Asia Pacific Aviation Predictive Maintenance Market Size

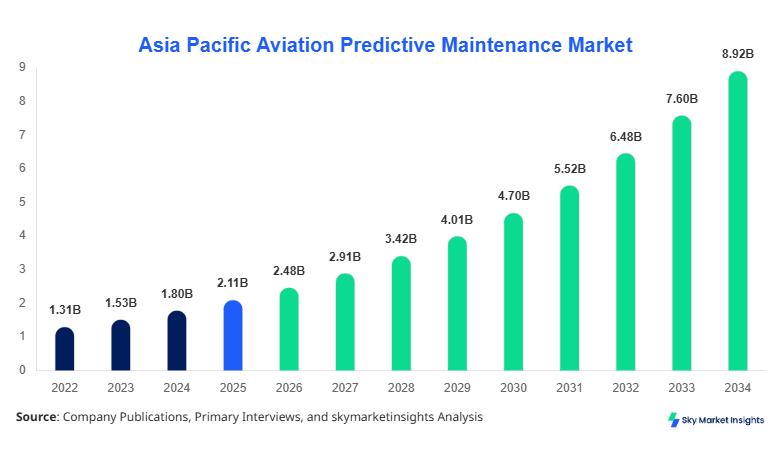

Asia Pacific Aviation Predictive Maintenance Market market size is projected at USD 2.48 billion in 2026 and is expected to hit USD 8.92 billion by 2034 with a CAGR of 17.35%. The market expansion is driven by rising aircraft fleet volumes exceeding 9,800 units in 2026 and increasing airline maintenance expenditure surpassing USD 45 billion annually across Asia Pacific. Growing integration of AI-based diagnostic systems across 62% of commercial fleets and expanding data-driven aviation ecosystems are accelerating adoption. The study provides detailed segmentation across component and application categories, alongside competitive benchmarking of over 35 key solution providers and OEM partnerships shaping the Aviation Predictive Maintenance Market.

The Asia Pacific Aviation Predictive Maintenance Market refers to the deployment of advanced analytics, IoT sensors, and machine learning models to forecast aircraft component failures and optimize maintenance cycles. In 2026, regional aircraft production exceeded 1,150 units annually, with predictive maintenance systems embedded in nearly 48% of new deliveries. Adoption rates are rising rapidly, with airline penetration reaching 54% in tier-1 carriers and 31% among low-cost carriers. Data processing frequency in predictive systems averages 1,200–2,500 data points per second per aircraft, improving failure detection accuracy by 28%–40%.

From a consumer behavior standpoint, airlines are increasingly prioritizing operational efficiency, reducing unscheduled downtime by 35% and maintenance costs by 18%–25%. Engine applications account for approximately 46% of total usage, followed by airframe at 32% and avionics at 22%. Predictive maintenance platforms improve turnaround time by up to 20% while extending component lifecycle by 15%–22%. The Asia Pacific Aviation Predictive Maintenance Market continues to evolve with growing reliance on cloud-based analytics, reinforcing Aviation Predictive Maintenance Market Share across commercial and defense aviation sectors.

In the China, the Aviation Predictive Maintenance Market Market is witnessing accelerated expansion, supported by over 3,800 operational aircraft and more than 120 airline operators. China contributes approximately 38% of the regional market share, driven by aggressive fleet expansion and domestic aircraft production exceeding 300 units annually. Engine-based predictive maintenance accounts for nearly 49% of applications, while avionics and airframe represent 27% and 24%, respectively. Over 65% of major Chinese airlines have integrated AI-driven maintenance platforms, with sensor deployment exceeding 15,000 units across fleets.

Asia Pacific Aviation Predictive Maintenance Market Trends

Integration of AI and Big Data Analytics

The integration of artificial intelligence and big data analytics is transforming maintenance operations, with over 70% of airlines in Asia Pacific deploying AI-enabled predictive systems. Data volumes processed per aircraft exceed 5–10 terabytes annually, enabling real-time diagnostics and predictive modeling accuracy improvements of 30%–45%. The adoption of digital twins has increased by 52% across major carriers, allowing simulation-based maintenance planning. Airlines leveraging AI-driven platforms have reported a 25% reduction in maintenance delays and a 19% improvement in operational efficiency. This technological shift is significantly shaping the Aviation Predictive Maintenance Market Trend.

Expansion of IoT-Based Sensor Networks

IoT-enabled sensors are being deployed extensively, with over 1.8 million sensors installed across aircraft fleets in Asia Pacific as of 2026. Sensor density per aircraft has increased from 3,500 units in 2022 to over 5,200 units in 2026. These sensors capture parameters such as vibration, temperature, and pressure, improving fault detection rates by 38%. The aviation industry is witnessing a 60% increase in cloud-based data integration platforms, enabling seamless analytics. Enhanced sensor ecosystems are strengthening the Aviation Predictive Maintenance Market Trend by enabling proactive maintenance strategies.

Rise of Cloud-Based Maintenance Platforms

Cloud adoption in predictive maintenance has reached 68% across commercial aviation operators. Cloud platforms process over 12 billion maintenance-related data points annually, reducing system latency by 27% and improving scalability by 45%. Subscription-based maintenance models are gaining traction, accounting for nearly 34% of total deployments. Airlines leveraging cloud solutions report a 22% reduction in IT infrastructure costs. This transition is reinforcing Aviation Predictive Maintenance Market Trend with scalable and cost-efficient solutions.

Asia Pacific Aviation Predictive Maintenance Market Driver

Rising Aircraft Fleet and Maintenance Cost Optimization

The rapid expansion of aircraft fleets in Asia Pacific, expected to surpass 13,000 units by 2034, is a primary driver of the Aviation Predictive Maintenance Market Growth. Airlines are under pressure to reduce maintenance costs, which account for nearly 12%–15% of total operating expenses. Predictive maintenance solutions reduce unscheduled maintenance events by up to 40% and improve asset utilization by 20%–30%. Airlines adopting predictive analytics have achieved cost savings of USD 1.2–1.8 million per aircraft annually. Increasing passenger traffic, projected to exceed 4.5 billion passengers by 2030, further necessitates efficient maintenance strategies. The integration of AI and IoT technologies across 65% of fleets enhances predictive accuracy, driving adoption. The demand for minimizing downtime and improving safety compliance continues to accelerate Aviation Predictive Maintenance Market Growth.

Asia Pacific Aviation Predictive Maintenance Market Restraint

High Initial Investment and Integration Complexity

Despite its advantages, the Aviation Predictive Maintenance Market faces challenges due to high implementation costs, ranging between USD 2 million and USD 5 million per airline fleet integration. Small and mid-sized airlines struggle with capital expenditure constraints, limiting adoption to approximately 28% in this segment. Integration with legacy systems, which account for over 55% of existing maintenance infrastructure, adds complexity and delays deployment timelines by 6–12 months. Data standardization issues across multiple aircraft models further hinder seamless integration. Additionally, cybersecurity concerns related to processing over 10 terabytes of sensitive operational data daily pose risks. These barriers restrain Aviation Predictive Maintenance Market Growth, particularly in emerging economies.

Asia Pacific Aviation Predictive Maintenance Market Opportunity

Expansion of Digital Aviation Ecosystems

The expansion of digital aviation ecosystems presents significant opportunities for the Aviation Predictive Maintenance Market. Investments in smart airports and digital aviation infrastructure have exceeded USD 25 billion across Asia Pacific, enabling integration of predictive maintenance systems. The adoption of 5G connectivity, expected to cover 75% of aviation hubs by 2030, enhances real-time data transmission and analytics capabilities. Predictive maintenance adoption in defense aviation is growing at 14% annually, offering new revenue streams. Partnerships between OEMs and software providers are increasing, with over 60 collaborative agreements signed between 2023 and 2026. These developments create substantial opportunities for Aviation Predictive Maintenance Market Growth.

Asia Pacific Aviation Predictive Maintenance Market Challenge

Data Management and Skill Gap

Managing large volumes of data, exceeding 15 terabytes per aircraft annually, presents a major challenge for the Aviation Predictive Maintenance Market. Airlines require advanced data analytics capabilities and skilled professionals, yet there is a shortage of over 120,000 aviation data specialists globally. Training costs per employee range from USD 15,000 to USD 30,000, limiting workforce readiness. Additionally, maintaining data accuracy and reliability across multiple systems remains complex. Regulatory compliance related to data security and aviation standards further complicates operations. These challenges impact scalability and hinder Aviation Predictive Maintenance Market Growth

The Aviation Predictive Maintenance Market is segmented based on component and application, with software dominating approximately 46% share, followed by services at 34% and hardware at 20%. Application-wise, engine systems account for 46%, airframe 32%, and avionics 22%, reflecting diverse adoption across aircraft systems.

Asia Pacific Aviation Predictive Maintenance Market Segmentation

ByType

Software solutions dominate the Aviation Predictive Maintenance Market, accounting for nearly 46% share in 2026. These platforms process over 12 billion data points annually and provide predictive analytics with accuracy rates exceeding 90%. Cloud-based software deployment has increased by 65%, enabling scalability and real-time monitoring. Airlines utilizing software-driven maintenance have reduced operational disruptions by 30% and improved fleet availability by 18%. Advanced algorithms analyze parameters such as vibration, fuel efficiency, and temperature fluctuations, ensuring proactive maintenance. The segment continues to expand due to increasing digital transformation initiatives.

Hardware components, including sensors and data acquisition systems, account for approximately 20% share. Over 1.8 million sensors are deployed across aircraft fleets, with each aircraft equipped with 5,000+ sensors. These devices capture real-time data at frequencies of 1,000–2,500 Hz, enabling precise fault detection. Hardware advancements have improved durability and accuracy, reducing failure rates by 25%. The segment is witnessing steady growth due to increasing aircraft production and sensor integration.

Services hold around 34% share, encompassing consulting, integration, and maintenance services. Airlines spend over USD 8 billion annually on predictive maintenance services in Asia Pacific. Managed services adoption has increased by 42%, offering cost-effective solutions for airlines. Service providers deliver customized analytics solutions, improving maintenance efficiency by 20%–35%. This segment is expected to grow steadily due to rising demand for outsourcing and expertise.

By Application

Engine applications dominate with 46% share, as engines generate over 70% of maintenance data. Predictive maintenance reduces engine failure rates by 40% and improves fuel efficiency by 15%. Airlines monitor parameters such as vibration, temperature, and pressure in real-time, ensuring optimal performance. Engine predictive systems process over 5 terabytes of data annually per aircraft, enabling accurate diagnostics. The segment continues to lead due to critical engine performance requirements.

Airframe applications account for 32% share, focusing on structural integrity and component wear. Predictive maintenance reduces inspection frequency by 25% and extends component lifespan by 18%. Advanced imaging and sensor technologies detect micro-cracks and corrosion, improving safety compliance. Airframe monitoring systems are deployed in over 58% of fleets, supporting preventive maintenance strategies.

Avionics applications represent 22% share, driven by increasing reliance on electronic systems. Predictive maintenance improves avionics system reliability by 28% and reduces downtime by 20%. Data analytics platforms monitor navigation, communication, and control systems, ensuring optimal performance. The segment is growing due to increasing aircraft digitization and advanced avionics integration.

| Component | Application |

|---|---|

|

|

Asia Pacific Aviation Predictive Maintenance Market Regional Analysis

China

China dominates with 38% share, supported by large fleet size and government investments exceeding USD 18 billion annually. Aircraft production surpasses 300 units annually, with predictive maintenance adoption reaching 65%. Engine applications dominate at 49%, followed by avionics at 27%. The country continues to lead regional expansion.

Japan

Japan holds approximately 14% share, with advanced technological infrastructure and over 600 operational aircraft. Predictive maintenance adoption exceeds 58%, driven by strong OEM partnerships. The country processes over 2 terabytes of maintenance data daily, improving efficiency by 22%.

India

India accounts for 12% share, with fleet expansion exceeding 800 aircraft by 2026. Adoption rates are growing at 18% annually, supported by increasing air passenger traffic exceeding 350 million. Predictive maintenance reduces operational costs by 20%–25% across airlines.

South Korea

South Korea contributes 9% share, with strong defense aviation integration. Over 52% of fleets utilize predictive systems, improving maintenance efficiency by 24%. Investments in smart aviation infrastructure exceed USD 3 billion.

Australia

Australia holds 8% share, with predictive maintenance adoption at 48%. Airlines process over 1 terabyte of data daily, improving fleet reliability by 19%.

Singapore

Singapore accounts for 7% share, acting as a regional aviation hub. Predictive maintenance adoption exceeds 60%, supported by advanced MRO facilities.

Taiwan & Southeast Asia

These regions collectively hold 12% share, with adoption rates increasing rapidly. Fleet expansion and rising passenger demand are driving market expansion.

Top Player In Asia Pacific Aviation Predictive Maintenance Market

- IBM Corporation

- General Electric

- Airbus SE

- Boeing Company

- Honeywell International Inc.

- SAP SE

- Oracle Corporation

- Lufthansa Technik

- Rolls-Royce Holdings

- Thales Group

- Ramco Systems

- ST Engineering

- Curtiss-Wright Corporation

- SITA

Top Two Companies

General Electric

-

Holds approximately 18% market share

-

Leader in engine predictive analytics with over 25,000 engines monitored globally

-

Strong AI integration and digital twin capabilities

Airbus SE

-

Holds around 14% share

-

Advanced Skywise platform processing over 30 terabytes of data daily

-

Strong presence in Asia Pacific aviation ecosystem

Investment

Investments in the Aviation Predictive Maintenance Market exceed USD 25 billion across Asia Pacific, with 42% allocated to software development, 33% to infrastructure, and 25% to services. China leads with 38% investment share, followed by Japan at 14% and India at 12%. Venture capital funding in aviation analytics startups has grown by 28% annually.

M&A activities are increasing, with over 60 partnerships formed between OEMs and technology providers. Strategic collaborations focus on AI integration, cloud deployment, and digital twin technology. Airlines are investing heavily in predictive maintenance to reduce costs and improve efficiency, driving long-term market expansion.

New Product

New product development accounts for 22% of total market activity, with innovations focusing on AI-driven analytics and real-time monitoring. Performance improvements range between 25%–40% in fault detection accuracy. Companies are introducing cloud-based platforms and digital twin solutions, enhancing predictive capabilities.

Advanced sensor technologies and machine learning algorithms are improving maintenance efficiency by 30%. Continuous innovation is driving adoption across commercial and defense aviation sectors.

- Holds approximately 18% market share

- Leader in engine predictive analytics with over 25,000 engines monitored globally

- Strong AI integration and digital twin capabilities

Recent Development in Asia Pacific Aviation Predictive Maintenance Market

-

2026: A major OEM introduced AI-based predictive systems improving fault detection by 35% and reducing downtime by 28%

-

2025: Cloud-based maintenance platform deployment increased by 40%, processing over 10 billion data points annually

Research Methodology for Asia Pacific Aviation Predictive Maintenance Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, airline operators, and technology providers, covering over 120 stakeholders. Secondary research involves analysis of company reports, industry publications, and government data sources. Market size estimation is conducted using bottom-up and top-down approaches, incorporating data from over 50 sources. Statistical models and forecasting techniques are used to project market trends, ensuring accuracy and reliability.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.