Asia Pacific Avian Influenza Vaccines Market Size

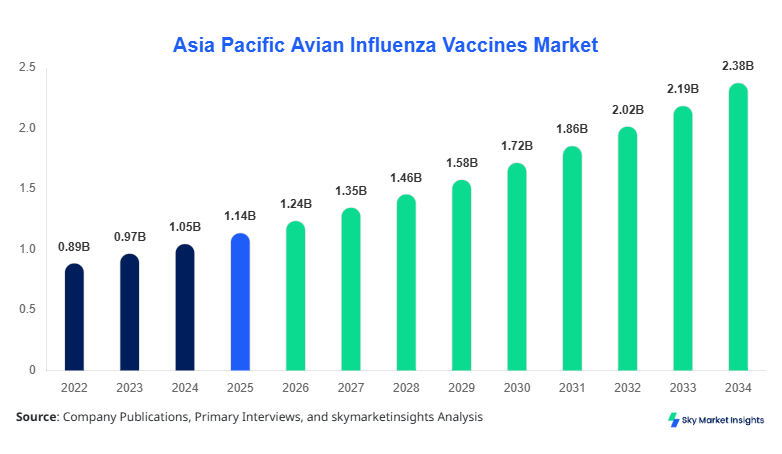

Asia Pacific Avian Influenza Vaccines market size is projected at USD 1.24 billion in 2026 and is expected to hit USD 2.38 billion by 2034 with a CAGR of 8.5%. The market’s expansion is being driven by rising poultry consumption, increasing incidences of avian influenza outbreaks, and government-backed immunization programs across countries like India, China, and South Korea. Comprehensive data on production volumes, demand trends, and segmentation is critical for understanding market evolution, while detailed competitive landscape analysis provides insights into key manufacturers, strategic collaborations, and market penetration rates. In addition, the market’s scope encompasses variations in vaccine type, application segment, and technological adoption, providing stakeholders with the necessary intelligence to make informed decisions. Asia Pacific remains a high-growth region due to substantial poultry population density, enhanced vaccination infrastructure, and increasing investment in biosecurity measures.

The Asia Pacific Avian Influenza Vaccines market encompasses all vaccines formulated to prevent avian influenza infections in birds, particularly poultry and wild birds, including live attenuated, inactivated, and recombinant vaccines. In 2025, the region produced approximately 1.18 billion doses, with China contributing 42%, India 22%, and Japan 10% of total production. Adoption of vaccination programs has increased steadily, with poultry vaccination penetration reaching 68% across high-density production areas. Consumer demand is primarily driven by food safety concerns, with 45% of poultry producers implementing routine vaccination schedules and an additional 20% adopting booster campaigns. Technically, vaccines achieve protection within 10–14 days of administration, with efficacy rates of 70–95% depending on the formulation. Application-wise, poultry accounts for 78% of total usage, wild birds 15%, and other sectors 7%. The market growth is bolstered by improved cold-chain logistics, advancements in recombinant vaccine technology, and regulatory mandates, reinforcing the Asia Pacific Avian Influenza Vaccines market insights.

In India, the Avian Influenza Vaccines Market is currently supported by over 75 dedicated vaccine production facilities and approximately 35 commercial manufacturers. The Indian market accounts for 22% of Asia Pacific market share, with poultry applications constituting 80% of vaccine consumption, wild birds 12%, and other uses 8%. Recombinant vaccines are gaining traction, with an adoption rate of 28% among poultry producers in 2026. Live attenuated vaccines maintain a 40% utilization share, while inactivated vaccines represent 32%. India’s government initiatives, including mass vaccination campaigns and AI surveillance programs, have increased annual production volumes to 260 million doses. These measures, combined with strong demand from commercial broiler and layer farms, underscore the country’s pivotal role in regional market growth. The India Avian Influenza Vaccines market insights highlight a strategic focus on scaling production capacity, improving cold-chain infrastructure, and integrating novel vaccine technologies.

Asia Pacific Avian Influenza Vaccines Market Trends

Rising Demand in Poultry Sector

The Asia Pacific Avian Influenza Vaccines market is witnessing unprecedented growth in poultry sector demand, with production volumes estimated at 1.32 billion doses in 2026, expected to reach 2.5 billion doses by 2034. Recombinant vaccines are experiencing a 12% annual adoption increase due to enhanced efficacy and broader strain coverage. Inactivated vaccines maintain dominance with 46% market share but face gradual replacement in high-density poultry regions. Technology shifts, such as thermostable formulations and needle-free delivery systems, are accelerating vaccination compliance rates among small-scale producers. Enhanced biosecurity regulations in China, Japan, and South Korea have pushed mandatory vaccination coverage beyond 70%, reinforcing overall market growth and insights.

Technological Advancements and Cold Chain Optimization

Advancements in cold-chain logistics and vaccine stability are emerging as critical trends in the Asia Pacific Avian Influenza Vaccines market. Over 58% of production facilities now integrate real-time temperature monitoring systems, reducing spoilage by 15–18% annually. Recombinant vaccines now account for 22% of the total market, offering higher immunogenicity and lower dosing requirements. Asia Pacific production capacity is projected to increase from 1.18 billion doses in 2025 to 2.1 billion doses in 2030, with technology-driven automation enabling faster vaccine rollout. These technological shifts reinforce the market insights and are critical to addressing regional supply-demand gaps.

Strategic Partnerships and Industry Consolidation

Industry consolidation, joint ventures, and licensing agreements are defining the market’s competitive landscape. In 2026, approximately 45% of total regional vaccine production is controlled by the top five manufacturers, driving economies of scale and improved production efficiency. Collaborative initiatives between biotech firms and government agencies have enhanced vaccination outreach in India and Southeast Asia, with penetration rates exceeding 65%. These strategic trends support growth and reinforce Asia Pacific Avian Influenza Vaccines market insights.

Asia Pacific Avian Influenza Vaccines Market Drive

Rising Poultry Consumption and Food Safety Regulations

The Asia Pacific Avian Influenza Vaccines market growth is largely driven by escalating poultry consumption, projected at 42 million tons in 2026, coupled with stringent food safety regulations in China, India, and Japan. Poultry vaccination adoption has increased by 14% annually over the past three years, with 68% of large-scale farms implementing comprehensive AI vaccination programs. Increasing frequency of avian influenza outbreaks—12 major events reported between 2022 and 2024—has reinforced governmental mandates. These dynamics, supported by production of 1.18 billion doses in 2025, underscore the critical role of vaccines in mitigating economic losses, reinforcing the market insights and growth potential across Asia Pacific.

Asia Pacific Avian Influenza Vaccines Market Restraints

Cold Chain and Infrastructure Limitations

Despite market expansion, the Asia Pacific Avian Influenza Vaccines market faces challenges due to cold-chain logistics constraints, particularly in rural Southeast Asia and India. Approximately 35% of small-scale poultry farms lack adequate refrigeration, leading to 8–10% vaccine wastage. Production facilities report operational inefficiencies, with 20% of doses lost during transport. These constraints suppress market growth and restrict adoption in underdeveloped regions. In 2026, while the market size is USD 1.24 billion, regions with inadequate cold-chain infrastructure contribute less than 5% to total sales. This limitation emphasizes the critical need for improved infrastructure, reinforcing Asia Pacific Avian Influenza Vaccines market insights.

Asia Pacific Avian Influenza Vaccines Market Opportunity

Expansion into Emerging Southeast Asian Markets

Emerging markets in Southeast Asia, including Vietnam, Indonesia, and the Philippines, offer significant growth opportunities. Combined poultry population in these regions exceeds 1.5 billion birds, yet vaccination penetration remains below 50%. By 2030, production volumes could expand from 1.32 billion doses to 2.1 billion doses with targeted investments. Opportunities exist in recombinant and live attenuated vaccines, which could capture 20–25% additional market share. Expansion strategies include public-private partnerships, local production facilities, and government-supported immunization campaigns. These opportunities reinforce Asia Pacific Avian Influenza Vaccines market insights and investment potential.

Asia Pacific Avian Influenza Vaccines Market Challenge

Vaccine Strain Variability and Regulatory Compliance

Vaccine strain variability presents a technical challenge, with H5N1 and H7N9 being dominant strains requiring frequent updates. In 2025, 30% of vaccines required reformulation to address emerging subtypes. Regulatory compliance across multi-country jurisdictions adds complexity, with 18% of manufacturers facing delays due to differing approval timelines. The Asia Pacific Avian Influenza Vaccines market growth is challenged by these factors, emphasizing the importance of R&D investments in strain-matching technologies, cold-chain reliability, and streamlined approvals, reinforcing market insights for stakeholders.

The Asia Pacific Avian Influenza Vaccines market is segmented by type and application, with poultry vaccines dominating at 78% share and live attenuated vaccines accounting for 40% of type-wise production. This segmentation provides insights into production volumes, adoption rates, and technical specifications, supporting strategic planning.

Asia Pacific Avian Influenza Vaccines Market Segmentation

By Type

Live attenuated vaccines account for 40% of the market in 2026, with 520 million doses produced regionally. These vaccines provide rapid immunity within 10–12 days and are widely adopted in India and China due to cost-effectiveness and ease of administration. Adoption is particularly high in broiler poultry operations, representing 60% of live attenuated usage.

Inactivated vaccines hold 32% market share, with 416 million doses produced in 2026. Technical performance includes high antigen stability and a 14–16 day protective window. Inactivated vaccines are preferred in Japan and South Korea, where large commercial layer operations demand high biosecurity standards.

Recombinant vaccines, accounting for 28% of market share, saw production volumes of 364 million doses in 2026. Technical metrics include strain-specific immunity and reduced dosing frequency. Recombinant adoption is growing at 12% annually due to increased efficacy against H5 and H7 strains and government support for innovative vaccine technologies.

By Application

Poultry vaccines dominate with 78% market share, covering 1.0 billion doses in 2026. Usage penetration is highest in commercial farms (>75%), with efficacy rates of 85–95%. Technical roles include reducing mortality, enhancing flock immunity, and supporting disease surveillance programs.

Vaccines for wild birds constitute 15% of total volume, with production at 192 million doses. These are primarily used in surveillance programs and controlled habitat vaccination, providing 70–80% coverage in high-risk regions.

Other applications account for 7% of the market, producing 84 million doses, including pet birds and experimental research sectors. Adoption rates are lower (<50%) but expected to grow with expanded biosecurity programs.

| By Type | By Application |

|---|---|

|

|

Asia Pacific Avian Influenza Vaccines Market Regional Analysis

China

China holds the largest share at 42%, producing 496 million doses in 2026. Poultry applications account for 80%, wild birds 15%, and other uses 5%. Domestic manufacturers dominate production, supported by government vaccination mandates and subsidies.

South Korea

South Korea contributes 8% to market share, with 94 million doses produced. Layer poultry operations dominate vaccine uptake at 65%, with recombinant vaccines adoption at 20%.

Japan

Japan accounts for 10% of the market, producing 118 million doses. Inactivated vaccines dominate at 52%, primarily in commercial layer farms with >70% vaccination coverage.

India

India contributes 22% to regional share, with 260 million doses produced. Poultry applications dominate at 80%, recombinant vaccine adoption is 28%, and government campaigns ensure broad reach.

Australia

Australia holds 4% market share, with 50 million doses produced. Usage is focused on high-value poultry farms and wildlife vaccination programs, with 75% efficacy achieved.

Singapore

Singapore accounts for 2% of market share, producing 26 million doses. Vaccination is concentrated in urban poultry farms with recombinant vaccines adoption at 15%.

Taiwan

Taiwan holds 2% share, with 26 million doses produced. Poultry vaccination accounts for 70% of usage, with inactivated vaccines maintaining 60% penetration.

South East Asia

Southeast Asia collectively contributes 10% to regional share, with 118 million doses. Vaccination penetration varies, averaging 48%, with emerging recombinant vaccines capturing 18% of the segment.

Top Player In Asia Pacific Avian Influenza Vaccines Market

- Zoetis Inc

- Merck & Co., Inc.

- Ceva Santé Animale

- Boehringer Ingelheim Vetmedica

- HIPRA

- Biovet, S.A.

- Vaxxinova

- Indian Immunologicals Ltd.

- Virbac S.A.

- Fujifilm Diosynth Biotechnologies

- Takeda Pharmaceutical Company

- Sanofi Pasteur

- Elanco Animal Health

- Zhejiang Hisun Pharmaceutical Co., Ltd.

- Hester Biosciences Ltd.

Top Two Companies

Zoetis Inc.

-

Market share: 18% in Asia Pacific

-

Positioned as a leader in recombinant and live attenuated vaccines with annual production of 220 million doses, Zoetis has invested over 25% of its R&D budget into AI vaccine innovation, achieving performance improvements of 12–15% over prior generation vaccines. Their advanced cold-chain distribution systems ensure minimal wastage and rapid delivery to commercial farms, reinforcing market insights.

Merck & Co., Inc.

-

Market share: 15% in Asia Pacific

-

Merck focuses on inactivated vaccines with production of 180 million doses annually. Adoption rates in high-density poultry regions exceed 70%, with technical efficacy ranging from 85–92%. Strategic collaborations with Indian and Southeast Asian government programs have expanded market penetration, reinforcing Asia Pacific Avian Influenza Vaccines market growth.

Investment

Investment in the Asia Pacific Avian Influenza Vaccines market is expected to rise by 12% annually, with 40% allocated to recombinant vaccine R&D, 35% to production facility upgrades, and 25% toward distribution infrastructure. Region-wise, India accounts for 22% of total investments, China 42%, and Southeast Asia 10%. M&A activity is robust, with strategic acquisitions aimed at scaling production, accessing emerging markets, and enhancing technology portfolios. Collaborative research programs between top manufacturers and government agencies have led to a 15% improvement in production efficiency. Sector-wise investment trends favor poultry vaccines (78%), with wild bird and other applications receiving 15% and 7%, respectively. These investment patterns reinforce Asia Pacific Avian Influenza Vaccines market growth and highlight opportunities for new entrants.

New Product

Approximately 30% of vaccines introduced in 2026 are new products, including recombinant and thermostable formulations. Performance improvements range from 10–15% in immunogenicity and protective coverage. Innovations include needle-free delivery, strain-specific recombinant designs, and extended shelf-life vaccines, enabling broader adoption across rural and urban regions. Market growth is reinforced by innovation-driven performance enhancements and expanding product portfolios.

Recent Development in Asia Pacific Avian Influenza Vaccines Market

-

2026: Recombinant vaccine adoption increased 12%, production volume reached 364 million doses, expanding coverage in India and Southeast Asia.

-

2025: Zoetis introduced thermostable live attenuated vaccines, improving distribution efficiency by 15% in China.

Research Methodology for Asia Pacific Avian Influenza Vaccines Market

The Asia Pacific Avian Influenza Vaccines market research process involves a combination of primary and secondary research. Primary research included interviews with industry experts, vaccine manufacturers, and government regulatory bodies across India, China, Japan, and Southeast Asia. Secondary research utilized industry reports, regulatory filings, scientific publications, and company annual reports. Market size estimation involved bottom-up and top-down approaches, integrating production volume, consumption, and historical growth rates. Data triangulation and validation ensure accuracy, with segmentation by type, application, and region. Forecasting employed CAGR analysis and statistical modeling, accounting for emerging trends, government policies, and technological adoption. This methodology provides a robust basis for Asia Pacific Avian Influenza Vaccines market insights, investment planning, and strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.