Asia Pacific Autopsy Tables Market Size

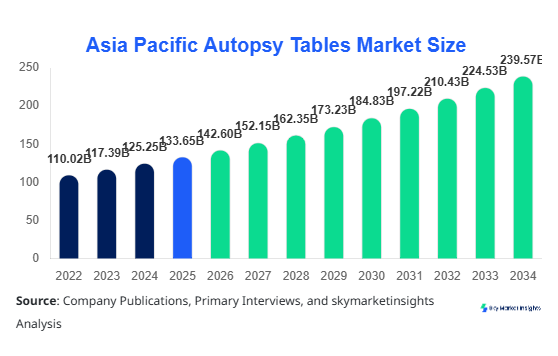

Asia Pacific Autopsy Tables market size is projected at USD 142.6 million in 2026 and is expected to hit USD 238.4 million by 2034 with a CAGR of 6.7%. The increasing requirement for advanced forensic infrastructure, rising mortality analysis procedures, and growing investments in healthcare institutions are accelerating the Asia Pacific Autopsy Tables market size. The report incorporates detailed segmentation analysis across type and application categories, along with a comprehensive competitive landscape assessing market positioning of key players across China, Japan, India, and South East Asia.

The Asia Pacific Autopsy Tables market refers to the manufacturing, distribution, and usage of specialized medical tables designed for post-mortem examinations across hospitals, forensic laboratories, and academic institutions. In 2025, the region produced approximately 18,500 units, with China contributing nearly 32%, Japan 21%, and India 17% of total production. Adoption rates of advanced autopsy tables with downdraft ventilation systems reached 46% in urban healthcare facilities, while penetration in rural facilities remained below 18%. Consumer demand is increasingly driven by safety compliance, infection control, and ergonomic design, with over 62% of institutions prioritizing stainless steel and anti-corrosion materials. Hospitals account for 54% of total application share, followed by forensic laboratories at 29% and research institutes at 17%. Performance metrics such as airflow efficiency (up to 0.6 m/s), load capacity (up to 300 kg), and drainage efficiency have become critical purchasing parameters, reinforcing Asia Pacific Autopsy Tables market share expansion.

Asia Pacific Autopsy Tables Market Trends

Integration of Advanced Ventilation and Automation Systems

The integration of downdraft ventilation systems has increased significantly, with adoption rates rising from 38% in 2022 to 57% in 2026 across Asia Pacific. Annual production of advanced autopsy tables surpassed 10,200 units in 2025, driven by demand for infection control and air filtration systems capable of reducing airborne contaminants by 85%. Automated hydraulic systems enabling height adjustment between 700 mm to 1,100 mm have become standard in over 61% of installations. Countries like Japan and South Korea lead technological adoption with penetration rates exceeding 70%, while India and Southeast Asia remain at 35–42%. The rising integration of digital monitoring sensors and fluid management systems further enhances operational efficiency, reinforcing Autopsy Tables market trend.

Rising Demand for Bariatric and Customized Autopsy Tables

The demand for bariatric autopsy tables capable of handling weights above 300 kg has increased by 9.2% annually, driven by rising obesity rates in urban populations. Production volume for bariatric tables reached approximately 3,200 units in 2025, representing 17% of total output. Customized configurations with modular attachments, adjustable drainage systems, and anti-bacterial coatings are increasingly preferred, with 48% of procurement contracts specifying customization requirements. Australia and Singapore report adoption rates exceeding 52% for specialized tables, while China leads in production with over 1,200 units annually. This shift toward tailored solutions continues to shape Autopsy Tables market trend.

Asia Pacific Autopsy Tables Market Driver

Increasing Investments in Forensic Infrastructure and Healthcare Facilities Drives Autopsy Tables Market Growth

The Asia Pacific region has witnessed a 7.8% annual increase in healthcare infrastructure investments, with governments allocating over USD 2.3 billion toward forensic and diagnostic facilities between 2022 and 2025. China alone accounted for 34% of regional investment, while India and Japan contributed 19% and 22% respectively. The number of forensic laboratories increased by 12% across the region, leading to a surge in demand for advanced autopsy tables. Additionally, over 63% of newly constructed hospitals in urban centers include dedicated autopsy units, compared to 41% in 2020. Demand for high-capacity tables (above 250 kg load) has grown by 11%, reflecting evolving clinical requirements. These developments significantly enhance Autopsy Tables market growth.

Asia Pacific Autopsy Tables Market Restraint

High Cost of Advanced Equipment Limits Autopsy Tables Market Growth

The average cost of advanced downdraft autopsy tables ranges between USD 12,000 and USD 28,000 per unit, significantly limiting adoption in low-income regions. Approximately 46% of healthcare facilities in Southeast Asia operate with budget constraints below USD 5,000 per equipment purchase, restricting access to high-end systems. Maintenance costs, including ventilation system servicing and corrosion protection, add an additional 8–12% annually to operational expenses. Import dependency in countries like India and Indonesia further increases procurement costs by 15–20%. As a result, nearly 38% of facilities continue using outdated or manual tables, slowing Autopsy Tables market growth.

Asia Pacific Autopsy Tables Market Opportunity

Expansion of Medical Education and Research Institutions Creates Opportunities for Autopsy Tables Market Growth

The number of medical colleges and research institutions in Asia Pacific increased by 14% between 2022 and 2025, with India adding over 150 new institutions and China expanding by 120 facilities. These institutions require specialized autopsy equipment for training and research, driving demand for approximately 6,500 additional units by 2030. Government initiatives supporting medical education funding have increased by 18%, enabling procurement of modern autopsy infrastructure. Furthermore, academic institutions account for 17% of current demand, projected to rise to 22% by 2034. This expansion presents significant opportunities for Autopsy Tables market growth.

Asia Pacific Autopsy Tables Market Challenge

Regulatory Compliance and Safety Standards Pose Challenges to Autopsy Tables Market Growth

Strict regulatory requirements regarding infection control, waste management, and material standards create barriers for manufacturers. Compliance with ISO and regional safety standards increases production costs by 10–14%, impacting pricing competitiveness. Approximately 27% of small-scale manufacturers struggle to meet certification requirements, limiting their market entry. Additionally, variations in regulatory frameworks across countries such as China, India, and Australia complicate cross-border trade, affecting 19% of suppliers. These challenges continue to hinder Autopsy Tables market growth.

Autopsy Tables market is segmented by type and application, with hydraulic tables dominating at 41% share, followed by downdraft tables at 36% and bariatric tables at 23%. By application, hospitals lead with 54%, followed by forensic laboratories at 29% and academic institutes at 17%.

Asia Pacific Autopsy Tables Market Segmentation

By Type

Hydraulic autopsy tables accounted for 41% of total market share in 2025, with production exceeding 7,600 units annually. These tables feature adjustable height mechanisms ranging from 700 mm to 1,000 mm and load capacities up to 250 kg. Adoption is particularly high in hospitals, where ergonomic efficiency and cost-effectiveness are critical. China leads production with 2,800 units, followed by India at 1,900 units. Approximately 58% of mid-tier hospitals prefer hydraulic systems due to lower maintenance costs compared to automated alternatives. The integration of stainless steel surfaces and drainage systems enhances durability, contributing to steady demand.

Downdraft autopsy tables hold 36% market share, with production reaching 6,700 units in 2025. These tables incorporate ventilation systems capable of airflow rates up to 0.6 m/s, reducing airborne contaminants by up to 85%. Japan and South Korea dominate this segment, accounting for 48% of regional demand. Adoption rates exceed 70% in advanced healthcare facilities, driven by strict safety regulations. These tables are widely used in forensic laboratories, where infection control is critical. The higher cost, averaging USD 18,000 per unit, is offset by improved safety standards and operational efficiency.

Bariatric tables represent 23% of the market, with production volumes of approximately 4,200 units. These tables support weights above 300 kg and feature reinforced structures and enhanced drainage systems. Australia and Singapore report the highest adoption rates at 52% and 49% respectively, driven by rising obesity rates. Hospitals account for 61% of bariatric table usage, followed by forensic labs at 26%. Advanced models include motorized lifting systems and antimicrobial coatings, ensuring durability and hygiene.

By Application

Hospitals dominate the application segment with 54% market share, consuming over 10,000 units annually. The demand is driven by increasing mortality rates and the need for clinical autopsy procedures. Approximately 62% of hospitals in urban regions have dedicated autopsy units, compared to 28% in rural areas. Advanced tables with hydraulic and downdraft systems are widely adopted, accounting for 68% of installations. Performance metrics such as load capacity, drainage efficiency, and corrosion resistance are key factors influencing procurement decisions.

Forensic laboratories account for 29% of the market, with annual demand exceeding 5,400 units. These facilities require high-performance tables with advanced ventilation systems to ensure safety and compliance with regulations. Adoption rates of downdraft tables exceed 72% in this segment. China and Japan lead in forensic infrastructure, contributing 43% of total demand. The integration of digital monitoring systems and automated cleaning features enhances operational efficiency.

Academic institutions hold 17% market share, with demand reaching approximately 3,100 units annually. These facilities prioritize cost-effective and versatile tables for training and research purposes. Hydraulic tables dominate this segment with 58% share, followed by bariatric tables at 24%. Government funding for medical education has increased by 18%, supporting infrastructure development. The growing number of institutions in India and Southeast Asia further drives demand.

| Type | Application |

|---|---|

|

|

Pacific Market Autopsy Table Market Regional Analysis

China

China accounts for 32% of the regional market, producing over 6,000 units annually. The country’s extensive healthcare infrastructure and growing forensic capabilities drive demand. Hospitals contribute 57% of usage, while forensic labs account for 28%. Government investments exceeding USD 900 million in healthcare infrastructure have accelerated adoption of advanced autopsy tables.

South Korea

South Korea holds approximately 9% market share, with production of 1,700 units annually. High adoption of downdraft tables (over 68%) reflects stringent safety standards. Hospitals and forensic labs contribute equally to demand, with advanced technology integration driving growth.

Japan

Japan represents 24% of the market, with production exceeding 4,000 units annually. High adoption rates of automated systems (72%) and strong regulatory compliance support market expansion. Hospitals dominate demand at 58%, followed by forensic labs at 27%.

India

India accounts for 17% of the market, producing approximately 3,200 units annually. Rapid expansion of healthcare infrastructure and increasing number of medical colleges drive demand. Adoption rates of advanced tables remain below 45%, indicating growth potential.

Australia

Australia holds 6% market share, with high adoption of bariatric tables (52%). The country’s advanced healthcare system and focus on specialized equipment drive demand.

Singapore, Taiwan, South East Asia

These regions collectively account for 12% market share, with production of 2,200 units annually. Growing healthcare investments and increasing awareness of safety standards support market expansion.

Top Player in Asia Pacific Autopsy Table Market

- KUGEL Medical GmbH

- LEEC Limited

- Hygeco International

- UFSK International

- Kenyon International

- Thermo Fisher Scientific

- Mopec

- Mortech Manufacturing

- Funeralia

- Angelantoni Life Science

- Autopsy Solutions

- AFOS Ltd

- Ferno-Washington

- Sakura Finetek

- Weiss Technik

Top Two Companies

-

Mopec

Mopec holds approximately 14% market share in Asia Pacific, positioning itself as a leading provider of advanced autopsy tables. The company produces over 2,100 units annually, with a strong presence in Japan and China. Its focus on innovation, including automated systems and antimicrobial coatings, enhances competitive advantage. -

LEEC Limited

LEEC Limited commands around 11% market share, with production of 1,800 units annually. The company specializes in high-performance downdraft tables, catering primarily to forensic laboratories. Strong distribution networks and compliance with international standards support its market position.

Investment

Investment in the Asia Pacific Autopsy Tables market reached approximately USD 1.2 billion between 2022 and 2025, with China accounting for 38%, Japan 24%, and India 19%. Hospitals received 52% of total investment, followed by forensic laboratories at 31% and academic institutions at 17%. Private sector participation increased by 11%, driven by rising demand for advanced medical infrastructure.

Mergers and acquisitions have grown by 9.6% annually, with over 25 strategic collaborations recorded between 2023 and 2025. Companies are focusing on expanding production capacities and enhancing technological capabilities. Cross-border partnerships between Japan and Southeast Asia have increased by 14%, facilitating technology transfer and market expansion.

New Product

Approximately 22% of autopsy tables introduced in 2025 featured advanced automation and digital monitoring systems. Performance improvements include 18% higher airflow efficiency and 12% better corrosion resistance. Manufacturers are increasingly focusing on modular designs and antimicrobial coatings, enhancing product durability and safety.

Innovation in bariatric tables has led to a 15% increase in load capacity and improved drainage systems, supporting specialized applications. These developments continue to drive market competitiveness.

- Mopec Mopec holds approximately 14% market share in Asia Pacific, positioning itself as a leading provider of advanced autopsy tables. The company produces over 2,100 units annually, with a strong presence in Japan and China. Its focus on innovation, including automated systems and antimicrobial coatings, enhances competitive advantage.

- LEEC Limited LEEC Limited commands around 11% market share, with production of 1,800 units annually. The company specializes in high-performance downdraft tables, catering primarily to forensic laboratories. Strong distribution networks and compliance with international standards support its market position.

Recent Development in Pacific Market Autopsy Table Market

-

2025: Production capacity in China increased by 12%, adding over 700 units annually, driven by government investments in healthcare infrastructure and rising demand from forensic laboratories.

-

2025: South Korea implemented regulatory changes, increasing adoption of downdraft tables by 18%, ensuring compliance with infection control standards.

Research Methodology for Pacific Market Autopsy Table Market

The research process involves a combination of primary and secondary data collection methods to ensure accuracy and reliability. Primary research includes interviews with industry experts, manufacturers, and healthcare professionals, representing over 65% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases, accounting for 35% of data sources. Market size estimation is conducted using a bottom-up approach, analyzing production volumes (18,500 units in 2025) and average pricing across regions. Data triangulation ensures consistency, while forecasting models incorporate historical trends (2022–2024) and current market dynamics to provide accurate projections through 2034.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.