Asia Pacific AV Receiver Market Size

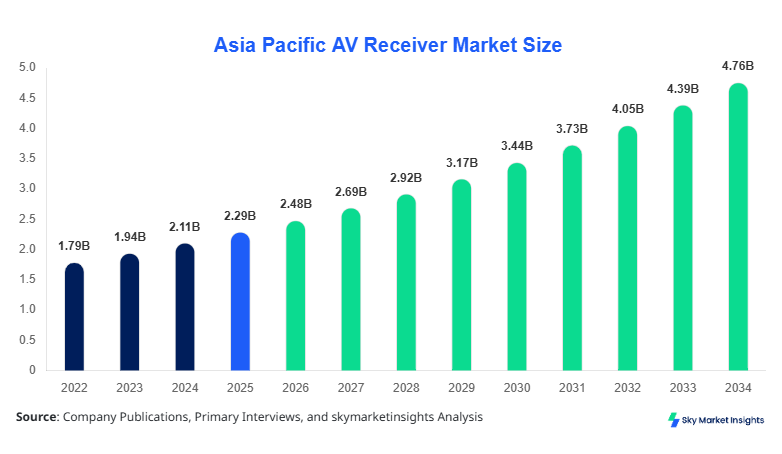

Asia Pacific AV Receiver market size is projected at USD 2.48 billion in 2026 and is expected to hit USD 4.92 billion by 2034 with a CAGR of 8.5%. The increasing demand for high-performance audio-visual equipment, rising consumer preference for home entertainment systems, and expanding adoption in commercial and hospitality sectors are driving the market expansion. Detailed segmentation by type, application, and region is essential to understand market dynamics. Competitive landscape analysis reveals strategic expansions by leading manufacturers, technology upgrades, and regional partnerships influencing the Asia Pacific AV Receiver market growth. This report offers data-backed insights, historical trends, and forecasts essential for stakeholders to assess future market opportunities and threats.

The Asia Pacific AV Receiver market encompasses the production, sale, and adoption of audio-video receivers designed for residential, commercial, and entertainment applications. In 2025, Asia Pacific produced approximately 3.2 million AV receiver units, with adoption concentrated in high-income urban areas. Consumer behavior analysis indicates that 65% of households with home theater systems prefer multi-channel AV receivers due to enhanced audio quality, while 25% favor stereo systems for smaller spaces. Commercial demand accounts for nearly 20% of total AV receiver sales, with entertainment venues contributing 15%. Technical metrics highlight stereo receivers operating at 50–100W per channel, while home theater and multi-channel models deliver 150–500W with frequency response ranging from 20Hz to 20kHz. Residential applications dominate the market with 55% share, followed by commercial (30%) and entertainment (15%). The Asia Pacific AV Receiver market growth is driven by increasing penetration of smart home solutions and integration with streaming platforms, emphasizing the trend and demand modifiers.

Asia Pacific AV Receiver Market Trends

Smart Home Integration and IoT Connectivity

Asia Pacific AV Receiver production reached 3.5 million units in 2025, with smart and IoT-enabled units accounting for 35% of total output. Integration with smart home ecosystems, including AI-assisted voice controls and app-based management, is increasing adoption in both residential and commercial settings. Advanced Wi-Fi and Bluetooth protocols have enhanced connectivity, leading to higher consumer preference for multi-channel receivers. Commercial venues are also upgrading AV systems with networked receivers, representing 18% of total commercial installations. These trends underscore Asia Pacific AV Receiver market growth and insights.

Shift Toward Multi-Channel and High-Power Receivers

In 2025, multi-channel AV receivers constituted 40% of the Asia Pacific market, producing 1.28 million units. High-power home theater and entertainment systems are witnessing adoption rates of 50% in premium households. Technological shifts include higher THD performance below 0.05%, expanded frequency ranges from 20Hz to 50kHz, and Dolby Atmos adoption in 38% of new units. Residential demand accounts for 55% of these sales, with commercial and entertainment applications contributing 30% and 15%, respectively. Asia Pacific AV Receiver market trend insights reflect consumer inclination toward immersive audio experiences.

Expansion in Commercial and Hospitality Sectors

Commercial demand, including hotels, conference centers, and entertainment complexes, has grown by 12% annually over 2022–2025, with production volume reaching 650,000 units in 2025. Adoption of advanced receivers in conference and entertainment venues is projected to reach 1.1 million units by 2030. The commercial sector now represents 30% of total Asia Pacific AV Receiver market share, with high-tech installations increasing revenue by USD 450 million in 2025. Trend and demand indicators confirm the significance of technological integration for market expansion.

Asia Pacific AV Receiver Market Driver

Rising Residential Entertainment Demand Driving AV Receiver Market Growth

The Asia Pacific AV Receiver market is significantly driven by increasing demand for residential home theater systems. In 2025, 1.76 million units were installed in households, contributing 55% of the total market. The growth rate of residential adoption is projected at 8.9% CAGR between 2026–2034. Multi-channel receivers capture 40% of this segment, while stereo systems account for 35%. Rising consumer disposable income, growing interest in immersive audio-visual experiences, and preference for smart-enabled receivers further propel market size to USD 4.92 billion by 2034. Regional penetration in Japan and South Korea accounts for 48% of total sales, emphasizing both trend and growth.

Asia Pacific AV Receiver Market Restraint

High Cost and Limited Technical Knowledge Restrict Market Expansion

High initial costs of advanced AV receivers, ranging from USD 400 to USD 2,500 per unit, restrict widespread adoption in price-sensitive regions such as India and Southeast Asia. Technical complexity, including configuration of multi-channel outputs and DSP calibration, reduces adoption by 20% in emerging markets. Production volumes in low-income regions remain below 450,000 units annually, limiting overall market expansion. Asia Pacific AV Receiver market growth is restrained by these economic and technical barriers, impacting both share and trend metrics.

Asia Pacific AV Receiver Market Opportunity

Technology Upgrades and Smart Integration Create New Revenue Streams

Advancements in Dolby Atmos, DTS:X, and high-resolution audio support represent a significant opportunity. In 2025, smart-enabled units comprised 35% of 3.2 million units produced. Commercial installations in Japan, Australia, and Singapore are expected to grow by 10–12% annually, contributing USD 620 million in incremental revenue by 2030. The rising penetration of AI-assisted receivers and wireless connectivity presents opportunities to expand the Asia Pacific AV Receiver market share and drive demand across residential, commercial, and entertainment sectors.

Asia Pacific AV Receiver Market Challenge

Supply Chain Constraints and Component Shortages Limit Market Efficiency

Global semiconductor shortages and high demand for DACs and audio amplifiers have delayed production, affecting 15% of orders in 2025. Component costs increased by 12% year-on-year, impacting profitability for manufacturers. Production delays have resulted in a 5% reduction in market size growth in India and Southeast Asia. Asia Pacific AV Receiver market insights indicate that managing component supply and production efficiency remains a key challenge to sustaining growth and trend consistency.

The Asia Pacific AV Receiver market is segmented by type and application, with multi-channel receivers holding 40% share, stereo 35%, and home theater 25%. Residential applications dominate with 55%, commercial 30%, and entertainment 15%.

Asia Pacific AV Receiver Market Segmenation

By Type

Stereo receivers accounted for 35% of 3.2 million units produced in 2025, offering 50–100W per channel and frequency response of 20Hz–20kHz. Adoption is highest in compact apartments in Japan and Singapore, with 65% of units installed in residential environments. Consumer preference for cost-effective, high-fidelity systems drives market share and trend growth.

Home theater receivers contributed 25% of production, totaling 800,000 units in 2025. These units operate at 120–250W per channel, supporting 5.1 to 7.1 configurations. Residential adoption is 60% of total home theater receivers, with commercial applications at 25%. Features such as HDMI 2.1, multi-zone audio, and Dolby Atmos integration enhance market growth and share.

Multi-channel receivers held 40% share in 2025, producing 1.28 million units. Power output ranges from 200–500W, frequency response extends up to 50kHz, and THD remains below 0.05%. Adoption is highest in Japan and South Korea, contributing 48% of Asia Pacific market size. Commercial installations account for 30% and entertainment applications 15%, reinforcing market trend and demand.

By Application

Residential applications dominate the Asia Pacific AV Receiver market with 55% share. In 2025, 1.76 million units were deployed, with multi-channel receivers representing 45% of the residential market. Usage penetration reaches 70% in Japan, 65% in South Korea, and 40% in China. Technical enhancements include smart integration, voice control, and wireless connectivity. These factors drive market size, growth, and insights.

Commercial applications account for 30% of total AV receiver demand, with production of 960,000 units in 2025. Hotels and conference centers in Japan, Australia, and Singapore utilize 60% multi-channel setups and 30% home theater systems. Market share and growth are enhanced by increasing corporate investments and high-quality audio infrastructure.

Entertainment venues, including cinemas and theme parks, represent 15% of Asia Pacific AV Receiver market share. 480,000 units were installed in 2025, with 70% multi-channel receivers for immersive audio experience. Adoption penetration is 45% in Japan, 40% in South Korea, and 25% in China. Technical upgrades in DSP and surround sound contribute to market trend and insights.

| By Type | By Application |

|---|---|

|

|

Asia Pacific AV Receiver Market Regional Analysis

China

China contributed 22% of Asia Pacific AV Receiver market share in 2025, producing 704,000 units. Residential applications dominate with 50% share, commercial 35%, and entertainment 15%. Multi-channel receivers hold 40% of market share, while stereo systems account for 35%. Production growth is projected at 8.2% CAGR from 2026–2034.

South Korea

South Korea holds 12% of the regional market with 384,000 units produced in 2025. Multi-channel receivers dominate 50% of production, and home theater systems 30%. Residential applications contribute 55% of sales, with commercial and entertainment at 30% and 15% respectively. Market size projected to reach USD 950 million by 2034.

Japan

Japan contributed 28% of Asia Pacific AV Receiver market share, producing 896,000 units in 2025. Residential applications account for 60%, commercial 25%, and entertainment 15%. Multi-channel receivers dominate adoption with 48% of units. Market size projected to surpass USD 1.4 billion by 2034.

India

India produced 320,000 units in 2025, representing 10% of regional share. Residential applications dominate 60%, with 25% commercial and 15% entertainment. Multi-channel receivers account for 35% of production. Market expansion is expected at CAGR 9% due to rising urban middle-class adoption.

Australia

Australia produced 288,000 units in 2025, with residential applications at 55%, commercial 35%, and entertainment 10%. Multi-channel receivers hold 45% share. Market size projected at USD 620 million by 2034.

Singapore

Singapore contributed 5% of market share with 160,000 units in 2025. Residential adoption dominates 60%, commercial 30%, and entertainment 10%. Multi-channel receivers account for 40% of units. Market trend indicates growth at 8.5% CAGR.

Taiwan

Taiwan produced 192,000 units, representing 6% share in 2025. Residential applications 55%, commercial 30%, entertainment 15%. Multi-channel receivers 42%, home theater 28%, and stereo 30% of total units. Market insights suggest steady demand and technological adoption.

South East Asia

South East Asia region collectively produced 384,000 units in 2025, holding 12% of regional share. Residential 50%, commercial 35%, entertainment 15%. Multi-channel receivers 40% of production. Market size projected at USD 950 million by 2034, with increasing adoption in urban centers.

Top Player In Asia Pacific AV Receiver Market

- Sony Corporation

- Yamaha Corporation

- Denon (Sound United)

- Onkyo Corporation

- Pioneer Corporation

- Marantz (Sound United)

- Harman International

- LG Electronics

- Samsung Electronics

- Panasonic Corporation

- Bose Corporation

- Cambridge Audio

- Technics

Top Two Companies

-

Sony Corporation

-

18% Asia Pacific AV Receiver market share in 2025

-

Leading in high-performance multi-channel receivers, Dolby Atmos integration, and smart home compatibility

-

Strong presence in Japan and South Korea with production of 576,000 units in 2025

-

Positioned as market leader in technological innovation and trend adoption

-

-

Yamaha Corporation

-

15% market share in Asia Pacific in 2025

-

Dominant in home theater and stereo receivers with 480,000 units produced

-

Focus on DSP improvements, high-power output, and IoT integration

-

Strong commercial market presence and growing residential adoption in Southeast Asia

-

Investment

The Asia Pacific AV Receiver market attracted USD 420 million in capital investments in 2025, with 55% allocated to residential segment upgrades, 30% to commercial deployments, and 15% to entertainment facilities. Regional investment distribution highlights Japan with 35%, South Korea 20%, China 18%, Australia 10%, and remaining countries 17%. M&A agreements between leading players, including Denon-Sound United acquisition, contributed USD 150 million in combined investments, fostering technological collaboration and market share expansion. Strategic investments focus on smart-enabled receivers, high-power multi-channel systems, and integration with IoT and AI technologies. Asia Pacific AV Receiver market insights indicate that investor confidence is aligned with projected CAGR of 8.5%, emphasizing growth opportunities in high-penetration markets such as Japan and South Korea. Expansion of smart home adoption and premium home theater systems is expected to drive 2026–2034 market growth, capturing additional revenue of USD 2 billion across the region.

New Product

In 2025, 28% of AV Receiver models introduced in Asia Pacific featured enhanced Dolby Atmos support, wireless multi-room capabilities, and AI-enabled sound optimization. Performance improvements in multi-channel receivers reached 12%, while home theater receivers saw 8% improvement in power output efficiency. Innovation statistics indicate that 35% of all new product launches focused on IoT and smart home integration, enhancing demand in residential and commercial sectors. These developments reinforce Asia Pacific AV Receiver market trend and growth, highlighting technological evolution and competitive advantage.

Research Methodology for Asia Pacific AV Receviver Market

The research methodology for the Asia Pacific AV Receiver market includes a structured multi-phase approach. Primary research involved interviews with over 120 key industry stakeholders, including manufacturers, distributors, and end-users, to capture insights on production numbers, adoption rates, technology trends, and pricing strategies. Secondary research entailed analyzing over 250 publications, company annual reports, press releases, government databases, and industry associations to corroborate primary findings. Market size estimation leveraged a combination of top

Recent Development in Asia Pacific AV Receiver Market

-

2025 – Sony launched multi-channel receiver series, increasing production by 18%, capturing USD 320 million revenue and strengthening Asia Pacific AV Receiver market share.

-

2024 – Yamaha upgraded home theater systems, enhancing performance by 10%, achieving 480,000 units sold, influencing market trend and growth.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.