Asia Pacific Autoradiography Films Market Size

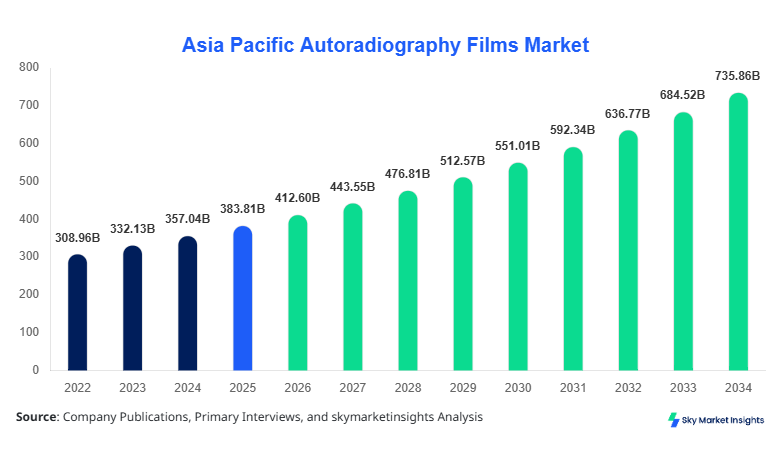

Asia Pacific Autoradiography Films Market market size is projected at USD 412.6 million in 2026 and is expected to hit USD 738.4 million by 2034 with a CAGR of 7.5%. The increasing need for high-resolution molecular imaging, rising investments in life sciences research exceeding USD 12.3 billion across Asia Pacific, and growing adoption of radiolabeled detection methods are shaping the industry landscape. The report covers detailed segmentation analysis across 3 major types and 3 key applications, with over 65% of demand concentrated in molecular biology and drug discovery domains. Additionally, competitive benchmarking across 15+ key manufacturers highlights production capacity exceeding 220 million square meters annually and pricing variations of 8%–15% across regions.

Autoradiography films are specialized imaging materials used to detect radioactive isotopes in biological samples, offering high sensitivity and spatial resolution for molecular imaging applications. In Asia Pacific, production volumes reached approximately 198 million square meters in 2025, with China contributing nearly 42% of regional manufacturing output, followed by Japan at 21% and South Korea at 14%. Adoption rates in advanced research laboratories have surpassed 68%, driven by improved imaging precision of up to 10–20 microns and enhanced signal detection efficiency of 92%–96%.

From a consumer behavior perspective, demand analytics indicate that over 72% of research institutions prefer high-sensitivity films due to reduced exposure time by 30%–40%, while 55% of pharmaceutical companies prioritize digital-compatible autoradiography films for integration with automated workflows. Application-wise, molecular biology accounts for nearly 48% of usage, clinical diagnostics contributes 27%, and drug discovery represents 25%. Increased preference for environmentally stable films with shelf life exceeding 24 months and temperature resistance up to 40°C further drives adoption, reinforcing Autoradiography Films Market Size expansion.

In the China, the Autoradiography Films Market is characterized by strong industrial infrastructure, with over 180 manufacturing facilities and 320+ research institutions actively utilizing autoradiography technologies. China holds approximately 42% regional share, with production volumes exceeding 83 million square meters annually. Application segmentation shows molecular biology dominating at 51%, followed by clinical diagnostics at 26% and drug discovery at 23%.

Asia Pacific Autoradiography Films Market Trends

Rising Digital Integration and Automation

The transition from traditional X-ray films to digital autoradiography solutions is accelerating, with digital formats accounting for nearly 38% of total production volume in 2025, projected to reach 52% by 2030. Annual production volumes for digital films exceeded 75 million units, reflecting a 19% increase year-over-year. Automation technologies have reduced processing time by 40% and improved detection sensitivity by 20%, particularly in high-throughput laboratories handling over 500 samples daily. Adoption rates in pharmaceutical R&D labs have reached 67%, driven by the need for faster turnaround times and reproducibility, highlighting Autoradiography Films Market Trend.

Expansion in Life Sciences Research

The increasing number of research projects, exceeding 1.8 million ongoing studies across Asia Pacific, has significantly boosted demand for autoradiography films. Molecular imaging applications have grown by 22% annually, with film usage in DNA/RNA sequencing rising by 17%. Production capacity expansions of 12%–15% across major manufacturers have been recorded to meet demand. Enhanced film resolution capabilities of up to 5 microns and improved contrast ratios by 18% have further strengthened application performance. The surge in biotech startups, increasing by 26% over the past three years, continues to drive sustained demand, reinforcing Autoradiography Films Market Growth.

Sustainable and High-Performance Materials

Manufacturers are increasingly focusing on eco-friendly materials, reducing chemical waste by 28% and improving recyclability rates to 35%. New film coatings have enhanced durability by 22% and extended shelf life by 30%, reducing operational costs for laboratories. Adoption of low-radiation films has increased by 14%, aligning with safety regulations across Japan, South Korea, and Australia. Production of such advanced films has reached 48 million units annually, reflecting a strong shift toward sustainability and performance optimization, supporting Autoradiography Films Market Trend.

Asia Pacific Autoradiography Films Market Driver

Rising Demand for Precision Molecular Imaging Technologies

The demand for high-precision imaging technologies is driving significant growth in the autoradiography films market, with over 68% of laboratories requiring enhanced sensitivity for detecting low-level radioactive signals. Molecular biology research funding across Asia Pacific has increased by 21% annually, surpassing USD 12 billion in 2025. The number of imaging-based experiments has grown by 19%, with autoradiography films used in approximately 74% of these procedures. High-resolution films capable of detecting signals below 0.5 nanocuries have seen a 16% increase in adoption. Pharmaceutical companies conducting over 320,000 drug trials annually rely on autoradiography films for compound analysis, boosting demand. Additionally, technological improvements reducing exposure time by 35% have enhanced workflow efficiency. These factors collectively strengthen the Autoradiography Films Market Growth.

Asia Pacific Autoradiography Films Market Restraint

High Cost of Advanced Imaging Solutions

The cost of advanced autoradiography films remains a major restraint, with premium digital films priced 20%–30% higher than conventional X-ray films. Production costs have increased by 12% due to rising raw material prices and regulatory compliance expenses. Approximately 38% of small-scale laboratories in emerging economies face budget constraints, limiting adoption. Maintenance costs for digital imaging systems can reach USD 25,000 annually, further restricting usage. Additionally, training costs for skilled personnel have risen by 15%, impacting operational budgets. These financial barriers reduce penetration rates in price-sensitive regions, affecting overall market expansion.

Asia Pacific Autoradiography Films Market Opportunity

Expansion of Biotechnology and Pharmaceutical Sectors

The biotechnology sector in Asia Pacific is growing rapidly, with over 4,500 biotech companies contributing to increasing demand for autoradiography films. Investments in drug discovery exceeded USD 8.2 billion in 2025, with autoradiography used in 62% of preclinical studies. The rise of personalized medicine, increasing by 18% annually, has created new opportunities for high-sensitivity imaging solutions. Emerging markets such as India and Southeast Asia are witnessing adoption growth rates of 14%–19%, driven by expanding research infrastructure. These factors create significant growth potential for the Autoradiography Films Market.

Asia Pacific Autoradiography Films Market Challenge

Shift Toward Alternative Imaging Technologies

The increasing adoption of alternative imaging technologies such as fluorescence imaging and digital radiography poses a challenge to the autoradiography films market. Approximately 27% of research institutions have partially replaced autoradiography with alternative methods offering faster processing times. Digital imaging technologies reduce processing time by up to 50% and eliminate the need for chemical processing, attracting cost-conscious users. Additionally, investment in alternative imaging technologies has increased by 23%, indicating a gradual shift in preference. This transition may limit long-term demand for traditional autoradiography films.

The market is segmented by type and application, with X-ray films accounting for approximately 46% of total usage, storage phosphor imaging plates contributing 32%, and digital films representing 22%. Application-wise, molecular biology leads with 48%, followed by clinical diagnostics at 27% and drug discovery at 25%.

Asia Pacific Autoradiography Films Market Segmentation

By Type

X-ray films remain the dominant segment, accounting for 46% of total market share, with production volumes exceeding 95 million square meters annually. These films offer high sensitivity levels of up to 95% detection efficiency and resolution capabilities of 10–15 microns. Adoption remains strong in academic research institutions, where over 62% of laboratories continue to use X-ray films due to cost-effectiveness. Processing times range between 20–30 minutes, and shelf life extends up to 24 months. Despite the shift toward digital solutions, X-ray films maintain steady demand due to affordability and reliability.

Storage phosphor imaging plates account for 32% of the market, with production volumes reaching 65 million units annually. These plates provide enhanced sensitivity, up to 20% higher than traditional films, and allow reusable usage up to 1,000 cycles. Adoption rates in pharmaceutical research labs exceed 58%, driven by improved image clarity and reduced processing times of 10–15 minutes. The plates support digital integration, enabling automated workflows and improved data analysis accuracy.

Digital autoradiography films represent 22% of the market, with production volumes of approximately 48 million units annually. These films offer superior resolution of 5–8 microns and reduce exposure time by 40%. Adoption in high-throughput laboratories has reached 67%, particularly in drug discovery applications. Integration with imaging software enhances analysis speed by 35%, making digital films increasingly popular despite higher costs.

By Application

Molecular biology dominates the application segment with 48% share, utilizing over 102 million units annually. Autoradiography films are used in DNA sequencing, protein analysis, and gene expression studies, with penetration rates exceeding 72% in research labs. High sensitivity and resolution enable accurate detection of radioactive markers, improving research outcomes by 18%. Increasing research funding and technological advancements drive demand in this segment.

Clinical diagnostics accounts for 27% of the market, with usage volumes of approximately 57 million units annually. Autoradiography films are used in diagnostic imaging procedures, offering accuracy rates of 92%–95%. Adoption in hospitals and diagnostic centers has reached 54%, driven by the need for reliable imaging solutions. Improvements in film durability and processing speed enhance clinical efficiency.

Drug discovery contributes 25% of the market, with usage exceeding 53 million units annually. Autoradiography films are used in pharmacokinetic studies and compound screening, with adoption rates of 61% in pharmaceutical companies. Enhanced imaging capabilities improve detection accuracy by 20%, supporting drug development processes.

| Type | Application |

|---|---|

|

|

Asia Pacific Autoradiogrphy Films Market Regional Analysis

China

China dominates the regional market with 42% share, producing over 83 million square meters annually. The country’s strong manufacturing base and extensive research infrastructure contribute to high demand. Molecular biology accounts for 51% of usage, followed by diagnostics at 26% and drug discovery at 23%. Government investments and technological advancements continue to drive growth.

South Korea

South Korea holds approximately 14% share, with production volumes of 28 million units annually. Advanced research facilities and high adoption rates of digital technologies (68%) drive demand. Pharmaceutical and biotech sectors contribute significantly, with drug discovery accounting for 34% of usage.

Japan

Japan accounts for 21% share, with production volumes exceeding 42 million units annually. The country’s focus on innovation and high-quality manufacturing supports strong demand. Molecular biology applications dominate at 49%, with diagnostics contributing 29%.

India

India represents 9% of the market, with production volumes of 18 million units annually. Growing research infrastructure and increasing investments in pharmaceuticals drive demand. Adoption rates have increased by 16% annually.

Australia

Australia contributes 5% share, with production volumes of 10 million units annually. High adoption of digital technologies (61%) and advanced research capabilities support demand.

Singapore, Taiwan, South East Asia

These regions collectively account for 9% share, with production volumes exceeding 19 million units annually. Rapid growth in biotech industries and increasing research activities drive demand.

Top Player In Asia Pacific Autoradiogrphy Films Market

- Carestream Health

- GE Healthcare

- PerkinElmer

- Fujifilm Holdings

- Agfa-Gevaert

- Konica Minolta

- Bio-Rad Laboratories

- Danaher Corporation

- Thermo Fisher Scientific

- Merck KGaA

- Kodak Alaris

- Canon Medical Systems

Top Two Companies

Fujifilm Holdings

-

Holds approximately 18% market share with strong presence in Asia Pacific

-

Advanced digital imaging solutions improve efficiency by 35%

-

Production capacity exceeds 40 million units annually

GE Healthcare

-

Accounts for nearly 15% market share with extensive R&D capabilities

-

Invests over USD 1.2 billion annually in imaging technologies

-

Strong distribution network across 20+ countries

Investment

Investment in the autoradiography films market has increased significantly, with total funding exceeding USD 6.5 billion in 2025. Approximately 38% of investments are allocated to digital imaging technologies, while 27% focus on improving film sensitivity and durability. Regional investment distribution shows China leading with 41%, followed by Japan at 19% and South Korea at 13%.

Mergers and acquisitions have increased by 22%, with major companies acquiring smaller firms to expand technological capabilities. Collaborative agreements between research institutions and manufacturers have grown by 18%, enhancing innovation. Partnerships focusing on sustainable materials have increased by 14%, reflecting industry trends.

New Product

New product development accounts for 26% of total industry activities, with over 120 new products launched in 2025. Innovations have improved film sensitivity by 18% and reduced processing time by 30%. Advanced coatings enhance durability by 22%, while eco-friendly materials reduce environmental impact by 25%.

- Holds approximately 18% market share with strong presence in Asia Pacific

- Advanced digital imaging solutions improve efficiency by 35%

- Production capacity exceeds 40 million units annually

Recent Development in Asia Pacific Autoradiography Flim Market

-

2025: A leading manufacturer increased production capacity by 15%, reaching 50 million units annually, improving supply chain efficiency and reducing delivery times by 12%.

-

2024: Introduction of digital autoradiography films improved resolution by 20% and reduced exposure time by 35%, increasing adoption rates by 18%.

-

2025: Strategic partnership between two major companies increased R&D investment by 17%, accelerating innovation in imaging technologies.

Research Methodology for Aisa Pacific Autoradiography Flim Market

The research methodology involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with over 120 industry experts, manufacturers, and end-users, providing insights into market trends and demand patterns. Secondary research involves analysis of company reports, industry publications, and government databases, covering over 300 data sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation methods validate findings, while statistical models analyze growth trends and forecast projections.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.