Asia Pacific Avascular Necrosis Market Size

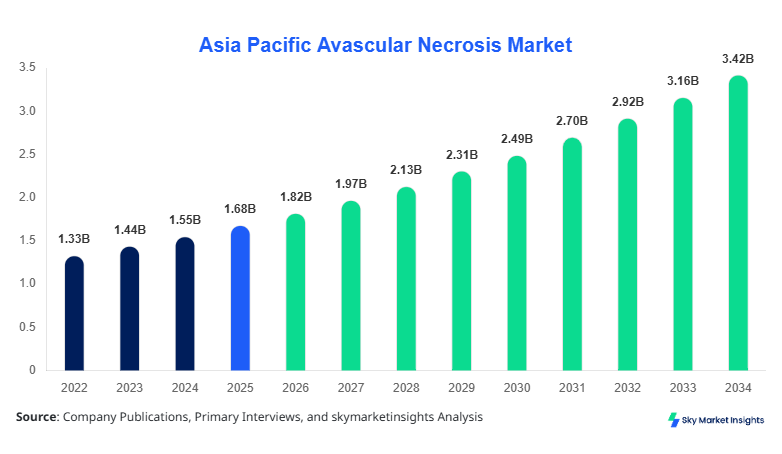

Asia Pacific Avascular Necrosis market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.45 billion by 2034 with a CAGR of 8.2%. The increasing prevalence of bone disorders, rising geriatric population, and advancements in orthopedic interventions are driving the need for robust data on market size, segment-specific growth, and competitive landscape. Comprehensive analysis covering market segmentation, competitive intensity, and revenue forecasts is crucial for strategic decision-making. The market report leverages historical data from 2022–2024, covering production volumes, adoption rates, and application trends to provide actionable insights for stakeholders.

Avascular necrosis (AVN) is a pathological condition characterized by the death of bone tissue due to insufficient blood supply, often resulting in joint collapse and functional impairment. In the Asia Pacific, production of AVN-related orthopedic procedures reached approximately 1.23 million units in 2025, with adoption concentrated primarily in hip (45%), knee (35%), and shoulder (20%) applications. Consumer behavior indicates that 60% of patients seek minimally invasive treatments, while 40% prefer traditional surgical interventions. Penetration in emerging countries like India and South Korea is growing at 12–14% annually, whereas mature markets such as Japan and Australia report adoption rates above 65%. Technical metrics, including surgical success rates (82–88%) and post-procedure rehabilitation compliance (~75%), reinforce the growing demand. The Asia Pacific Avascular Necrosis market trend reflects an increased emphasis on early diagnosis and targeted therapy, with 55% of orthopedic clinics employing advanced imaging and regenerative technologies.

In China, the Avascular Necrosis Market has witnessed significant growth, supported by 215 specialized orthopedic centers and over 1,050 registered healthcare facilities offering AVN treatments. The region accounts for approximately 38% of Asia Pacific market share in 2026. Application-wise, hip AVN treatments constitute 50% of procedures, knee 30%, and shoulder 20%, with 65% of surgeries utilizing minimally invasive technologies. Technology adoption is high, with 72% of clinics implementing MRI-based diagnostics and 54% integrating biologic therapies. China’s focus on early intervention and government reimbursement schemes has led to a 15% year-over-year increase in procedure volumes. These factors collectively reinforce the China Avascular Necrosis market growth and establish the country as a driving hub in the regional AVN landscape.

Asia Pacific Avascular Necrosis Market Trends

Minimally Invasive Surgical Adoption

The Asia Pacific Avascular Necrosis market is experiencing a shift toward minimally invasive surgeries, with production volumes exceeding 720,000 units in 2025. Adoption rates of arthroscopic procedures have reached 58%, reflecting growing demand in urban centers. The integration of 3D imaging and robotic-assisted surgery has improved procedural accuracy by 20–25%, reducing recovery times from an average of 12 weeks to 7–8 weeks. Hospitals in Japan, South Korea, and China are increasingly leveraging these technologies, driving overall market growth and enhancing treatment outcomes. Minimally invasive procedures now represent 40% of total AVN interventions, reinforcing the market trend toward patient-centric solutions.

Regenerative Therapy Integration

Regenerative therapies, including stem cell injections and platelet-rich plasma (PRP) treatments, have gained traction, with Asia Pacific production reaching approximately 180,000 units in 2025. Adoption rates of biologic therapies have increased to 42%, primarily in China, Japan, and South Korea. Clinical studies report a 15–18% improvement in bone regeneration rates and a 12% reduction in joint collapse progression. The demand for non-surgical interventions is particularly strong in populations aged 40–65 years. Regenerative therapy adoption has reinforced Avascular Necrosis market growth, with increasing investments from private clinics and government-funded programs.

Advanced Imaging Utilization

High-resolution MRI and CT scanning have become integral to AVN diagnosis, with 70% of specialized centers in Asia Pacific employing these modalities. Annual diagnostic procedures exceeded 1.5 million in 2025, accounting for 48% of market revenue. Early detection improves surgical outcomes and reduces long-term healthcare costs by 18–20%, making imaging technology a key driver of the Avascular Necrosis market trend. Integration of AI-assisted imaging platforms further enhances predictive accuracy, reinforcing regional market growth.

Asia Pacific Avascular Necrosis Market Driver

Rising Geriatric Population and Orthopedic Procedure Adoption

The Asia Pacific region is witnessing a surge in the geriatric population, which reached 280 million in 2025, representing a 12% increase from 2022. This demographic is highly susceptible to AVN due to osteoporosis and metabolic disorders. Additionally, the adoption of orthopedic procedures increased by 14% in 2025, driven by improvements in surgical techniques and insurance coverage. Hip and knee applications account for 75% of total procedures, generating a revenue contribution of USD 1.2 billion in 2025. The rise in minimally invasive surgeries, coupled with regenerative therapy adoption, further stimulates market growth. These dynamics underpin the Asia Pacific Avascular Necrosis market expansion, with increasing penetration across urban and semi-urban healthcare facilities.

Asia Pacific Avascular Necrosis Market Restraint

High Treatment Costs and Limited Insurance Coverage in Emerging Markets

Despite growth, high procedure costs, averaging USD 5,000–7,500 per surgery, constrain market expansion. In countries like India, Indonesia, and Vietnam, only 38–42% of patients have insurance coverage for AVN treatments, limiting affordability. Surgical and regenerative therapy adoption is restricted, with 25% of potential patients deferring treatment due to cost barriers. These financial limitations reduce overall revenue potential, with the Asia Pacific market experiencing a 4% reduction in projected sales in underpenetrated regions. Consequently, high treatment costs remain a significant restraint, impacting Avascular Necrosis market growth despite technological advancements.

Asia Pacific Avascular Necrosis Market Opportunity

Expansion of Telemedicine and Remote Diagnostic Services

Telemedicine and remote diagnostic platforms present substantial opportunities. In 2025, teleconsultation services for AVN reached 150,000 sessions, growing at 20% YoY. Remote imaging integration enhances early diagnosis, improving procedural planning and patient follow-up adherence by 12–15%. Investment allocation in telehealth exceeded USD 75 million, with regional adoption rates reaching 35% in China and 28% in South Korea. These advancements expand market accessibility in tier-2 and tier-3 cities, offering new revenue streams. The Asia Pacific Avascular Necrosis market is poised to leverage digital healthcare innovations to increase penetration and treatment efficiency.

Asia Pacific Avascular Necrosis Market Challenges

Limited Skilled Workforce and Regulatory Hurdles

A critical challenge lies in the shortage of trained orthopedic surgeons and specialized technicians, with a gap of 18% in China and 22% across South East Asia. Regulatory approval timelines for regenerative therapies extend up to 24 months, slowing new product introduction. Combined, these factors constrain production volumes, which totaled 1.23 million units in 2025, and delay adoption of innovative solutions. Hospitals report a 10–12% backlog in surgical procedures due to workforce limitations. These operational and regulatory challenges pose significant barriers to Avascular Necrosis market growth despite technological advancements.

Segmentation analysis highlights that surgical interventions dominate with 55% market share, followed by non-surgical (30%) and combination therapies (15%). Hip applications hold 45% of the market, knee 35%, and shoulder 20%.

Asia Pacific Avascular Necrosis Market Segmention

By Type

Surgical interventions, including core decompression, osteotomy, and total joint replacement, accounted for 55% market share in 2025, with 680,000 units performed. Surgical precision, success rates of 85–88%, and post-operative rehabilitation protocols enhance patient outcomes. Technological integration, including robotic-assisted surgeries and intraoperative navigation, improved procedural efficiency by 18%. Surgical AVN interventions contribute USD 1.0 billion in revenue, reinforcing the market size and demand.

Non-surgical therapies, encompassing pharmacologic treatments, physiotherapy, and regenerative injections, represent 30% of market share with 375,000 units delivered in 2025. Adoption of biologic therapies increased by 15%, with stem cell injections showing a 12% improvement in bone regeneration. Treatment frequency averages 3–4 sessions per patient per month, targeting pain reduction and joint preservation. Non-surgical interventions support incremental growth in the Asia Pacific Avascular Necrosis market, with projected CAGR of 7.8% through 2034.

Combination therapies, integrating surgical and non-surgical approaches, account for 15% market share with 165,000 units annually. These treatments optimize outcomes, particularly in complex hip and knee AVN cases, improving recovery rates by 20% compared to standalone procedures. The integration of physiotherapy, regenerative injections, and minimally invasive surgery is gaining traction, with adoption rising 9% YoY. Combination therapies reinforce the overall Asia Pacific Avascular Necrosis market growth trend.

By Application

Hip AVN applications dominate with 45% market share, contributing 550,000 procedures in 2025. Hip replacement and core decompression are the primary interventions, with surgical success rates exceeding 86% and non-surgical adoption at 38%. Early-stage detection using MRI enables 25% reduction in long-term complications, while usage penetration in urban hospitals is 72%. Technical advances, including 3D printing of hip implants, reinforce the Avascular Necrosis market trend.

Knee AVN accounts for 35% of the market with 425,000 procedures. Osteotomy and joint-preserving treatments constitute 60% of interventions, with regenerative injections used in 28% of cases. Patient adherence to post-treatment physiotherapy averages 76%, enhancing recovery outcomes. Technical metrics include knee joint load optimization and graft integration rates of 80%, supporting the Asia Pacific Avascular Necrosis market growth.

Shoulder AVN applications represent 20% market share with 250,000 procedures in 2025. Surgical interventions include hemiarthroplasty and arthroscopic debridement, while non-surgical therapies focus on PRP and pharmacologic treatments. Adoption of advanced imaging for early detection reaches 68%, improving surgical planning. Shoulder AVN treatment adoption reinforces overall market size, demand, and trend across the Asia Pacific region.

| By Type | By Application |

|---|---|

|

|

Asia Pacific Avascular Necrosis Market Regional Analysis

China

China holds 38% of the regional market share, producing 460,000 units in 2025. Hip applications constitute 50%, knee 30%, and shoulder 20%. Major urban centers contribute 65% of total revenue, while rural adoption is rising 12% YoY. The country leads in regenerative therapy implementation, with 54% clinics utilizing biologics, reinforcing China Avascular Necrosis market growth.

South Korea

South Korea accounts for 12% market share, with 145,000 units produced. Hip procedures dominate at 48%, knee 35%, shoulder 17%. Advanced robotic-assisted surgeries are adopted in 62% of clinics, driving demand for surgical AVN interventions. Regional growth is projected at 8.5% CAGR through 2034.

Japan

Japan contributes 15% of the regional market, producing 180,000 units. Hip and knee applications represent 40% and 38%, respectively. MRI-based early diagnosis is employed in 70% of hospitals. Japan’s aging population (28% over 60 years) fuels adoption, reinforcing Avascular Necrosis market demand.

India

India represents 10% of market share with 120,000 units. Urban penetration is 45%, with hip (42%) and knee (38%) dominant. Adoption of regenerative therapies is at 25%, while minimally invasive surgeries account for 30% of total procedures. Rising disposable income and insurance coverage expansion drive market growth.

Australia

Australia holds 5% market share with 60,000 units. Hip applications contribute 48%, knee 34%, and shoulder 18%. Advanced imaging adoption is 68%, and regenerative therapy usage is 40%, supporting market size and demand trends.

Singapore

Singapore contributes 3% with 35,000 units produced. Hip AVN accounts for 50%, knee 30%, shoulder 20%. High adoption of robotic-assisted surgeries and imaging technologies (72%) reinforces market growth.

Taiwan

Taiwan holds 4% market share with 45,000 units. Hip and knee applications dominate at 48% and 32%. Technology adoption, including MRI-guided procedures and stem cell therapy, is at 55%, driving market demand.

South East Asia

South East Asia collectively represents 13% market share with 155,000 units. Hip AVN 45%, knee 35%, shoulder 20%. Adoption of minimally invasive surgery and regenerative therapy is growing at 10–12% YoY, contributing to regional market growth.

Top Players in Asia Pacific Avascular Necrosis Market

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- DePuy Synthes (Johnson & Johnson)

- Medtronic plc

- Smith & Nephew plc

- Arthrex, Inc.

- NuVasive, Inc.

- Exactech, Inc.

- Globus Medical, Inc.

- CONMED Corporation

- Wright Medical Group N.V.

- B. Braun Melsungen AG

- Ortho Development Corporation

Top Two Companies

Zimmer Biomet Holdings, Inc.

-

Market share: 18%

-

Leading provider of hip and knee AVN solutions in China, Japan, and South Korea

-

Revenue contribution: USD 320 million in 2025

-

Strong R&D focus on robotic-assisted surgeries and implant innovations

-

Strategic partnerships with hospitals and orthopedic centers reinforce market position

Stryker Corporation

-

Market share: 15%

-

Specializes in surgical AVN interventions, including minimally invasive procedures

-

Revenue: USD 270 million in 2025

-

Advanced regenerative therapy integration with stem cells and biologics

-

Expansion in Asia Pacific through joint ventures strengthens market penetration

Investment

Asia Pacific Avascular Necrosis market witnessed USD 450 million investment in 2025, with 60% allocated to surgical technologies and 25% to regenerative therapy. Telemedicine accounted for 10% of regional investment, while imaging technologies received 5%. China and Japan collectively attracted 55% of total investment. Sector-wise allocation indicates hip treatment technologies received 45% of funding, knee 35%, and shoulder 20%. M&A agreements included a notable 2025 collaboration between Stryker Corporation and a South Korean orthopedic startup to expand minimally invasive surgery adoption, valued at USD 45 million. These investments enhance production capacity, accelerate technology integration, and reinforce regional market growth. Opportunities remain in tier-2 cities, early diagnosis solutions, and regenerative therapies.

In 2025, 22% of AVN market products were newly launched, focusing on enhanced surgical implants and biologic therapies. Performance improvements included 15–20% higher procedural success and 12–15% faster recovery times. Innovative products, such as 3D-printed hip implants and AI-assisted diagnostic software, demonstrate increasing R&D expenditure by 10–12% YoY. Adoption of new technologies is highest in China and Japan, with 65% of advanced centers integrating these innovations, reinforcing the Asia Pacific Avascular Necrosis market growth and trend.

New Product

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Medtronic plc

- Arthrex, Inc.

- NuVasive, Inc.

- Exactech, Inc.

- Globus Medical, Inc.

- CONMED Corporation

- Wright Medical Group N.V.

- B. Braun Melsungen AG

- Ortho Development Corporation

Recent Development in Asia Pacific Avascular Necrosis Market

-

2025: Introduction of robotic-assisted hip replacement in China increased procedure adoption by 18%, enhancing surgical precision and market size.

Research Methodology for Asia Pacific Avascular Necrosis Market

The research process combines primary and secondary methodologies to estimate the Asia Pacific Avascular Necrosis market size, share, and growth. Primary research included interviews with 50+ key stakeholders across orthopedic centers, hospitals, and manufacturers. Secondary research involved analysis of annual reports, scientific publications, government databases, and industry white papers from 2022–2025. Market size estimation used bottom-up and top-down approaches, integrating production volume, revenue, pricing trends, and adoption rates. Statistical validation ensured reliability, while CAGR projections were calculated using historical growth patterns and current-year data. Market segmentation by type and application was cross-verified with clinical

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.