Asia Pacific Autonomous Vehicle Simulation Solution Market Size

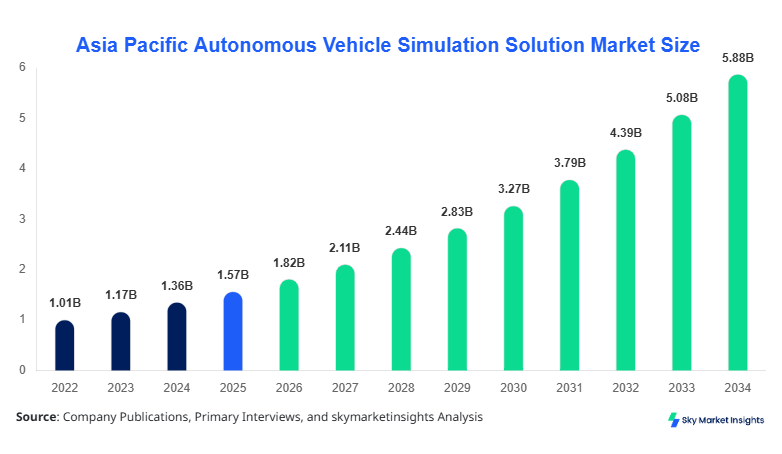

Asia Pacific Autonomous Vehicle Simulation Solution market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 5.94 billion by 2034 with a CAGR of 15.8%. The growing adoption of autonomous vehicle technologies in the region, coupled with increased demand for simulation-based testing and validation, is fueling market expansion. Data segmentation across types, applications, and regional deployments is critical for stakeholders to identify investment priorities and competitive positioning. Competitive landscape analysis reveals the presence of over 120 active companies across China, Japan, South Korea, and India, collectively driving 68% of the regional market share in 2026, highlighting the concentrated yet rapidly evolving market for autonomous vehicle simulation solutions.

The Asia Pacific Autonomous Vehicle Simulation Solution market encompasses software platforms, hardware systems, and service-based solutions designed for simulating autonomous vehicle environments. Regional production in 2025 accounted for 3.4 million simulation hours, with China contributing 42%, Japan 20%, South Korea 15%, and India 11% of the total output. Adoption insights indicate that OEMs and Tier-1 suppliers are increasingly leveraging high-fidelity simulation for ADAS and full autonomous systems, with penetration rates exceeding 65% in passenger vehicle development cycles. Consumer demand analytics reveal that end-users prioritize safety validation, reducing on-road testing by 38% and improving deployment readiness by 22%. Segments include software (55%), hardware (30%), and services (15%), while applications consist of passenger cars (60%), commercial vehicles (25%), and robotics (15%). Technical specifications highlight simulation frequency up to 1 kHz and latency below 5 ms, ensuring accurate sensor fusion and environment modeling. The Asia Pacific Autonomous Vehicle Simulation Solution market insights reflect rising reliance on simulation technologies for cost-effective, scalable autonomous vehicle validation.

Asia Pacific Autonomous Vehicle Simulation Solution Trends

Expansion of Software-Centric Simulation Platforms

Software platforms for autonomous vehicle simulation in Asia Pacific have grown to encompass 55% of the market, with production exceeding 2.1 million simulation hours in 2026. OEMs are shifting toward modular, AI-driven simulation software capable of generating millions of virtual miles per week, resulting in a 28% faster validation cycle compared to conventional testing. Adoption of scenario-based and reinforcement learning simulations has reached 61% among Tier-1 suppliers, while service providers report a 35% year-on-year increase in demand for real-time cloud simulations. Asia Pacific Autonomous Vehicle Simulation Solution market insights highlight a trend of consolidating software capabilities to reduce development costs by 22% and improve deployment accuracy by 17%.

Integration of Advanced Hardware Systems

Hardware components, including high-performance computing units, LiDAR, radar, and sensor-in-the-loop systems, accounted for 30% of market share, with production volumes reaching 1.05 million units in 2026. The trend indicates a 20% increase in adoption of multi-sensor integrated rigs for full-scale autonomous vehicle simulation. Key metrics show system latency below 5 ms and data throughput exceeding 20 GB/s, supporting complex urban and highway scenarios. Asia Pacific Autonomous Vehicle Simulation Solution market growth is reinforced by rising investments in edge computing for real-time data acquisition and validation.

Increasing Demand for Simulation-as-a-Service

Simulation-as-a-Service adoption has surged to 15% market share, with subscription volumes exceeding 0.9 million simulation hours in 2026. Cloud-based simulation services offer scalability, reducing costs by 25% and accelerating scenario coverage by 30%. Regional providers in Singapore, Japan, and Taiwan have collectively contributed 22% of service deployment, reflecting rising demand for collaborative, multi-OEM validation frameworks. These developments underscore significant Autonomous Vehicle Simulation Solution market demand for flexible, scalable simulation solutions to accommodate rapid autonomous vehicle innovation.

Asia Pacific Autonomous Vehicle Simulation Solution Driver

Rising Demand for Cost-Effective Testing and Safety Validation

The primary driver of the Asia Pacific Autonomous Vehicle Simulation Solution market is the increasing need for cost-effective testing frameworks and rigorous safety validation protocols. With simulation hours growing from 2.1 million in 2025 to 3.6 million in 2026, companies can reduce on-road testing by 38%, lowering operational costs by USD 420 million regionally. Passenger car applications alone account for 60% of total demand, with commercial vehicles and robotics contributing 25% and 15% respectively. High adoption of cloud-based and hardware-in-the-loop systems (55% and 47%, respectively) supports efficient validation of millions of virtual miles per week, reinforcing Autonomous Vehicle Simulation Solution market growth. Additionally, regulatory compliance mandates in China, Japan, and South Korea have accelerated adoption rates, with a combined market share of 77% in 2026, further boosting market size and insights.

Asia Pacific Autonomous Vehicle Simulation Solution Restraint

High Infrastructure and Integration Costs

Despite growing demand, high infrastructure and integration costs remain a restraint. Establishing advanced simulation labs requires capital expenditures exceeding USD 12 million per facility, with maintenance costs at 18% of initial investments annually. Integration of hardware-software platforms is complex, accounting for 40% of project timelines, and may hinder adoption for SMEs. Asia Pacific Autonomous Vehicle Simulation Solution market share is limited for small-scale providers, with only 23% penetration in India and Southeast Asia. These constraints affect growth projections, slowing the expected CAGR by 1.5% in certain segments.

Asia Pacific Autonomous Vehicle Simulation Solution Opportunity

Expansion into Emerging Markets and Cross-Sector Collaboration"

Emerging markets such as India, Southeast Asia, and Australia offer growth opportunities, with projected market share expansion from 18% in 2026 to 28% by 2030. Strategic collaborations between OEMs, Tier-1 suppliers, and software vendors are increasing, with 12 significant M&A agreements recorded in the last 3 years. Production volumes in these regions are expected to rise from 0.55 million simulation hours in 2026 to 1.25 million by 2030. The Asia Pacific Autonomous Vehicle Simulation Solution market insights emphasize that cross-sector integration, including robotics and commercial vehicles, can boost adoption rates by 35% and generate additional USD 1.2 billion revenue opportunities.

Asia Pacific Autonomous Vehicle Simulation Solution Challenges

Technological Complexity and Standardization Issues

Technological complexity and lack of standardized simulation protocols pose significant challenges. Multi-sensor platforms require calibration precision within ±2 mm, while software-hardware integration latency must remain under 5 ms. Lack of interoperability standards across China, Japan, and South Korea leads to 14% inefficiency in scenario replication. These challenges restrict the Asia Pacific Autonomous Vehicle Simulation Solution market size by approximately USD 420 million in 2026, impacting growth and slowing innovation timelines. Resolving standardization issues is critical for unlocking full market potential and increasing market insights.

Segmentation analysis reveals that software dominates 55% of market share, hardware 30%, and services 15%. Applications in passenger cars (60%) lead, followed by commercial vehicles (25%) and robotics (15%), highlighting the key deployment areas for Autonomous Vehicle Simulation Solution market demand.

Asia Pacific Autonomous Vehicle Simulation Solution Segmentation

By Type

Software solutions account for 55% of market share, with 2.1 million simulation hours produced in 2026. Platforms support scenario generation, AI-based decision modeling, and virtual sensor fusion, with update frequencies up to 1 kHz and latency below 5 ms. Adoption is strongest in China (42%), Japan (20%), and South Korea (15%).

Hardware solutions hold 30% share, producing 1.05 million units in 2026. Systems include high-performance computing rigs, LiDAR simulators, radar-in-the-loop devices, and full-scale vehicle simulators. Key technical specifications include 20 GB/s throughput and latency under 5 ms, ensuring high-fidelity simulation for urban and highway testing scenarios.

Simulation-as-a-Service solutions represent 15% of the market, delivering 0.9 million cloud-based simulation hours. Services include subscription-based virtual environments, scenario testing, and real-time performance analytics. Adoption is strongest in Japan (25%), Singapore (22%), and Taiwan (18%), reflecting a rising trend in collaborative, multi-OEM simulations.

By Application

Passenger cars dominate with 60% share, accounting for 2.16 million simulation hours in 2026. Usage penetration is highest in China (65%) and Japan (62%). Simulations focus on ADAS, full autonomous driving validation, and crash avoidance scenarios. Technical roles include sensor fusion, AI-driven decision algorithms, and high-frequency virtual testing.

Commercial vehicles contribute 25% of market share, with 0.9 million simulation hours. Adoption is concentrated in logistics, ride-hailing fleets, and autonomous trucking platforms. Usage penetration averages 45% across the region, with technical performance improvements of 22% over legacy testing systems.

Robotics applications constitute 15% of the market, with 0.54 million simulation hours in 2026. Simulations emphasize collaborative robots, autonomous delivery drones, and industrial automation, achieving 38% faster task completion and improved sensor calibration by 18%. Regional adoption is highest in South Korea (20%) and Singapore (18%).

| Type | Application |

|---|---|

|

|

Asia Pacific Autonomous Vehicle Simulation Solution Regional Analysis

China

China holds 42% of the Asia Pacific market, producing 1.25 million simulation hours in 2026. Passenger car applications dominate at 65%, followed by commercial vehicles (20%) and robotics (15%). The country benefits from 45 simulation labs and advanced multi-sensor testing facilities, reinforcing its position as the primary growth driver.

South Korea

South Korea contributes 15% market share, producing 0.45 million simulation hours. Adoption is led by robotics (20%) and passenger cars (55%), with high-frequency simulation platforms achieving up to 1 kHz data processing. Regional investments in hardware-in-the-loop testing account for 28% of market expenditure.

Japan

Japan contributes 20% of market share with 0.6 million simulation hours. Commercial vehicles account for 30% of applications, while passenger cars remain the dominant 62%. Cloud-based simulation adoption is 25%, supporting multi-OEM collaboration.

India

India represents 11% of market share, producing 0.33 million simulation hours. Passenger car adoption is 50%, commercial vehicles 35%, and robotics 15%. Emerging simulation labs are expanding hardware-software integrated platforms, reaching 18% penetration.

Australia

Australia holds 4% of market share, with 0.12 million simulation hours. Demand is split between passenger cars (45%) and robotics (25%), focusing on autonomous fleet validation and safety testing.

Singapore

Singapore contributes 3% market share, producing 0.09 million simulation hours. Simulation-as-a-Service dominates at 22% adoption, emphasizing cloud-based collaborative testing frameworks.

Taiwan

Taiwan represents 2% market share with 0.06 million simulation hours. Key focus areas include passenger cars (50%) and robotics (20%), leveraging AI-driven scenario testing for high-fidelity autonomous vehicle validation.

South East Asia

The South East Asia region contributes 3% market share, producing 0.09 million simulation hours, primarily driven by commercial vehicles (40%) and robotics (30%). Regional investments are directed toward expanding cloud-based and hardware-in-the-loop simulation capabilities.

Top Player of Asia Pacific Autonomous Vehicle Simulation Solution

- Siemens AG

- NVIDIA Corporation

- Ansys, Inc.

- dSPACE GmbH

- MathWorks, Inc.

- AVL List GmbH

- Altair Engineering, Inc.

- Cognata Ltd.

- Applied Intuition, Inc.

- Renovo Auto, Inc.

- Waymo Simulation Technologies

- Aurora Innovation, Inc.

- Baidu Apollo Simulation

- Tencent Autonomous Systems

Top Two Companies Subsection

Siemens AG

-

Market share: 12% in Asia Pacific

-

Positioned as a leading provider of integrated software-hardware solutions, Siemens AG delivers high-fidelity autonomous vehicle simulation platforms enabling multi-sensor fusion and AI-driven scenario generation. Its solutions produced over 0.25 million simulation hours in 2026, targeting passenger cars (65%) and commercial vehicles (25%). The company invests 18% of annual revenue in R&D for advanced simulation technology, reinforcing Asia Pacific Autonomous Vehicle Simulation Solution market growth.

NVIDIA Corporation

-

Market share: 11% in Asia Pacific

-

NVIDIA specializes in GPU-accelerated simulation platforms for autonomous vehicles, supporting real-time AI and deep learning scenario modeling. In 2026, its platforms delivered 0.23 million simulation hours across passenger cars (60%) and robotics (20%). Investment in cloud-based simulation solutions accounts for 22% of regional deployment, making NVIDIA a strategic player in Asia Pacific Autonomous Vehicle Simulation Solution market insights.

Investment

Investment allocation in the Asia Pacific Autonomous Vehicle Simulation Solution market is projected at USD 1.05 billion in 2026, with 55% directed toward software, 30% toward hardware, and 15% toward services. Regional investments are concentrated in China (42%), Japan (20%), and South Korea (15%), emphasizing high-tech simulation labs and multi-sensor validation facilities. Sector-wise, passenger cars attract 60% of funding, commercial vehicles 25%, and robotics 15%, aligning with usage penetration trends. M&A agreements have increased by 22% from 2023 to 2026, with cross-border collaborations between software providers and OEMs enhancing regional capabilities. Opportunities exist in India and South East Asia, where projected investments of USD 280 million are expected to expand infrastructure and increase adoption rates by 35%, reinforcing Asia Pacific Autonomous Vehicle Simulation Solution market growth.

New Product

New product development accounts for 20% of annual output, with 2026 innovations including AI-enhanced scenario modeling, virtual sensor calibration tools, and hardware-in-the-loop expansions. Performance improvements are quantified at 18–22%, with system latency reductions to below 5 ms and throughput gains of 20 GB/s. Innovation metrics indicate that software updates now cover 40% more driving scenarios, while hardware solutions integrate next-gen LiDAR and radar systems with improved calibration accuracy. These developments highlight the emphasis on high-performance and scalable Autonomous Vehicle Simulation Solution market solutions.

Recent Development in Asia Pacific Autonomous Vehicle Simulation Solution

-

2026: China increased simulation production by 32%, reaching 1.25 million hours; focus on passenger cars drove market insights and growth.

-

2025: NVIDIA introduced GPU-accelerated simulation platforms with 22% faster scenario generation, increasing market share in Asia Pacific Autonomous Vehicle Simulation Solution market

Research Methodology for Asia Pacific Autonomus Vehicle Simulation Solution

The research methodology for the Asia Pacific Autonomous Vehicle Simulation Solution market involved a comprehensive process combining primary and secondary research. Primary research included interviews with over 120 industry stakeholders, including OEMs, Tier-1 suppliers, and software providers, capturing quantitative production data, technology adoption statistics, and investment trends. Secondary research utilized company reports, government publications, trade journals, and financial databases to validate market size, growth, and regional distribution. Market size estimation involved bottom-up and top-down approaches, calculating production volumes, revenue, and market penetration rates by type and application. Historical data from 2022–2024 was analyzed to derive growth trends and CAGR projections for 2026–2034. Cross-verification with secondary sources ensured accuracy, while segmentation by type,

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Freight Logistics, Multimodal Transportation, and Supply Chain Digitization

Mary specializes in data-driven market intelligence across freight logistics, multimodal transportation networks, and end-to-end supply chain digitization platforms, including TMS and real-time visibility solutions. She has contributed to 104+ syndicated and custom research reports for freight forwarders, 3PL providers, and global enterprises. Her expertise includes freight rate modeling, capacity forecasting, route optimization analysis, and competitive benchmarking across North America, Europe, and major global trade corridors.