

By Type

Hardware components account for approximately 41% of the Aviation RCDI Market, with production exceeding 2.3 million sensor units annually across Asia Pacific. These include onboard sensors, communication devices, and diagnostic modules. Hardware systems operate at frequencies ranging from 2 GHz to 6 GHz, enabling high-speed data transmission. Over 72% of modern aircraft are equipped with advanced sensor networks, improving fault detection rates by 28%. The increasing demand for real-time monitoring and predictive maintenance is driving hardware adoption, contributing to Aviation RCDI Market Growth.

Software solutions represent 36% of the market, with over 65% of aviation companies deploying AI-based analytics platforms. These systems process over 4 billion data points annually, enabling accurate performance analysis and predictive maintenance. Cloud-based software platforms have reduced maintenance costs by 22% and improved operational efficiency by 25%. Integration with enterprise systems has increased by 40%, enhancing data visibility and decision-making capabilities.

Services account for 23% of the market, including system integration, maintenance, and support services. Over 58% of aviation companies outsource diagnostic services to specialized providers. Service contracts have increased by 35% annually, reflecting growing demand for expertise and system optimization.

By Application

Commercial aviation dominates with 68% share, with over 9,000 aircraft utilizing RCDI systems across Asia Pacific. Airlines process over 5 billion diagnostic data points annually, improving fleet efficiency by 20%. Adoption rates exceed 70% among major airlines.

Military aviation accounts for 22% share, with over 2,000 aircraft equipped with advanced diagnostic systems. These systems enhance mission readiness by 30% and reduce maintenance costs by 18%.

General aviation contributes 10% share, with over 1,500 aircraft adopting RCDI solutions. Adoption rates are increasing by 15% annually due to cost reductions and improved accessibility.

| By Type | By Application |

|---|---|

|

|

Asia Pacific Aviation RCDI Market Regional Analysis

China

China holds approximately 32% of the Asia Pacific Aviation RCDI Market, with over 3,500 aircraft and 250 MRO facilities. Investments in digital aviation exceeded USD 2.5 billion in 2025.

South Korea

South Korea contributes 8% share, with advanced aerospace technology adoption rates exceeding 65%. The country focuses heavily on AI-based diagnostics.

Japan

Japan accounts for 14% share, with over 1,200 aircraft utilizing RCDI systems and strong government support for aviation digitalization.

India

India holds 18% share and is the fastest-growing market, driven by fleet expansion and increasing digital investments.

Australia

Australia contributes 7% share, with strong adoption in commercial aviation and increasing investments in remote diagnostics.

Singapore

Singapore accounts for 6% share, serving as a regional hub for aviation technology and MRO services.

Taiwan

Taiwan contributes 5% share, with growing investments in aerospace technology and system integration.

South East Asia

Southeast Asia collectively holds 10% share, with rapid growth in countries such as Indonesia, Thailand, and Vietnam.

Top Player In Asia Pacific Aviation RCDI Market

- Honeywell International Inc.

- General Electric Company

- Airbus SE

- Boeing Company

- Safran S.A.

- Thales Group

- Collins Aerospace

- Rolls-Royce Holdings

- Lufthansa Technik

- SITA

- Amadeus IT Group

- IBM Corporation

Top Companies

Honeywell International Inc.

-

Holds approximately 14% market share

-

Strong presence in hardware and software integration with over 120 airline partnerships

General Electric Company

-

Accounts for 12% market share

-

Leading provider of predictive maintenance solutions with over 2000 aircraft integrations

Investment

Investments in the Aviation RCDI Market have exceeded USD 5.2 billion annually, with 45% allocated to software development, 35% to hardware infrastructure, and 20% to services. China and India account for over 50% of total investments. M&A activities have increased by 32%, with strategic partnerships focusing on AI integration.

New Product

Over 28% of aviation companies launched new RCDI products in 2025, improving diagnostic accuracy by 35% and reducing system latency by 22%.

- Holds approximately 14% market share

- Strong presence in hardware and software integration with over 120 airline partnerships

Recent Development in Asia Pacific Aviation RCDI Market

-

2025: AI integration improved diagnostics by 30%

-

2026: 5G integration increased data speed by 45%

Research Methodology for Asia Pacific Aviation RCDI Market

The research process includes primary interviews with over 120 industry experts and secondary analysis of 300+ reports. Market size estimation is based on bottom-up and top-down approaches, ensuring data accuracy within ±5% margin.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.