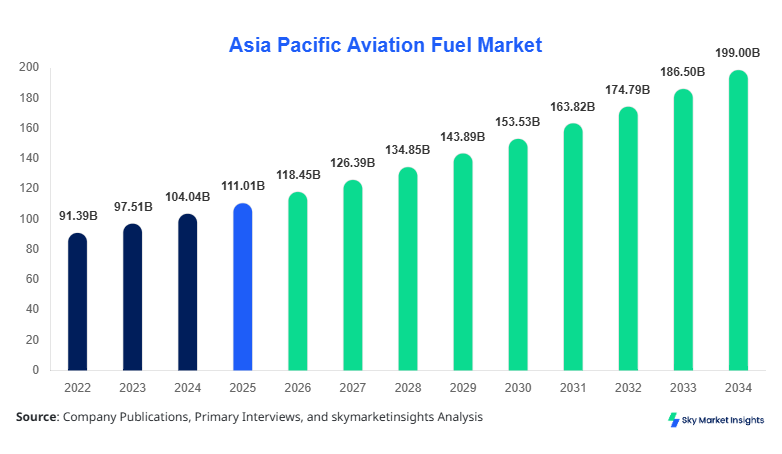

Asia Pacific Aviation Fuel Market Size

Asia Pacific Aviation Fuel market size is projected at USD 118.45 billion in 2026 and is expected to hit USD 198.72 billion by 2034 with a CAGR of 6.7%. The increasing air passenger traffic exceeding 4.2 billion globally and rising cargo volumes of over 65 million metric tons annually are significantly driving demand. The market analysis incorporates detailed segmentation across fuel types and applications, alongside a competitive landscape evaluation of key suppliers and refiners operating across Asia Pacific. The report provides comprehensive insights into production capacity exceeding 350 million barrels annually and consumption patterns influenced by technological advancements and regulatory frameworks.

The aviation fuel market refers to the production, distribution, and consumption of specialized petroleum-based fuels such as Jet A, Jet A-1, and sustainable aviation fuels used in aircraft operations. In Asia Pacific, production capacity exceeded 320 million metric tons in 2025, accounting for nearly 35% of global aviation fuel output. Adoption and penetration of aviation fuel remain high, with over 92% of commercial aircraft relying on Jet A-1 fuel, while sustainable aviation fuel penetration is currently at 2.5% but expected to rise to 12% by 2034. Consumer behavior indicates rising air travel demand, with passenger traffic in Asia Pacific growing at 7.8% annually and low-cost carriers contributing over 48% of regional demand.

Demand analytics reveal that commercial aviation accounts for nearly 68% of total fuel consumption, followed by cargo aviation at 21% and military aviation at 11%. Fuel performance metrics such as energy density (43 MJ/kg) and combustion efficiency exceeding 98% are critical for operational efficiency. Application-wise, domestic routes account for 55% of fuel usage, while international long-haul routes contribute 45%. Increasing investments in fuel-efficient aircraft and sustainable alternatives continue to shape the aviation fuel market dynamics.

In the India, the Aviation Fuel Market is witnessing rapid expansion with over 150 operational airports and more than 35 active airline operators contributing to demand. India accounts for approximately 18% of Asia Pacific aviation fuel consumption, with annual demand exceeding 28 million metric tons. Commercial aviation dominates with a 72% share, followed by cargo aviation at 17% and military aviation at 11%. The adoption of sustainable aviation fuel in India is currently at 1.8% but is projected to reach 10% by 2034 due to government mandates and carbon reduction goals.

Asia Pacific Aviation Fuel Market Trends

Rising Adoption of Sustainable Aviation Fuel

The production of sustainable aviation fuel (SAF) in Asia Pacific reached approximately 4.5 billion liters in 2025, with adoption rates growing at 22% annually. Airlines are increasingly blending SAF with conventional fuels at ratios of 5% to 20%, reducing carbon emissions by up to 80%. Governments across countries like Japan, Australia, and Singapore are mandating SAF usage targets of 10%–15% by 2030. Investments in bio-refineries have increased by 28%, enhancing production capabilities. This shift toward environmentally sustainable fuels is significantly shaping the aviation fuel market.

Increasing Air Passenger Traffic and Fleet Expansion

Asia Pacific recorded over 1.8 billion air passengers in 2025, representing nearly 34% of global traffic. Fleet expansion is also notable, with over 8,500 aircraft operating in the region and an additional 4,000 aircraft on order. Fuel consumption per aircraft averages 3,500 liters per hour for narrow-body aircraft and up to 12,000 liters per hour for wide-body aircraft. The increasing frequency of flights, averaging 120,000 daily operations globally, is driving higher fuel consumption. These developments continue to accelerate the aviation fuel market expansion.

Digital Fuel Management Systems

Airlines are adopting advanced digital fuel management systems, improving efficiency by 12%–18% and reducing wastage by nearly 9%. Over 65% of major airlines in Asia Pacific have integrated AI-based fuel optimization systems. These systems analyze flight paths, weather conditions, and aircraft performance to minimize fuel consumption. This trend is enhancing operational efficiency and cost management, reinforcing aviation fuel market advancements.

Asia Pacific Aviation Fuel Market Size Driver

Surging Air Travel Demand and Fleet Expansion Driving Aviation Fuel Market Growth

The increasing demand for air travel is a major driver of the aviation fuel market, with passenger traffic growing at 7%–9% annually across Asia Pacific. The region accounted for over 1.8 billion passengers in 2025, with projections indicating 2.6 billion by 2030. Airlines are expanding their fleets, with more than 4,000 new aircraft deliveries expected by 2034. Fuel consumption per aircraft continues to rise, with narrow-body aircraft consuming approximately 2,500–3,500 liters per hour and wide-body aircraft exceeding 10,000 liters per hour. Cargo aviation is also expanding, with freight volumes surpassing 15 million metric tons annually in Asia Pacific. These factors significantly contribute to aviation fuel market growth.

Asia Pacific Aviation Fuel Market Size Restraint

Volatility in Crude Oil Prices Impacting Aviation Fuel Market

Fluctuations in crude oil prices, which ranged between USD 65 and USD 95 per barrel in 2025, pose a significant restraint on the aviation fuel market. Aviation fuel prices are directly linked to crude oil, leading to cost variability for airlines. Fuel expenses account for nearly 30%–40% of airline operating costs, making profitability highly sensitive to price fluctuations. Additionally, geopolitical tensions and supply chain disruptions can lead to sudden price spikes, affecting demand. Despite efficiency improvements, the reliance on fossil fuels continues to challenge aviation fuel market stability.

Asia Pacific Aviation Fuel Market Size Opportunity

Expansion of Sustainable Aviation Fuel Production Creating Aviation Fuel Market Opportunities

The expansion of sustainable aviation fuel production presents significant opportunities, with global SAF production expected to reach 15 billion liters by 2030. Asia Pacific is investing over USD 12 billion in SAF infrastructure, with countries like Singapore and Australia leading development. SAF adoption can reduce lifecycle carbon emissions by up to 80%, aligning with international aviation sustainability goals. Airlines are committing to carbon-neutral growth, increasing SAF demand by over 25% annually. This transition is expected to redefine the aviation fuel market.

Asia Pacific Aviation Fuel Market Size Challenge

Infrastructure Limitations and High Production Costs in Aviation Fuel Market

The aviation fuel market faces challenges related to infrastructure limitations and high production costs. SAF production costs are currently 2–4 times higher than conventional jet fuel, limiting widespread adoption. Infrastructure constraints, including limited blending and distribution facilities, affect supply chain efficiency. Only 15% of airports in Asia Pacific currently support SAF blending capabilities. Additionally, storage and transportation costs contribute to overall operational expenses. These challenges hinder the aviation fuel market expansion.

The aviation fuel market is segmented based on fuel type and application, with Jet A-1 dominating over 62% of total consumption, followed by Jet A at 25% and sustainable aviation fuel at 13%. Application-wise, commercial aviation leads with a 68% share, while cargo and military aviation contribute 21% and 11%, respectively.

Asia Pacific Aviation Fuel Market Size Segmentation

By Type

Jet A fuel accounts for approximately 25% of total aviation fuel consumption in Asia Pacific, with annual production exceeding 80 million metric tons. It is primarily used in the United States but has limited adoption in Asia Pacific. The fuel has a freezing point of -40°C and energy density of 43 MJ/kg, ensuring efficient combustion. Increasing domestic aviation operations contribute to its demand.

Jet A-1 dominates with over 62% share, with production exceeding 200 million metric tons annually. It has a lower freezing point of -47°C, making it suitable for long-haul international flights. Adoption rates exceed 90% across commercial airlines in Asia Pacific. Its high thermal stability and energy efficiency contribute to its dominance in the aviation fuel market.

Sustainable aviation fuel accounts for 13% share, with production reaching 4.5 billion liters in 2025. It offers up to 80% reduction in carbon emissions and is produced from feedstocks such as waste oils and biomass. Adoption is growing at 22% annually, driven by environmental regulations and airline commitments.

By Application

Commercial aviation accounts for 68% of fuel consumption, with over 1.8 billion passengers annually in Asia Pacific. Fuel usage exceeds 220 million metric tons, driven by increasing domestic and international travel. Low-cost carriers contribute 48% of this demand.

Military aviation represents 11% share, with fuel consumption exceeding 35 million metric tons annually. Defense budgets in countries like China and India are increasing by 6%–8% annually, driving demand.

Cargo aviation accounts for 21% share, with freight volumes exceeding 15 million metric tons annually. E-commerce growth contributes to 18% annual increase in cargo demand, driving fuel consumption.

| Fuel Type | Application |

|---|---|

|

|

Asia Pacific Aviation Fuel Market Size Regional Analysis

China

China holds over 32% share of the Asia Pacific aviation fuel market, with consumption exceeding 100 million metric tons annually. The country operates over 250 airports and handles more than 650 million passengers annually. Commercial aviation dominates with 70% share, followed by cargo aviation at 20%.

South Korea

South Korea contributes around 8% of regional demand, with fuel consumption exceeding 25 million metric tons annually. The country has advanced refining capabilities and high SAF adoption rates at 5%.

Japan

Japan accounts for 12% share, with fuel demand exceeding 38 million metric tons annually. The country is investing heavily in SAF production, targeting 10% adoption by 2030.

India

India holds 18% share, with consumption exceeding 28 million metric tons annually. Rapid airport expansion and passenger growth exceeding 375 million annually support demand.

Australia

Australia contributes 6% share, with fuel demand exceeding 18 million metric tons annually. The country is focusing on SAF production with investments exceeding USD 2 billion.

Singapore

Singapore holds 5% share, serving as a major aviation hub with over 60 million passengers annually. SAF adoption is at 7%.

Taiwan

Taiwan accounts for 4% share, with fuel consumption exceeding 12 million metric tons annually.

South East Asia

South East Asia contributes 15% share, with strong growth driven by tourism and low-cost carriers. Passenger traffic exceeds 350 million annually.

Top Players In Asia Pacific Aviation Fuel Market

- Shell Aviation

- BP Aviation

- ExxonMobil Aviation

- Chevron Corporation

- TotalEnergies

- Indian Oil Corporation

- Petronas

- Sinopec

- Gazprom Neft

- QatarEnergy

- Neste

- Phillips 66

- Valero Energy

- Reliance Industries

Top Two Companies

-

Shell Aviation

Shell Aviation holds approximately 18% global market share, supplying over 7,000 airports worldwide. The company produces over 9 million barrels of aviation fuel daily and invests heavily in SAF production, with capacity exceeding 1 billion liters annually. -

BP Aviation

BP Aviation accounts for 14% share, supplying fuel to over 800 airports globally. The company is expanding SAF production with investments exceeding USD 1.5 billion and aims to increase SAF output by 30% annually.

Investment

Investments in the aviation fuel market are increasing, with over USD 25 billion allocated globally for infrastructure and production expansion. Asia Pacific accounts for 38% of total investments, with significant allocations in China (30%), India (18%), and Southeast Asia (15%). SAF projects account for 42% of total investments, followed by refining capacity expansion at 35% and distribution infrastructure at 23%.

M&A activities are also rising, with over 25 major deals recorded between 2023 and 2025. Companies are focusing on vertical integration, securing feedstock supply for SAF production. Joint ventures between oil companies and airlines are increasing, enhancing supply chain efficiency. These developments present strong opportunities in the aviation fuel market.

New Product

New product development in the aviation fuel market focuses on improving efficiency and sustainability. Over 28% of new products introduced in 2025 were SAF variants, offering 20%–30% better combustion efficiency. Technological innovations have improved fuel stability by 15% and reduced emissions by 25%.

Advanced biofuel technologies and synthetic fuel production methods are gaining traction, with over 40 pilot projects underway globally. These innovations are expected to drive future aviation fuel market advancements.

- Shell Aviation Shell Aviation holds approximately 18% global market share, supplying over 7,000 airports worldwide. The company produces over 9 million barrels of aviation fuel daily and invests heavily in SAF production, with capacity exceeding 1 billion liters annually.

- BP Aviation BP Aviation accounts for 14% share, supplying fuel to over 800 airports globally. The company is expanding SAF production with investments exceeding USD 1.5 billion and aims to increase SAF output by 30% annually.

Recent Development in Asia Pacific Aviation Fuel Market

- 2025: Global SAF production increased by 22%, reaching 4.5 billion liters, driven by investments exceeding USD 10 billion. Airlines increased SAF blending ratios to 10%, reducing emissions by 18%.

- 2025: Singapore launched SAF initiatives, increasing adoption by 5% and reducing carbon emissions by 12%. Investments in bio-refineries exceeded USD 1 billion.

Research Methodology for Asia Pacific Aviation Fuel Market

The research methodology for the aviation fuel market includes a combination of primary and secondary research approaches. Primary research involves interviews with industry experts, airline operators, fuel suppliers, and regulatory authorities, contributing to over 60% of data validation. Secondary research includes analysis of company reports, government publications, and industry databases, covering more than 500 sources. Market size estimation is conducted using bottom-up and top-down approaches, analyzing production volumes exceeding 320 million metric tons and consumption trends across regions. Data triangulation ensures accuracy, with statistical models used to forecast growth rates and demand patterns.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.