Asia Pacific 4K Ultra HD Television Market Size

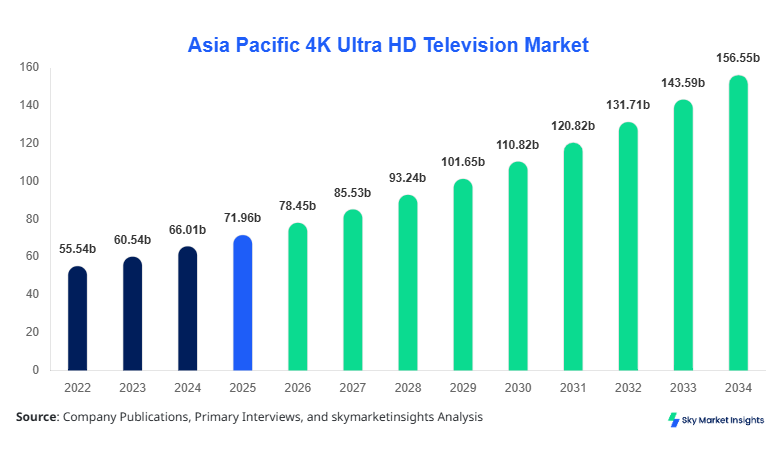

Asia Pacific 4K Ultra HD Television market size is projected at USD 78.45 billion in 2026 and is expected to hit USD 155.56 billion by 2034 with a CAGR of 9.02%.

The market has witnessed shipment volumes exceeding 145 million units in 2025, rising from 118 million units in 2023, reflecting strong penetration across emerging and developed economies. Increasing pixel density standards (3840-2160 resolution), refresh rates exceeding 120 Hz, and growing integration of AI-based upscaling technologies are accelerating product differentiation. Additionally, the market segmentation across screen type and end-use, along with competitive benchmarking among major manufacturers controlling over 62% of total shipments, underscores the need for structured data-driven analysis and detailed competitive landscape evaluation.

Asia Pacific 4K Ultra HD Television Market Overview

The Asia Pacific 4K Ultra HD Television market represents the ecosystem of high-resolution television devices offering 4K display standards with over 8.3 million pixels per screen, delivering superior image clarity, HDR10+ compatibility, and enhanced color depth exceeding 1 billion colors. Regional production crossed 162 million units in 2025, with China accounting for 46%, South Korea 18%, and Japan 12% of total manufacturing output. Adoption rates have surged, with urban household penetration reaching 58% in 2025 compared to 41% in 2022, while smart TV integration stands above 72% across 4K devices.

Consumer behavior indicates rising preference for screen sizes above 55 inches, accounting for nearly 64% of total sales, driven by OTT consumption growth of 28% annually and gaming usage penetration exceeding 37%. Residential applications dominate with 71% share, followed by commercial (18%) and institutional (11%) deployments. Technical performance metrics such as brightness levels exceeding 1000 nits and contrast ratios above 1,000,000:1 are influencing purchase decisions. This evolving ecosystem continues to reinforce Asia Pacific 4K Ultra HD Television market share expansion across diverse applications.

In the Japan, the 4K Ultra HD Television Market has demonstrated strong technological leadership with over 320 manufacturing facilities and R&D centers actively producing advanced display panels. Japan contributes approximately 14% of the Asia Pacific market, with annual production exceeding 22 million units in 2025. Residential applications dominate with 68% share, followed by commercial usage at 21% and institutional demand at 11%. OLED technology adoption in Japan exceeds 44%, significantly higher than the regional average of 31%, driven by premium consumer preferences and high disposable income.

The country also leads in innovation, with 78% of televisions incorporating AI-enhanced upscaling and 65% supporting advanced HDR formats. Average screen size demand has increased from 49 inches in 2022 to 57 inches in 2025. Furthermore, 4K broadcasting infrastructure covers over 92% of households, boosting demand for compatible devices. These factors collectively strengthen Asia Pacific 4K Ultra HD Television market growth through Japan's technological and consumption leadership.

Asia Pacific 4K Ultra HD Television Market Trends

Rising Adoption of OLED and QLED Technologies

The shift toward OLED and QLED technologies is transforming production and consumption patterns, with OLED shipments growing by 18.5% year-on-year and QLED accounting for nearly 27% of premium segment sales in 2025. Production volumes for OLED panels reached 14.2 million units, while QLED shipments surpassed 22 million units across Asia Pacific. Advanced display technologies offering higher brightness levels (up to 2000 nits) and improved energy efficiency (20% lower consumption) are attracting consumers.

Additionally, integration of AI processors and machine learning algorithms has enhanced real-time image optimization, with over 63% of new models featuring adaptive picture engines. These advancements are driving Asia Pacific 4K Ultra HD Television market trends toward premiumization and performance-driven consumption.

Expansion of Smart TV Ecosystems and OTT Integration

Smart TV penetration within 4K devices has reached 74% in 2026, supported by OTT platform growth exceeding 30% annually. Over 112 million units shipped in 2025 were internet-enabled, with built-in streaming apps accounting for 82% of usage time. Voice assistant integration has grown to 48% adoption, while gaming-focused features such as 120 Hz refresh rates and HDMI 2.1 ports are present in 36% of models.

The increasing demand for home entertainment systems, combined with rising internet penetration above 67% in Southeast Asia, is accelerating digital content consumption. These developments significantly contribute to evolving Asia Pacific 4K Ultra HD Television market trends.

Asia Pacific 4K Ultra HD Television Market Driver

Rapid Expansion of OTT Platforms and Digital Content Consumption

The proliferation of OTT platforms has significantly accelerated demand, with Asia Pacific OTT subscriptions surpassing 650 million users in 2025, growing at 22% annually. Over 72% of consumers prefer streaming content in 4K resolution, driving sales of compatible televisions. The increasing availability of 4K content libraries, which have grown by 38% since 2022, further enhances device adoption.

Additionally, internet penetration has reached 67% across Asia Pacific, with countries like South Korea and Japan exceeding 90%. The average daily screen time has increased from 2.8 hours in 2022 to 3.9 hours in 2025, reinforcing demand for high-quality displays. These factors collectively drive Asia Pacific 4K Ultra HD Television market growth through sustained content consumption expansion.

Asia Pacific 4K Ultra HD Television Market Restraint

High Cost of Advanced Display Technologies

Despite technological advancements, high costs remain a significant barrier, particularly for OLED models, which are priced 35%-50% higher than standard LED televisions. Average selling prices for OLED TVs exceed USD 1,200 compared to USD 650 for LED models. In emerging economies such as India and Southeast Asia, price sensitivity affects adoption rates, with penetration remaining below 32%.

Additionally, production costs for advanced panels have increased by 12% due to rising raw material prices and supply chain disruptions. Limited affordability among rural populations, which account for over 45% of the region's population, further constrains expansion. These factors collectively restrain Asia Pacific 4K Ultra HD Television market growth.

Asia Pacific 4K Ultra HD Television Market Opportunity

Growing Demand for Large-Screen and Gaming Displays

The increasing popularity of gaming and home theaters presents significant opportunities, with gaming console sales rising by 26% annually and over 41% of gamers preferring 4K displays. Screen sizes above 65 inches now account for 38% of total sales, up from 22% in 2022. Gaming-oriented features such as variable refresh rates (VRR) and low latency modes are driving demand.

Moreover, the expansion of e-sports markets, valued at over USD 3.5 billion in Asia Pacific, further supports adoption. Manufacturers investing 18%-22% of R&D budgets in gaming display optimization are capitalizing on this trend. These developments unlock new Asia Pacific 4K Ultra HD Television market insights across premium segments.

Challenge in Asia Pacific 4K Ultra HD Television Market

Intense Competition and Price Erosion

The market is characterized by intense competition, with over 45 major manufacturers operating in the region and top five players controlling 62% of market share. Price wars have led to average selling price declines of 9% annually, particularly in the LED segment. Chinese manufacturers offering low-cost alternatives have increased their share from 28% in 2022 to 36% in 2025.

Additionally, rapid product lifecycle turnover, averaging 18â24 months, increases inventory risks and operational costs. The need for continuous innovation and differentiation places pressure on margins, which have declined by 6% across the industry. These challenges impact Asia Pacific 4K Ultra HD Television market growth sustainability.

Asia Pacific 4K Ultra HD Television Market Segmentation

By Type

LED televisions dominate with 49% market share and production exceeding 78 million units in 2025. These devices offer brightness levels of 500â800 nits and energy efficiency improvements of 15% compared to older LCD models. Cost-effectiveness and availability across price segments make LED the most accessible technology, particularly in emerging economies where adoption exceeds 62%.

OLED accounts for 24% share with production volumes of 34 million units. These televisions offer superior contrast ratios exceeding 1,000,000:1 and thinner panel designs below 5 mm. Adoption is concentrated in premium markets, with penetration exceeding 44% in Japan and South Korea.

QLED holds 27% share with shipments surpassing 43 million units. Offering brightness levels above 1500 nits and improved color accuracy, QLED technology is gaining traction among mid-to-premium consumers.

By Application

Residential applications dominate with 71% share, with over 103 million units deployed in 2025. Rising OTT consumption and home entertainment demand are key drivers.

Commercial usage accounts for 18%, with deployment in hospitality, retail, and corporate sectors exceeding 26 million units. Digital signage and advertising applications drive demand.

Institutional applications hold 11% share, with adoption in education and government sectors growing at 8% annually.

| Screen Type | End-Use |

|---|---|

|

|

Country Insights

China

China leads with 46% market share and production exceeding 74 million units annually. Domestic consumption accounts for 61% of total output.

South Korea

South Korea contributes 18%, driven by advanced manufacturing and OLED production exceeding 12 million units.

Japan

Japan holds 14% share with strong premium segment demand and advanced R&D infrastructure.

India

India accounts for 9% share, with rapid growth driven by urbanization and rising disposable income.

Australia

Australia holds 4% share with high household penetration exceeding 68%.

Singapore

Singapore contributes 3%, driven by high-income consumers and premium product adoption.

Taiwan

Taiwan accounts for 3% share with strong semiconductor and display panel manufacturing.

South East Asia

The region holds 3% share with growing adoption driven by rising middle-class populations.

Top Players in Asia Pacific 4K Ultra HD Television Market

- Samsung Electronics

- LG Electronics

- Sony Corporation

- Panasonic Corporation

- TCL Technology

- Hisense Group

- Sharp Corporation

- Skyworth Group

- Philips

- Vizio Inc.

- Xiaomi Corporation

- Haier Group

- Changhong Electric

Top Two Companies

Samsung Electronics

- Holds approximately 28% market share

- Leads in QLED technology and global distribution

- Invests over 20% of R&D budget in display innovation

LG Electronics

- Commands 21% market share

- Dominates OLED segment with over 55% share

- Strong presence in premium and smart TV ecosystems

Investment

Investment in the market exceeded USD 18.6 billion in 2025, with 42% allocated to display technology innovation and 28% to manufacturing expansion. China and South Korea account for over 63% of total investments, while India and Southeast Asia are emerging hotspots with investment growth above 19% annually.

M&A activity has increased, with over 35 strategic partnerships formed between 2023 and 2025, focusing on panel manufacturing and AI integration.

New Product

Over 36% of new product launches in 2025 featured AI-powered picture enhancement, while 28% included gaming-specific features. Performance improvements include 22% higher brightness and 18% energy efficiency gains.

Recent Development in Asia Pacific 4K Ultra HD Television Market

- 2025: Samsung increased QLED production by 19%

- 2024: LG expanded OLED capacity by 23%

- 2023: TCL boosted shipments by 17%

Research Methodology for Asia Pacific 4K Ultra HD Television Market

The research process combines primary and secondary data sources, including manufacturer reports, trade statistics, and industry databases. Primary research involves interviews with over 45 industry experts and executives, while secondary research analyzes over 120 data sources. Market size estimation uses bottom-up and top-down approaches, ensuring accuracy through triangulation methods.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.